UGC NET / JRF Unit 3: Business Economics PYQ’s 25th Dec 2021 Shift 1:

| Examination: | UGC NET |

| Subject: | COMMERCE (Paper 2) |

| Exam cycle: | 25th Dec 2021 Shift 1 |

| Types of Paper: | PYQ’s (Previous Year Questions) |

| Which Unit? | Unit 3 Business Economics |

Question No.1

Penetration pricing strategy delivers results:

(A) Where price quality association is weak

(B) When the product is perceived as a ‘high technology’ product

(C) When the market is characterised by intensive competition

(D) When the firm uses it as an entry strategy

Choose the most appropriate answer from the options given below:

- B, C only

- A, D only

- A, C, D only

- A, B, C only

Solutions:

The correct answer is A, C, D only

Key Points

Penetration pricing:

- Penetration pricing is a sort of pricing that is particularly aggressive.

- In order to increase customer demand, a company uses this strategy to set its pricing very cheap (sometimes even with a negative margin).

- The corporation then raises the price again, in the hopes of capturing the same degree of client demand as with its previous extremely low pricing.

Important Points Penetration pricing strategy is helpful:

- Where price has a weak relationship with quality.

- When There is competition in the market.

- When It is a strategy to enter the market.

Question No.2

Match List I with List II:

| List I (Pricing Strategies) | List II (Description) | ||

| (A) | Ramsay pricing | (I) | Setting a high price when a product is first introduced and gradually lowering price as it gains scale |

| (B) | Price skimming | (II) | Firm charges lower price (than the ongoing price) to gain market entry |

| (C) | Cost plus pricing | (III) | Price deviations from marginal cost should be inversely proportional to price elasticity of the product |

| (D) | Penetration pricing | (IV) | It is full cost pricing strategy that also includes mark up for target return, degree of competition, price elasticity and availability of substitutes. |

Choose the correct answer from the options given below:

- (A) – (III), (B) – (IV), (C) – (I), (D) – (II)

- (A) – (II), (B) – (I), (C) – (III), (D) – (IV)

- (A) – (III), (B) – (I), (C) – (IV), (D) – (II)

- (A) – (I), (B) – (IV), (C) – (II), (D) – (III)

Solutions:

The correct answer is (A) – (III), (B) – (I), (C) – (IV), (D) – (II)

The correct match is given below:

| List I (Pricing Strategies) | List II (Description) | ||

| (A) | Ramsay pricing | (III) | Price deviations from marginal cost should be inversely proportional to price elasticity of the product |

| (B) | Price skimming | (I) | Setting a high price when a product is first introduced and gradually lowering price as it gains scale |

| (C) | Cost plus pricing | (IV) | It is full cost pricing strategy that also includes mark up for target return, degree of competition, price elasticity and availability of substitutes. |

| (D) | Penetration pricing | (II) | Firm charges lower price (than the ongoing price) to gain market entry |

Important Points

Ramsay pricing:

- It is a pricing strategy that promotes economic welfare while ensuring that enterprises meet profit targets.

- Ramsey pricing reduces to marginal cost pricing if all companies produce with constant returns to scale and must break even.

- The mark-ups of the Ramsey pricing over marginal cost are inversely related to the elasticity of demand if enterprises have growing returns to scale and must break even.

- Ramsey pricing has been studied in the setting of regulated private sector natural monopoly and public sector monopoly.

- The Ramsey rule for optimal commodity taxes is closely related to Ramsey pricing.

Price skimming:

- Price skimming is a pricing technique in which a product’s or service’s price is initially set high and then gradually reduced as customers become more familiar with it.

- This strategy is aimed at early adopters rather than the general public.

Cost plus pricing:

- Markup pricing is another name for cost-plus pricing.

- It’s a form of pricing in which a fixed percentage is added to the cost of producing one unit of a product (unit cost).

- The resulting number is the product’s selling price.

- This pricing technique considers only the unit cost and ignores rival prices.

- As a result, it is not necessarily the ideal fit for many firms because it ignores external issues such as competition.

Penetration pricing:

- Businesses use penetration pricing as a marketing tactic to attract customers to a new product or service by offering a lower price during its initial release.

- A reduced price assists a new product or service in breaking into the market and luring customers away from competitors.

Question No.3

Match List I with List II:

| List I | Books | List II | Author(s) |

| (A) | Wealth of Nations, 1776 | (I) | Thomas Malthus |

| (B) | Principles of Political Economy and Taxation, 1817 | (II) | Karl Marx |

| (C) | Principle of Population, 1798 | (III) | Adam Smith |

| (D) | Das Capital, 1867 | (IV) | David Ricardo |

Choose the correct answer from the options given below:

- (A) – (I), (B) – (III), (C) – (IV), (D) – (II)

- (A) – (III), (B) – (IV), (C) – (I), (D) – (II)

- (A) – (II), (B) – (III), (C) – (I), (D) – (IV)

- (A) – (III), (B) – (I), (C) – (IV), (D) – (II)

Solutions:

The correct answer is (A) – (III), (B) – (IV), (C) – (I), (D) – (II)

The correct match is given below:

| List I | Books | List II | Author(s) |

| (A) | Wealth of Nations, 1776 | (III) | Adam Smith |

| (B) | Principles of Political Economy and Taxation, 1817 | (IV) | David Ricardo |

| (C) | Principle of Population, 1798 | (I) | Thomas Malthus |

| (D) | Das Capital, 1867 | (II | Karl Marx |

Important Points Wealth of Nations 1776:

- This is an important work of economic and social theory by Adam Smith, published in 1776.

- Its full title was Inquiry into the Nature and Causes of the Wealth of Nations.

- In it, he analysed the relationship between work and the production of a nation’s wealth.

- His conclusion was that encouraging free enterprise (an economic system in which there is unrestricted competition in industry and trade and no government control) leads to the optimum economic position.

Principles of Political Economy and Taxation, 1817:

- David Ricardo’s work, Principles of Political Economy and Taxation was published in April 1817.

- The book concludes that land rent rises in line with population growth.

- It also explains the comparative advantage hypothesis, which states that free trade between two or more countries can be mutually advantageous even if one country has an absolute advantage over the others in all areas of production.

Principle of Population, 1798:

- An Essay on the Principle of Population was first published anonymously in 1798, but Thomas Robert Malthus was soon identified as the author.

- The book warned in advance of future difficulties based on the assumption that population would increase in a geometric progression (doubling every 25 years) while food production would increase in an arithmetic progression, leaving a gap that would result in a lack of food and famine unless birth rates were reduced.

Das Capital, 1867:

- Das Kapital is a key work by Karl Marx (1818–83), a 19th-century economist and philosopher, in which he outlined his theory of the capitalist system, its dynamism, and its tendency toward self-destruction.

- His goal, he said, was to reveal “the economic rule of motion of modern civilization.”

- According to Marx, the existence of a massive army of unemployed, which he blamed on the capitalists, was what drove wages to subsistence levels, not population pressure.

- He claimed that in the capitalist system, labour was nothing more than a commodity that could

Question No.4

Factor conditions in Michael Porter’s competitive advantage of Nations include

- Market size

- Demand conditions

- Internationally competitive suppliers

- Skilled labour and scientific knowledge

Solutions:

The Correct answer is Skilled labour and scientific knowledge

Key Points

The Competitive Advantage Of Nations by Michael Porter:

- The Competitive Advantage of Nations is an economics book written by American author Michael E. Porter, a Harvard Business School professor and expert in corporate competitive strategy whose work is regularly quoted in business and economics.

- For Porter, the concept of national productivity is not a meaningful term because countries don’t compete like businesses do.

Important Points A four-factor system is used in Porter’s Diamond model to forecast or evaluate cluster activities:

1. Firm Strategy, Structure, and Rivalry:

A company’s structure and business strategy must align with the local business climate in order for it to grow. Direct rivalry with other businesses should encourage each company to use its skills and resources to boost innovation and productivity—and to outperform its local competitors.

2. Demand Conditions:

When customers in a local market expect high-quality, differentiated products, companies trying to meet those demands will be obliged to innovate in order to survive. As a result, a company that succeeds in a competitive and aggressively demanding local market will also succeed in the global market since its products have been fine-tuned.

3. Related and Supporting Industries:

All organizations rely on suppliers for parts, raw materials, and information exchange to some extent, and most companies engage in this cycle as both customers and providers. When a company’s supply chain firms are productive, high-quality enterprises with the potential to prosper in both the local and global market, the company’s efficiency, productivity, and innovation will improve as well.

4. Factor Conditions:

Factor conditions in Michael Porter’s competitive advantage of Nations include Skilled labour and scientific knowledge. This is a country’s situation in terms of production elements such as knowledge and infrastructure. These are important considerations in determining industry competitiveness. Material resources, people resources (labour expenses, credentials, and dedication), knowledge resources, and infrastructure are all elements to consider.

Question No.5

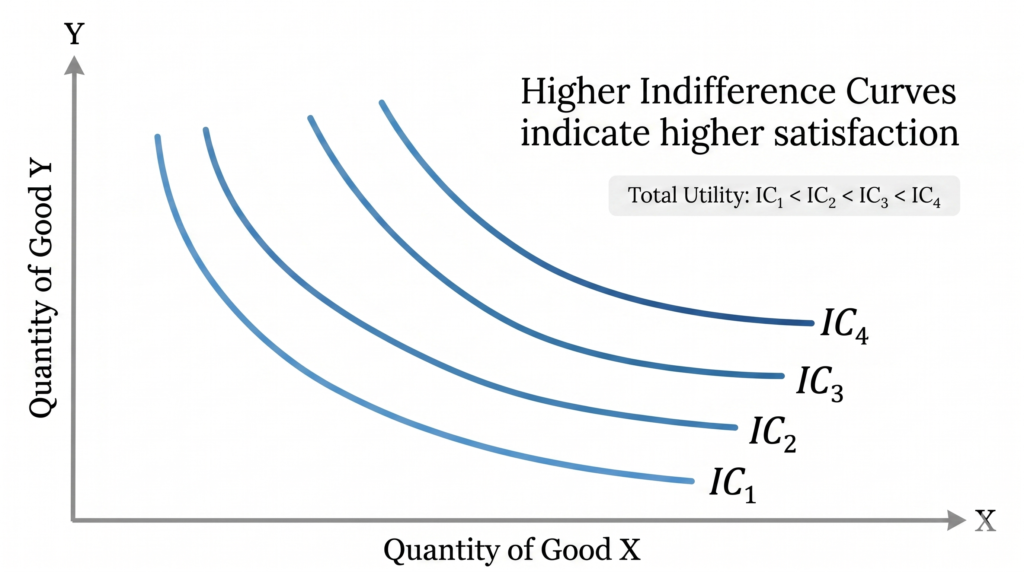

Why is an indifference curve convex to the origin?

(A) Indifference curve slope downward to the right

(B) Two commodities are imperfect substitutes

(C) Declining marginal rate of substitution between commodities

(D) Diminishing marginal utilities

Choose the most appropriate answer from the options given below:

- A and B only

- B and C only

- C and D only

- A and D only

Solutions:

The correct Answer is B and C

Key Points

Indifference curves:

- An indifference curve is a graph showing a combination of two goods that give the consumer equal satisfaction and utility.

- It shows a combination of two goods giving a consumer equal satisfaction making the consumer indifferent.

- A higher indifference curve represents a higher level of satisfaction because the higher Indifference Curve means a bundle comprising both the goods or the same quantity of one good and more quantity of the other good.

Important Points

Reasons for Indifference Curve being convex to the origin:

Two commodities are imperfect substitutes

- The downward-sloping curve indicates that when the amount of one commodity in the combination is increased, the amount of other commodities is reduced.

- This must be so if the level of satisfaction is to remain constant on the same indifference curve.

Declining marginal rate of substitution between commodities:

- When a consumer picks the substitute over another good, rather than simultaneously consuming more, marginal substitution is diminishing.

- MRS diminishes as one proceeds down a standard convex-shaped curve, which is the indifference curve, according to the law of diminishing marginal rates of substitution.

- This is one of the reason for the indifference curve being convex to the origin.

Question No.6

In Cobb-Douglas production function, Q = AKaLß increasing returns to scale occurs when

- a + b > 1

- K + L > 1

- a + b < 1

- K + L < 1

Solutions:

The correct answer is a + b > 1

Key Points Cobb-Douglas production function:

- The Cobb-Douglas production function is based on Paul H. Douglas and C.W. Cobb’s empirical analysis of the American manufacturing industry.

- It is a degree one linear homogeneous production function that considers two inputs, labour and capital, for the total output of the manufacturing industry.

- The Cobb-Douglas production function is expressed as Q = AKaLß

where Q is output and L and С are inputs of labour and capital, respectively. A, a and β are positive parameters where = a > O, β > O.

Important Points The Cobb Douglas production function exhibits the three types of returns:

- If a+b>1, there are increasing returns to scale.

- If a+b=1, we get constant returns to scale.

- If a+b<1, we get decreasing returns to scale.

Question No.7

The extreme case of non-price competition in an Oligopoly is

- Formation of cartels

- Interdependent decision-making

- Attaining economies of scale

- Formation of duopoly

Solutions:

The correct answer is Formation of cartels

Key Points

Oligopoly:

- An oligopoly is a market that is dominated by a few big companies. Only a few companies sell homogeneous or differentiated products in this sector.

- There are few sellers in the market, every seller influences the behaviour of the other firms and other firms influence it.

Non-price Competition:

Non-price competition is a marketing approach that emphasizes product distinctiveness and long-term competitive advantages over price reductions.

Important Points

- The extreme case of non-price competition in an Oligopoly is Formation of cartels.

- Collusion occurs when companies work together to decrease output and keep prices high.

- A cartel is a collection of companies that have made a formal agreement to work together to generate monopoly output and sell it at monopoly prices.

Question No.8

Characteristics constituting the core of consumer’s rationality includes:

(A) Homogeneous expectations

(B) Non-satiation

(C) Selfish motive

(D) Clarity of preferences

(E) Possession of information

Choose the correct answer from the options given below:

- A, B and C only

- B, C and D only

- A, B, C and D only

- B, C, D and E only

Solutions:

The correct answer is B, C, D and E only

Key Points A Rational Consumer:

- A rational consumer is an economic notion that assumes that while making a decision, people will always prioritise maximising their own personal gains.

- When making a selection, rational consumers choose the alternative that will provide them with the maximum utility and satisfaction.

Example: Consider the situation when a person has to choose between purchasing a more expensive car A or a less expensive car B. If the cars are identical, sensible consumers will choose car B since it will provide the maximum value for their money.

Important Points Assumptions of consumer rationality:

- Non-Satiation: The assumption that a consumer will always benefit from additional consumption. The demand for some goods may have a finite limit, but it is likely that there is some good or service a consumer would benefit from having more of.

- Clarity Of Preferences: This assumption states that, logically, selections between goods are rational because of the transitivity statement, which posits that people always prefer goods in the following order: A is preferred to B, and B is preferred to C, so A is preferred to C.

- Economic Selfish Motive: The notion that human behaviour is governed by selfishness as an ultimate motive – without altruism (selflessness) and group selection.

- Possession Of Information: The assumption states that a consumer has perfect and complete information, and he makes choices based on this information.

Question No.9

Given below are two statements:

Statement I : Only low priced products will sell in rural India.

Statement II : Rural consumers are a homogenous lot.

In the light of the above statements, choose the most appropriate answer from the options given below:

- Both Statement I and Statement II are correct.

- Both Statement I and Statement II are incorrect.

- Statement I is correct but Statement II is incorrect.

- Statement I is incorrect but Statement II is correct.

Solutions:

The correct answer is Both Statement I and Statement II are incorrect.

Key Points

Statement I : Only low priced products will sell in rural India.

This statement is incorrect because the statement assumes that the all people residing in rural India have low per capita income and cannot afford high priced products. This is an unrealistic assumption.

Statement II : Rural consumers are a homogenous lot.

This statement is also incorrect as most firms assume that rural markets are homogenous. It is unwise on the part of these firms to assume that the rural market can be served with the same product, price and promotion combination.

Question No.10

For a decline in price, total revenue declines if the demand of the product is

- Inelastic

- Elastic

- Unitary elastic

- Zero elastic

Solutions:

The correct answer is inelastic

Key Points Elasticity of Demand

- Price elasticity of demand is an economic measurement of how the quantity demanded of a good will be affected by changes in its price. In other words, it’s a way to figure out the responsiveness of consumers to fluctuations in price.

- When the price of a good or service influences consumer demand, this is known as elastic demand. Consumers will buy a lot more if the price drops just a little. If prices rise somewhat, they will reduce their purchases and wait for pricing to return to normal.

- Inelastic demand is a term that economists use to refer to a situation where demand for an item remains the same, no matter how far its price rises or falls.

Important Points

Total revenue is price multiplied by quantity demanded (TR = P x Qd).

Inelastic Demand case

In the inelastic demand, a one percent change in the price results in a less than one percent change in the quantity demanded. A price increase will therefore increase total revenue, while a price decrease will decrease total revenue.

Elastic Demand Case:

In the elastic demand, the percentage change in quantity demanded is greater than the percentage change in price, so raising the price in this region of the demand curve will decrease total revenue while lowering the price increases total revenue.

Question No.11

Arrange the following market structures in the increasing order of pricing power to firms.

(A) Monopolistic competition

(B) Perfect competition

(C) Duopoly

(D) Monopoly

(E) Oligopoly

Choose the correct answer from the options given below:

- (B), (D), (A), (E), (C)

- (B), (A), (E), (C), (D)

- (A), (C), (B), (D), (E)

- (D), (C), (E), (A), (B)

Solutions:

The correct answer is (B), (A), (E), (C), (D)

Key Points

Perfect competition:

The term “perfect competition” refers to a market structure in which competition is at its most intense. A market which exhibits the following characteristics in its structure is said to show perfect competition:

- Large number of buyers and sellers

- Homogenous product is produced by every firm

- Free entry and exit of firms

- Zero advertising cost

- No transportation costs

- Every firm is a price taker. It considers the price as determined by the forces of supply and demand. There is no way for a company to alter the product’s price.

Monopolistic competition:

Monopolistic competition is a market system that combines monopolistic and competitive market characteristics. A monopolistic competitive market is one that allows enterprises to differentiate their products while allowing them to enter and exit freely. A monopolistic competitive industry has the following features:

- Many firms.

- Freedom of entry and exit.

- Firms produce differentiated products.

- Firms have price inelastic demand; they are price makers because the good is highly differentiated

- Firms make normal profits in the long run but could make supernormal profits in the short term

- Firms are allocative and productively inefficient.

Oligopoly:

An oligopoly is a market with a few firms that recognise their pricing and output policies are interconnected. Since, the number of firms is small, each one has some market power. An oligopoly industry has the following features:

- A Few Firms with Large Market Share

- High Barriers to Entry

- Interdependent firms

- Oligopolies have combined market power, they tend to keep prices higher to obtain larger profits.

Duopoly:

A market system in which there are just two sellers is known as a duopoly (producers). This is the most fundamental type of oligopoly competition. The two players sell competing goods and services to multiple buyers. Characteristics of duopoly:

- Market consists of two producers

- Producers have a high strategic dependence.

- Chances of collusive behaviour are high.

- The level of competition may be fierce.

- It is advantageous for them to band together and set prices and individual outputs at levels that maximise their combined earnings.

Monopoly:

A monopoly is a market structure that consists of a single seller who has exclusive control over a commodity or service. A monopoly displays characteristics that are different from other market structures:

- Single seller

- No close substitutes

- Barriers to entry

- Price maker – A monopolist has the power to charge any price for its product or service.

Discover more from WebComm.in

Subscribe to get the latest posts sent to your email.