13th June 2023 Shift 2 All PYQ’s of UGC NET/JRF Unit 4 Business Finance Commerce Subject:

Table of Contents

1. Question

The adjusted present value model used by MNCs to evaluate capital budgeting decision is based on

- Gresham’s principle

- Value additivity approach

- Law of one price

- Multilateral Netting approach

Solutions:

The correct answer is Value Additivity Principle

Important Points

- Value Additivity Principle

- The Value Additivity Principle in NPV states that the value of the total NPV of a bigger project is equal to the summation of all smaller NPVs of projects. In other words, the summation of all smaller NPVs provides the bigger NPV of an investment project. The NPV of a group of the independent projects will be equivalent to the NPV of all the independent projects.

- If A and B are two smaller projects, then the total NPV of the bigger project (A+B) would be −

- NPV (A+B) = NPV (A) + NPV (B)

- The adjusted present value model used by MNCs to evaluate capital budgeting decision is based on this method

Additional Information

- law of one price (LOOP) :

- The law of one price (LOOP) states that in the absence of trade frictions (such as transport costs and tariffs), and under conditions of free competition and price flexibility (where no individual sellers or buyers have power to manipulate prices and prices can freely adjust), identical goods sold in different locations must sell for the same price when prices are expressed in a common currency

- Gresham’s law:

- In economics, Gresham’s law is a monetary principle stating that “bad money drives out good”.

- For example, if there are two forms of commodity money in circulation, which are accepted by law as having similar face value, the more valuable commodity will gradually disappear from circulation

- Multilateral netting:

- Netting is the process of consolidating payables against receivables between parties.

- Multilateral netting involves pooling the funds from two or more parties so that a more simplified invoicing and payment process can be achieved.

- It is a payment arrangement among multiple parties that transactions be summed, rather than settled individually. Multilateral netting can take place within a single organization or among two or more parties.

2. Question

Which one of the following is an operational technique of hedging transaction exposure.

- Hedging through money market

- Hedging through forward

- Hedging through swap

- Hedging through leading & lagging

Solutions:

The correct answer is Hedging through leading & lagging.

Hedging in stock market is a strategy used by investors to reduce the risk of adverse price movements in an asset. It involves taking an offsetting position in a related security or financial instrument, with the goal of minimizing potential losses from market volatility.

Key Points

- Types of Hedging:

- Hedging through money market :

- It is a technique used to lock in the value of a foreign currency transaction in a company’s domestic currency.

- Therefore, a money market hedge can help a domestic company reduce its exchange rate or currency risk when conducting business transactions with a foreign company.

- It is called a money market hedge because the process involves depositing funds into a money market, which is the financial market of highly liquid and short-term instruments like Treasury bills, bankers’ acceptances, and commercial paper.

- Hedging through forward :

- Forward contract is used for hedging the foreign exchange risk for future settlement.

- For example, An importer or exporter having FX contract limit may lock in current exchange rate by entering into forward contract with the bank to avoid adverse rate movement.

- Hedging through swap :

- Currency swaps are a way to help hedge against that type of currency risk by swapping cash flows in the foreign currency with domestic at a pre-determined rate.

- Leading and lagging –

- In this timing payments in foreign currencies and take advantage of currency movements.

- Leading is paying in advance, and lagging is paying later, sometimes after the due date. Businesses that use these techniques try to anticipate which way a currency will move and make their transactions accordingly.

- It is a type of operational hedging that is the course of action that hedges the firm’s risk exposure by means of non-financial instruments, particularly through operational activities.

- Hedging through money market :

3. Question

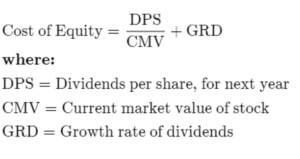

A company’s stock sells for Rs. 63. The company pays an annual dividend of Rs. 3 per share and has long established record of increasing its dividend by a context 5% annually. For this company, the cost of equity (Ke) is ______.

- 13%

- 14%

- 10%

- 8%

Solutions:

The correct answer is 10%

Key Points

- Cost of equity

- It is the return that a company requires for an investment or project, or the return that an individual requires for an equity investment.

- The formula used to calculate the cost of equity is either the dividend capitalization model or the CAPM.

- Here DPS=3 Rs

- CMV=63 Rs

- GRD=0.05

- Putting values in above formula

- =(3/63)=0.05

- 0.0976 ~ 10%

4. Question

Sequence the following steps in the process of securitisation.

A. Special purpose vehicle (SPV) issue tradeble securities to find the purchase of pool of assets

B. SPV subcotracts (outsource) the originator for collection of intrest and principle payments on the pool of assets

C. SPV repay the funds to the investor or cashflow arise on the pool of assets

D. Originator maker a pool of assets and sold it to the SPV

E. SPV pays the funds the orgination for the pool of assets

Choose the correct answer from the options given below:

- B, D, A, C, E

- D, E, B, A, C

- D, B, A, E, C

- E, A, B, D, C

Solutions:

The correct answer is – D, B, A, E, C

Key Points

- Step D: Originator creates a pool of assets and sells it to the SPV

- The originator (such as a bank or financial institution) gathers assets (e.g., loans, mortgages) and sells them to the Special Purpose Vehicle (SPV), an entity created for securitisation.

- This is the first step in securitisation, where the originator transfers ownership of the pool of assets to the SPV.

- Step B: SPV outsources the collection of payments to the originator

- The SPV outsources the responsibility of collecting interest and principal payments from the asset holders to the originator.

- This helps the SPV reduce operational complexity and risk, leveraging the originator’s existing infrastructure.

- Step A: SPV issues tradeable securities to fund the purchase of assets

- The SPV issues tradeable securities, such as asset-backed securities (ABS), in the financial market to raise funds for purchasing the assets from the originator.

- Investors buy these securities, providing the SPV with the necessary funds to complete the asset purchase.

- Step E: SPV pays the funds to the originator for the pool of assets

- Once the SPV raises the necessary funds by issuing the securities, it pays the originator for the pool of assets transferred earlier.

- This step ensures the originator receives payment for the assets that have been sold to the SPV.

- Step C: SPV repays the funds to the investor or cash flow arises on the pool of assets

- As the asset pool generates payments, the SPV uses the proceeds to repay the investors in the form of interest and principal payments.

- This final step ensures that investors receive returns from the cash flows generated by the assets.

Additional Information

- Securitisation Process

- Securitisation is a financial process where assets are pooled together and then converted into tradeable securities.

- The SPV plays a critical role in isolating the pool of assets from the originator’s balance sheet, thus reducing risk and enabling easier access to capital.

- Role of SPV

- The SPV is a legal entity created solely for the purpose of holding the asset pool and issuing the securities.

- It helps protect investors by ensuring that the underlying assets are legally separated from the originator.

- Investors in Securitisation

- Investors in securitisation typically include institutions like banks, pension funds, and mutual funds that seek to invest in asset-backed securities.

- These investors receive periodic payments based on the cash flows generated by the underlying assets in the pool.

5. Question

Match List I with List II.

| List I Capital Structure theories | List II Key Components | ||

| (a) | MM approach | (i) | Costs of financial distress |

| (b) | Pecking order theory | (ii) | Assymetric information |

| (c) | Trade off theory | (iii) | No target capital structure |

| (d) | Signaling thoery | (iv) | Home made Leverage |

Choose the correct answer answer from the options given below:

- A – III, B – II, C – IV, D – I

- A – IV, B – III, C – I, D – II

- A – IV, B – I, C – III, D – II

- A – IV, B – III, C – II, D – I

Solutions:

The correct answer is 2. A – IV, B – III, C – I, D – II.

Important Points MM approach – Home made Leverage

- Modigliani-Miller theorem – Investors can create their own leverage by borrowing and investing in risk-free assets.

- Homemade leverage- Investors can replicate the effects of corporate leverage by borrowing and investing in a firm’s debt and equity.

Implications –

- Firms’ capital structure is irrelevant to investors.

- Firms should focus on maximizing expected future cash flows and reducing risk, regardless of how they finance their operations.

In other words, investors can achieve the same level of risk and return regardless of the firm’s capital structure. This is because they can always borrow or lend money to adjust their own leverage.

Pecking order theory – No target capital structure

- The Pecking Order Theory suggests that firms prioritize financing methods in a specific order.

- This begin with internal funds, followed by debt issuance, and finally, equity issuance.

- Unlike the traditional notion of a target capital structure, this theory contends that firms do not have a predetermined mix of debt and equity in mind.

- Instead, they rely on available funds and prefer internal financing due to the asymmetry of information between management and external investors.

- This theory emphasizes the pragmatic approach firms take in their financing decisions.

Trade off theory – Costs of financial distress

- Trade-off theory in finance suggests that companies must strike a balance between the tax benefits of debt financing and the costs associated with financial distress.

- The costs of financial distress include legal and administrative expenses related to bankruptcy proceedings, the loss of customer and supplier relationships, and the decline in the firm’s value due to the uncertainty surrounding its financial health.

- Additionally, financial distress can lead to a reduced ability to invest in profitable projects, ultimately impacting the company’s long-term viability.

Signaling theory – Asymmetric information

- Signaling theory addresses situations where one party possesses more or better information than another.

- In financial contexts, it often refers to a firm’s ability to convey its quality or prospects to investors.

- For example, a company may issue a dividend to signal confidence in its future earnings or undertake a stock buyback to indicate undervaluation.

- These actions are intended to bridge the information gap and convey positive signals to investors, potentially affecting the firm’s stock price.

6. Question

Match List I with List II.

| List I Capital Structure theories | List II Key Components | ||

| A. | Opportunity cost Approach | I. | David Watson |

| B. | Replacement cost Approach | II. | Rensis Likert and Eric G. Flamholtg |

| C. | Historical cost Approach | III. | Brummer Flamholtz and Pyle |

| D. | Standard cost Approach | IV. | Hekimian and jones |

Choose the correct answer answer from the options given below:

- A – I, B – II, C – III, D – IV

- A – II, B – III, C – I, D – IV

- A – I, B – IV, C – III, D – II

- A – IV, B – II, C – III, D – I

Solutions:

The correct answer is A – IV, B – II, C – III, D – I.

Important PointsOpportunity cost Approach – Hekimian and jones

- Hekimian and Jones’ Opportunity Cost Approach is a method for evaluating the cost of equity capital.

- It posits that the cost of equity is equivalent to the return that could be earned on an investment of similar risk elsewhere in the market.

- This approach considers the foregone returns an investor could have earned in alternative investments of comparable risk.

- By comparing the expected returns from different investment opportunities, it helps determine the appropriate cost of equity for a company.

Replacement cost Approach – Rensis Likert and Eric G. Flamholtg

- The Replacement Cost Approach was introduced by Rensis Likert and Eric G. Flamholtz.

- It is a method used in financial accounting that values assets based on the cost to replace them at current market prices.

- This approach provides a more accurate reflection of a company’s true economic worth, especially in times of inflation or changing market conditions.

- By considering the cost of acquiring or replicating assets, it offers a more realistic assessment of a company’s value compared to historical cost accounting methods.

Historical cost Approach – Brummer Flamholtz and Pyle

- The Historical Cost Approach, associated with Brummer, Flamholtz, and Pyle, is an accounting method that values assets at their original purchase cost.

- This approach does not consider changes in market value or inflation over time.

- It is straightforward and easy to implement, providing a reliable record of transactions.

- However, critics argue that it may not reflect the true economic value of assets, especially in times of inflation or rapidly changing market conditions.

Standard cost Approach – David Watson

- The Standard Cost Approach, associated with David Watson, is a method used in managerial accounting to establish predetermined, standard costs for producing goods or services.

- These standard costs are based on a detailed analysis of past performance, industry benchmarks, and other relevant factors.

- Deviations from the standard costs can indicate areas where operations may need improvement or where there may be unexpected efficiencies.

- This approach helps in cost control and performance evaluation within an organization.

7. Question

The coexistence and cooperation between the formal and informed financial sector is commonly referred to as:

- Flexibility of operation

- Financial dualism

- Well regulated financial system

- Catering the financial needs of modern economy

Solutions:

The correct answer is 2. financial dualism.

Key Points

- The formal financial sector refers to regulated and organized institutions like banks, credit unions, and financial markets that operate under government supervision.

- On the other hand, the informal financial sector consists of unregulated and often community-based systems, like moneylenders, rotating savings and credit associations (ROSCAs), and microfinance groups.

Important Points

- Financial dualism refers to the coexistence of a formal and informal financial sector in an economy.

- The formal financial sector is regulated by the government and includes banks, microfinance institutions, and other financial institutions that offer a variety of financial services, such as savings accounts, loans, and insurance.

- The informal financial sector is unregulated and includes a variety of traditional financial institutions, such as money lenders, rotating savings and credit associations (ROSCAs), and pawnbrokers.

- Financial dualism may exist because of cultural factors. Some people may prefer to use the informal financial sector because it is more familiar to them or because they do not trust the formal financial sector.

- There are a number of benefits to financial dualism.

- The informal financial sector can provide financial services to people who would not otherwise have access to them.

- This can help to promote economic growth and development. The informal financial sector can also help to reduce poverty by providing people with the financial resources they need to start or grow a business.

some examples of cooperation between the formal and informal financial sectors –

- Banks may offer mobile banking services to reach customers in rural areas.

- Insurance companies may offer micro-insurance products to low-income people.

- Governments may provide training and financial support to informal financial institutions.

8. Question

Which of the following elements cause problem in application of internal rate of return method while evaluating mutually exclusive projects?

A. Discount rate

B. Timing

C. Scale

D. Reversing flow

E. Leverage

Choose the correct answer from the options given below:

- A, B only

- D, E only

- B, C only

- A, D only

Solutions:

The correct answer is B, C only.

Key PointsLet’s analyze each statement:

- Discount Rate

- This option is incorrect because:

- The internal rate of return (IRR) method itself doesn’t directly focus on the discount rate; it determines the discount rate that makes the net present value (NPV) zero.

- When comparing mutually exclusive projects, IRR doesn’t directly address differences caused by varying discount rates.

- Timing

- This option is correct because:

- IRR may not accurately handle projects with different cash flow timings.

- Projects with early returns versus those with later returns can yield misleading IRR results, leading to potentially poor decision-making.

- Scale

- This option is correct because:

- The IRR method doesn’t consider the scale or size of projects.

- Comparing projects of different scales using IRR can be misleading, as a higher IRR on a small project might be less desirable than a lower IRR on a larger project.

- Reversing Flow

- This option is incorrect because:

- Reversing flow (changes in the direction of cash flows) can complicate IRR calculations but isn’t a fundamental problem in comparing mutually exclusive projects.

- Multiple IRRs can exist if cash flows change direction, but this issue isn’t specific to project scale or timing differences.

- Leverage

- This option is incorrect because:

- Leverage refers to the use of borrowed capital to finance a project, which isn’t a direct concern when comparing the IRR of mutually exclusive projects.

- IRR analysis typically assumes project financing is separate from evaluation.

Based on the evaluation above, the correct answer is option 3: B and C, as these statements correctly describe aspects of the limitations of the IRR method when evaluating mutually exclusive projects.

9. Question

Given below are two statements: one is labelled as Assertion A and the other is labelled as Reason R

Assertion A: Cross listing can potentially increase the stock price and lower the cost of capital

Reason R: Cross listing facilitates wider stock ownership and expands invester base for a firm’s stock

In the light of the above statements, choose the correct answer from the options Given below:

- Both A and R are true and R is the correct explanation of A

- Both A and R are true and R is NOT correct explanation of A

- A is true but R is false

- A is false but R is true

Solutions:

Key Points

Assertion A: Cross listing can potentially increase the stock price and lower the cost of capital.

- Cross-listing is the listing of a company’s common shares on a different exchange than its primary and original stock exchange. Companies must meet the exchange’s listing requirements in order to be cross-listed.

- Advantages to cross-listing include having shares trade in multiple time zones, boosting liquidity and providing access to fresh capital.

- The international exposure provides companies with more liquidity, meaning there’s a healthy amount of buyers and sellers in the market. The added liquidity provides companies with a greater ability to raise capital or new money to invest in the future of the company.

- Hence Assertion A is correct.

Reason R: Cross listing facilitates wider stock ownership and expands invester base for a firm’s stock

- Companies that list shares across the globe attract varied investors belonging to different countries. This means more capital. But it also facilitates diversification advantages. MNCs that list globally are insulated from economic fluctuation occurring in a part of the world.

- Having shares in multiple exchanges buys the firm goodwill and a reputation in the international market. In addition, it adds to the firm’s international presence.

- Hence Reason R is correct,

Therefore we can say that Both A and R are true and R is the correct explanation of A,

10. Question

The dividend-irrelevance theory of Miller and Modigliani depends on which one of the following relationships between investment policy and dividend policy.

- Since dividend policy is irrelevant, there is no relationship between investment policy and dividend policy

- The level of investment does not influence or matter to the dividend decision

- Once dividend policy is set, the investment decision are residuals

- The investment policy is set ahead of time and not altered by change in dividend policy

Solutions:

The correct answer is 4. The investment policy is set ahead of time and not altered by change in dividend policy

Key Points

Dividend irrelevance theory :

- It proposes that a company’s dividend policy does not affect its overall value or stock price. It was introduced by Franco Modigliani and Merton Miller in 1961.

- It suggests that investors can create their desired income stream by buying or selling company shares as needed. This is regardless of whether the company pays dividends or retains its earnings.

- The theory aims to understand the relationship between dividends and a company’s value.

- This theory states that dividend patterns have no effect on share values.

- Broadly it suggests that if a dividend is cut now then the extra retained earnings reinvested will allow futures earnings and hence future dividends to grow.

- The investment policy is set ahead of time and not altered by change in dividend policy

- Dividend irrelevance theory holds that the markets perform efficiently so that any dividend payout will lead to a decline in the stock price by the amount of the dividend.

- In other words, if the stock price was $10, and a few days later, the company paid a dividend of $1, the stock would fall to $9 per share.

- As a result, holding the stock for the dividend achieves no gain since the stock price adjusts lower for the same amount of the payout

11. Question

Brewing financial stress endangering economic stability in developed economics is the immediate consequence of which of the following?

- Fiscal indispline

- Rising price level

- Over leverage

- Increased interest rates

Solutions:

The correct answer is 4. Increased interest rates.

Important Points

- Increased interest rates can lead to financial stress in a number of ways, including –

- Higher borrowing costs –

- When interest rates rise, it becomes more expensive for businesses and consumers to borrow money.

- This can make it difficult for businesses to invest and grow, and for consumers to buy homes and cars.

- It can also lead to higher debt payments for those who are already in debt, which can strain their finances.

- Reduced lending –

- Banks and other financial institutions may also reduce lending when interest rates rise.

- This is because they are more likely to lose money on loans if borrowers default.

- This can make it even more difficult for businesses and consumers to access the financing they need.

- Volatile markets –

- Rising interest rates can also lead to volatility in financial markets. This is because investors may sell off assets such as bonds and stocks in order to lock in higher yields.

- This volatility can make it difficult for businesses to raise capital and for investors to protect their savings.

- Higher borrowing costs –

Additional Information

- Fiscal indiscipline –

- This refers to a situation where a government is not adhering to sound fiscal policies, often characterized by excessive spending, large deficits, and growing public debt.

- While fiscal indiscipline can contribute to economic instability, it is not the immediate consequence mentioned in the question.

- Rising price level (inflation) –

- While high inflation can have negative effects on an economy, such as reducing purchasing power and creating uncertainty,

- it is not directly related to financial stress endangering economic stability.

- Over leverage –

- This occurs when individuals, businesses, or governments take on too much debt relative to their income or assets.

- Over leverage can indeed lead to financial stress, as debt obligations become harder to meet.

- However, it is not the immediate consequence mentioned in the question.

12. Question

Given below are two statements: one is labelled as Assertion A and the other is labelled as Reason R

Assertion A: The return on capital invested is a concept that measures the profit which a firm earns on investing a unit of capital

Reason R: Yield on capital is another term employed to express the idea

In the light of the above statements, choose the most appropriate answer from the options given below:

- Both A and R are correct and R is the correct explanation of A

- Both A and R are correct but R NOT the correct explanation of A

- A is correct but R is not correct

- A is not correct but R is correct

Solutions:

The correct answer is 2. Both A and R are correct but R NOT the correct explanation of A.

Key Points

- Return on capital (ROC) is a measure of how efficiently a company is using its capital to generate profits. It is calculated by dividing the company’s net income by its total capital.

- Yield on capital is a measure of how much profit a company is generating on its capital investment. It is calculated by dividing the company’s operating profit by its total capital.

Important Points

- Both Assertion A and Reason R are correct statements, but Reason R does not provide a correct explanation for Assertion A.

- Assertion A states that the return on capital invested is a concept that measures the profit which a firm earns on investing a unit of capital. This is true. The return on capital invested is a financial metric that evaluates the efficiency and profitability of a company’s capital investments.

- Reason R states that Yield on capital is another term employed to express the idea. This is also true. “Yield on capital” is indeed another term used to refer to the return on capital invested. It represents the earnings generated from the capital invested.

- While both statements are accurate, Reason R does not directly explain or provide additional information about Assertion A. It essentially restates the concept using a different term, which doesn’t serve as an explanation for Assertion A. Therefore, Option 2 is the correct choice.

13. Question

Which of the following are likely to lead an appreciation in the value of a country’s currency?

A. Higher real interest rate

B. Higher nominal interest rate

C. Lower inflation

D. Higher inflation

E. Large current account deficit

Choose the correct answer from the options given below:

- B, C only

- A, C only

- D, B only

- E, A only

Solutions:

The correct option is A, C only.

Key Points

- Higher Real Interest Rate

- Higher real interest rates can attract foreign investors as they can get a higher return on their investment. This increases demand for the country’s currency, which can lead to an appreciation in its value.

- Higher Nominal Interest Rate

- Higher nominal interest rates might also attract foreign investors, but this scenario depends on relative inflation. If a country has high nominal interest rates but also high inflation, then the potential gain from higher nominal interest could be offset by the loss of purchasing power due to inflation.

- Lower Inflation

- Lower inflation generally indicates a stable economy wherein the purchasing power of the currency is well maintained. Inflation erodes purchasing power, and hence, lower inflation rates are often desirable and attract foreign investors, potentially leading to an appreciation of the currency.

- Higher Inflation

- Higher inflation can lead to a depreciation in the value of a currency because it erodes the purchasing power of money over time. This makes goods more expensive, and in turn, reduces the appeal for foreign investors, potentially leading to a depreciation of the currency.

- Large Current Account Deficit

- Large current account deficits usually contribute to the depreciation of a currency. This is because a deficit means that the country is importing more goods, services, and capital than it is exporting. To pay for these imports, it sells its own currency, increasing supply and reducing its value. Therefore, a large current account deficit generally leads to depreciation, not appreciation, of the currency.

Discover more from WebComm.in

Subscribe to get the latest posts sent to your email.