13th June 2023 Shift 2 All PYQ’s of UGC NET/JRF Unit 4 Business Finance Commerce Subject:

Table of Contents

1. Question

The adjusted present value model used by MNCs to evaluate capital budgeting decision is based on

- Gresham’s principle

- Value additivity approach

- Law of one price

- Multilateral Netting approach

Solutions:

The correct answer is Value Additivity Principle

Important Points

- Value Additivity Principle

- The Value Additivity Principle in NPV states that the value of the total NPV of a bigger project is equal to the summation of all smaller NPVs of projects. In other words, the summation of all smaller NPVs provides the bigger NPV of an investment project. The NPV of a group of the independent projects will be equivalent to the NPV of all the independent projects.

- If A and B are two smaller projects, then the total NPV of the bigger project (A+B) would be −

- NPV (A+B) = NPV (A) + NPV (B)

- The adjusted present value model used by MNCs to evaluate capital budgeting decision is based on this method

Additional Information

- law of one price (LOOP) :

- The law of one price (LOOP) states that in the absence of trade frictions (such as transport costs and tariffs), and under conditions of free competition and price flexibility (where no individual sellers or buyers have power to manipulate prices and prices can freely adjust), identical goods sold in different locations must sell for the same price when prices are expressed in a common currency

- Gresham’s law:

- In economics, Gresham’s law is a monetary principle stating that “bad money drives out good”.

- For example, if there are two forms of commodity money in circulation, which are accepted by law as having similar face value, the more valuable commodity will gradually disappear from circulation

- Multilateral netting:

- Netting is the process of consolidating payables against receivables between parties.

- Multilateral netting involves pooling the funds from two or more parties so that a more simplified invoicing and payment process can be achieved.

- It is a payment arrangement among multiple parties that transactions be summed, rather than settled individually. Multilateral netting can take place within a single organization or among two or more parties.

2. Question

Which one of the following is an operational technique of hedging transaction exposure.

- Hedging through money market

- Hedging through forward

- Hedging through swap

- Hedging through leading & lagging

Solutions:

The correct answer is Hedging through leading & lagging.

Hedging in stock market is a strategy used by investors to reduce the risk of adverse price movements in an asset. It involves taking an offsetting position in a related security or financial instrument, with the goal of minimizing potential losses from market volatility.

Key Points

- Types of Hedging:

- Hedging through money market :

- It is a technique used to lock in the value of a foreign currency transaction in a company’s domestic currency.

- Therefore, a money market hedge can help a domestic company reduce its exchange rate or currency risk when conducting business transactions with a foreign company.

- It is called a money market hedge because the process involves depositing funds into a money market, which is the financial market of highly liquid and short-term instruments like Treasury bills, bankers’ acceptances, and commercial paper.

- Hedging through forward :

- Forward contract is used for hedging the foreign exchange risk for future settlement.

- For example, An importer or exporter having FX contract limit may lock in current exchange rate by entering into forward contract with the bank to avoid adverse rate movement.

- Hedging through swap :

- Currency swaps are a way to help hedge against that type of currency risk by swapping cash flows in the foreign currency with domestic at a pre-determined rate.

- Leading and lagging –

- In this timing payments in foreign currencies and take advantage of currency movements.

- Leading is paying in advance, and lagging is paying later, sometimes after the due date. Businesses that use these techniques try to anticipate which way a currency will move and make their transactions accordingly.

- It is a type of operational hedging that is the course of action that hedges the firm’s risk exposure by means of non-financial instruments, particularly through operational activities.

- Hedging through money market :

3. Question

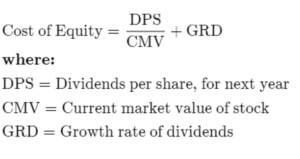

A company’s stock sells for Rs. 63. The company pays an annual dividend of Rs. 3 per share and has long established record of increasing its dividend by a context 5% annually. For this company, the cost of equity (Ke) is ______.

- 13%

- 14%

- 10%

- 8%

Solutions:

The correct answer is 10%

Key Points

- Cost of equity

- It is the return that a company requires for an investment or project, or the return that an individual requires for an equity investment.

- The formula used to calculate the cost of equity is either the dividend capitalization model or the CAPM.

- Here DPS=3 Rs

- CMV=63 Rs

- GRD=0.05

- Putting values in above formula

- =(3/63)=0.05

- 0.0976 ~ 10%

4. Question

Sequence the following steps in the process of securitisation.

A. Special purpose vehicle (SPV) issue tradeble securities to find the purchase of pool of assets

B. SPV subcotracts (outsource) the originator for collection of intrest and principle payments on the pool of assets

C. SPV repay the funds to the investor or cashflow arise on the pool of assets

D. Originator maker a pool of assets and sold it to the SPV

E. SPV pays the funds the orgination for the pool of assets

Choose the correct answer from the options given below:

- B, D, A, C, E

- D, E, B, A, C

- D, B, A, E, C

- E, A, B, D, C

Solutions:

The correct answer is – D, B, A, E, C

Key Points

- Step D: Originator creates a pool of assets and sells it to the SPV

- The originator (such as a bank or financial institution) gathers assets (e.g., loans, mortgages) and sells them to the Special Purpose Vehicle (SPV), an entity created for securitisation.

- This is the first step in securitisation, where the originator transfers ownership of the pool of assets to the SPV.

- Step B: SPV outsources the collection of payments to the originator

- The SPV outsources the responsibility of collecting interest and principal payments from the asset holders to the originator.

- This helps the SPV reduce operational complexity and risk, leveraging the originator’s existing infrastructure.

- Step A: SPV issues tradeable securities to fund the purchase of assets

- The SPV issues tradeable securities, such as asset-backed securities (ABS), in the financial market to raise funds for purchasing the assets from the originator.

- Investors buy these securities, providing the SPV with the necessary funds to complete the asset purchase.

- Step E: SPV pays the funds to the originator for the pool of assets

- Once the SPV raises the necessary funds by issuing the securities, it pays the originator for the pool of assets transferred earlier.

- This step ensures the originator receives payment for the assets that have been sold to the SPV.

- Step C: SPV repays the funds to the investor or cash flow arises on the pool of assets

- As the asset pool generates payments, the SPV uses the proceeds to repay the investors in the form of interest and principal payments.

- This final step ensures that investors receive returns from the cash flows generated by the assets.

Additional Information

- Securitisation Process

- Securitisation is a financial process where assets are pooled together and then converted into tradeable securities.

- The SPV plays a critical role in isolating the pool of assets from the originator’s balance sheet, thus reducing risk and enabling easier access to capital.

- Role of SPV

- The SPV is a legal entity created solely for the purpose of holding the asset pool and issuing the securities.

- It helps protect investors by ensuring that the underlying assets are legally separated from the originator.

- Investors in Securitisation

- Investors in securitisation typically include institutions like banks, pension funds, and mutual funds that seek to invest in asset-backed securities.

- These investors receive periodic payments based on the cash flows generated by the underlying assets in the pool.

5. Question

Match List I with List II.

| List I Capital Structure theories | List II Key Components | ||

| (a) | MM approach | (i) | Costs of financial distress |

| (b) | Pecking order theory | (ii) | Assymetric information |

| (c) | Trade off theory | (iii) | No target capital structure |

| (d) | Signaling thoery | (iv) | Home made Leverage |

Choose the correct answer answer from the options given below:

- A – III, B – II, C – IV, D – I

- A – IV, B – III, C – I, D – II

- A – IV, B – I, C – III, D – II

- A – IV, B – III, C – II, D – I

Solutions:

The correct answer is A – IV, B – III, C – I, D – II.

Important Points MM approach – Home made Leverage

- Modigliani-Miller theorem – Investors can create their own leverage by borrowing and investing in risk-free assets.

- Homemade leverage- Investors can replicate the effects of corporate leverage by borrowing and investing in a firm’s debt and equity.

Implications –

- Firms’ capital structure is irrelevant to investors.

- Firms should focus on maximizing expected future cash flows and reducing risk, regardless of how they finance their operations.

In other words, investors can achieve the same level of risk and return regardless of the firm’s capital structure. This is because they can always borrow or lend money to adjust their own leverage.

Pecking order theory – No target capital structure

- The Pecking Order Theory suggests that firms prioritize financing methods in a specific order.

- This begin with internal funds, followed by debt issuance, and finally, equity issuance.

- Unlike the traditional notion of a target capital structure, this theory contends that firms do not have a predetermined mix of debt and equity in mind.

- Instead, they rely on available funds and prefer internal financing due to the asymmetry of information between management and external investors.

- This theory emphasizes the pragmatic approach firms take in their financing decisions.

Trade off theory – Costs of financial distress

- Trade-off theory in finance suggests that companies must strike a balance between the tax benefits of debt financing and the costs associated with financial distress.

- The costs of financial distress include legal and administrative expenses related to bankruptcy proceedings, the loss of customer and supplier relationships, and the decline in the firm’s value due to the uncertainty surrounding its financial health.

- Additionally, financial distress can lead to a reduced ability to invest in profitable projects, ultimately impacting the company’s long-term viability.

Signaling theory – Asymmetric information

- Signaling theory addresses situations where one party possesses more or better information than another.

- In financial contexts, it often refers to a firm’s ability to convey its quality or prospects to investors.

- For example, a company may issue a dividend to signal confidence in its future earnings or undertake a stock buyback to indicate undervaluation.

- These actions are intended to bridge the information gap and convey positive signals to investors, potentially affecting the firm’s stock price.