Learning Inside

MEANING OF THE ACCOUNTING STANDARDS #

NATURE OF ACCOUNTING STANDARDS #

UTILITY OF ACCOUNTING STANDARDS #

Let’s dive into it..

The rise in diversity, complexity and globalisation of business, made the study of accounting information essential. But the diversity in the accounting policies being followed and the accounting treatment of transactions and events made the accounting information less meaningful and also incomparable. A need was thus felt that certain minimum standards should be universally applicable, so that the accounting statements have the qualitative characteristics of reliability, relevance, understandability and comparability. As a step towards this, and International Accounting Standard Committee (IASC) (now renamed as International Financial Reporting Committee) was set-up in the year 1973. The objectives of this committee are:

- To formulate and publish in public interest, Accounting Standards to be observed in the presentation of Financial Statements and also their worldwide acceptance; and

- To work for the improvement and harmonisation of regulation of Accounting Standards and procedures relating to the presentation of financial transactions.

The Institute of Chartered Accountants of India and the Institute of Cost and Works Accountants of India are members of this committee.

The Institute of Chartered Accountants of India, in April 1977, set-up the Accounting Standards Board (ASB) to identify areas of accounting where alternative and diverse practices were followed. ASB, with a purpose to bring uniformity in practices, was assigned the task of developing draft Accounting Standards Keeping in view the legal provisions of the country and after discussions with Government Representative, Public Sector Undertakings, Industry Federations, etc. While framing the draft Accounting Standards, ASB considers the International Accounting Standards also.

ASB submits the draft Accounting Standards to the Council, the Institute of Chartered Accountants of India which issues it for the comment of the government, industry and professionals, etc. The council of the Institute of Chartered Accountants of India gives due consideration to the comments received by amending the draft Accounting Standards, if necessary, before notifying it.

MEANING OF THE ACCOUNTING STANDARDS

The Accounting Standards are a set of guidelines, i.e., Generally Accepted Accounting Principles, issued by the accounting body of the country such as The Institute of Chartered Accountants of India, that are followed for preparation and presentation of Financial Statements. They are accounting rules and procedures relating to measurement, valuation and disclose issued by the council of the Institute of Chartered Accountants of India.

Kohler has defined Accounting Standards as, “a mode of conduct imposed on an accountant by custom, law and a professional body.”

NATURE OF ACCOUNTING STANDARDS

Following points highlight the nature of Accounting Standards:

- Accounting Standards are guidelines providing the framework so that credible Financial Statements can be produced.

- The objective of setting Accounting Standards is to bring uniformity in accounting practices and to ensure transparency, consistency and comparability.

- Accounting Standards are prepared keeping in view the business environment and laws of the country. It, therefore, naturally means that the guidelines change with change in business environment and laws. It is because of this that Accounting Standards are being revised from time to time. It may be noted that whenever a conflict arises between law and Accounting Standards, law will prevail.

- Accounting Standards are mandatory in nature.

- Accounting Standards have also been made flexible in the sense that where alternative accounting practices are acceptable, an enterprise is free to adopt any of the practices with a suitable disclosure. In case the enterprise chooses to change the practice followed, the effect of such change must be quantified and disclosed. An example of this would be the method of depreciation charged. An enterprise may charge depreciation on the Written Down Value Method or Straight-Line Method.

UTILITY OF ACCOUNTING STANDARDS

Accounting Standards serve the following purposes:

- Accounting Standards provide the norms on the basis of which financial statement should be prepared.

- Accounting Standards ensure uniformity in the preparation and presentation of financial statements by removing the effect of diverse accounting practices. The application of Accounting Standards make financial statements more meaningful and comparable.

- Accounting Standards create a sense of confidence among the users of accounting information. Accounting information created by applying Accounting Standards is considered reliable by users of such information.

- Accounting Standards help auditors in auditing the accounts. They help accountants to follow uniform practices and policies.

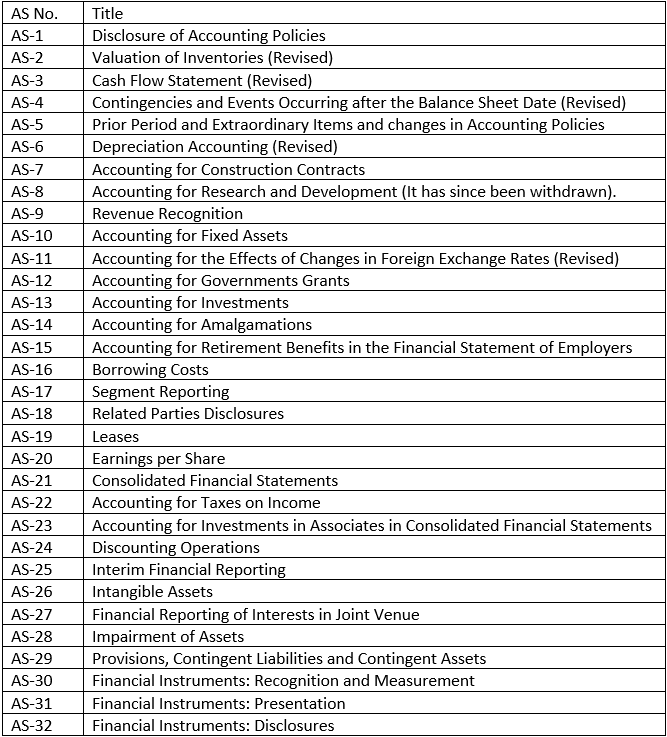

The Council of Institute of Chartered Accountants of India has so far issued thirty-two Accounting Standards (AS). These Accounting Standards are mandatory in the sense that these are binding on the members of the Institute. These standards are as follows: