TS Grewal Double Entry Book Keeping Class 12 Solutions Volume1: Accounting for Partnership Firms

TS Grewal Accountancy Class 12 Solutions Chapter 1 Financial Statements of Not-for-Profit Organisations are part of TS Grewal Accountancy Class 12 Solutions.

| Board | CBSE |

| Textbook | NCERT |

| Book | Accounting for Partnership Firms |

| Volume | I |

| Class | 12th |

| Subject | Accountancy |

| Chapter | 1 |

| Chapter Name | Financial Statements of Not-for-Profit Organisations |

| Number of Questions (Solved) | 54 |

| Category | TS Grewal’s Solutions |

TS Grewal Accountancy Class 12 Solutions – Chapter 1th Financial Statements of Not-for-Profit Organisations

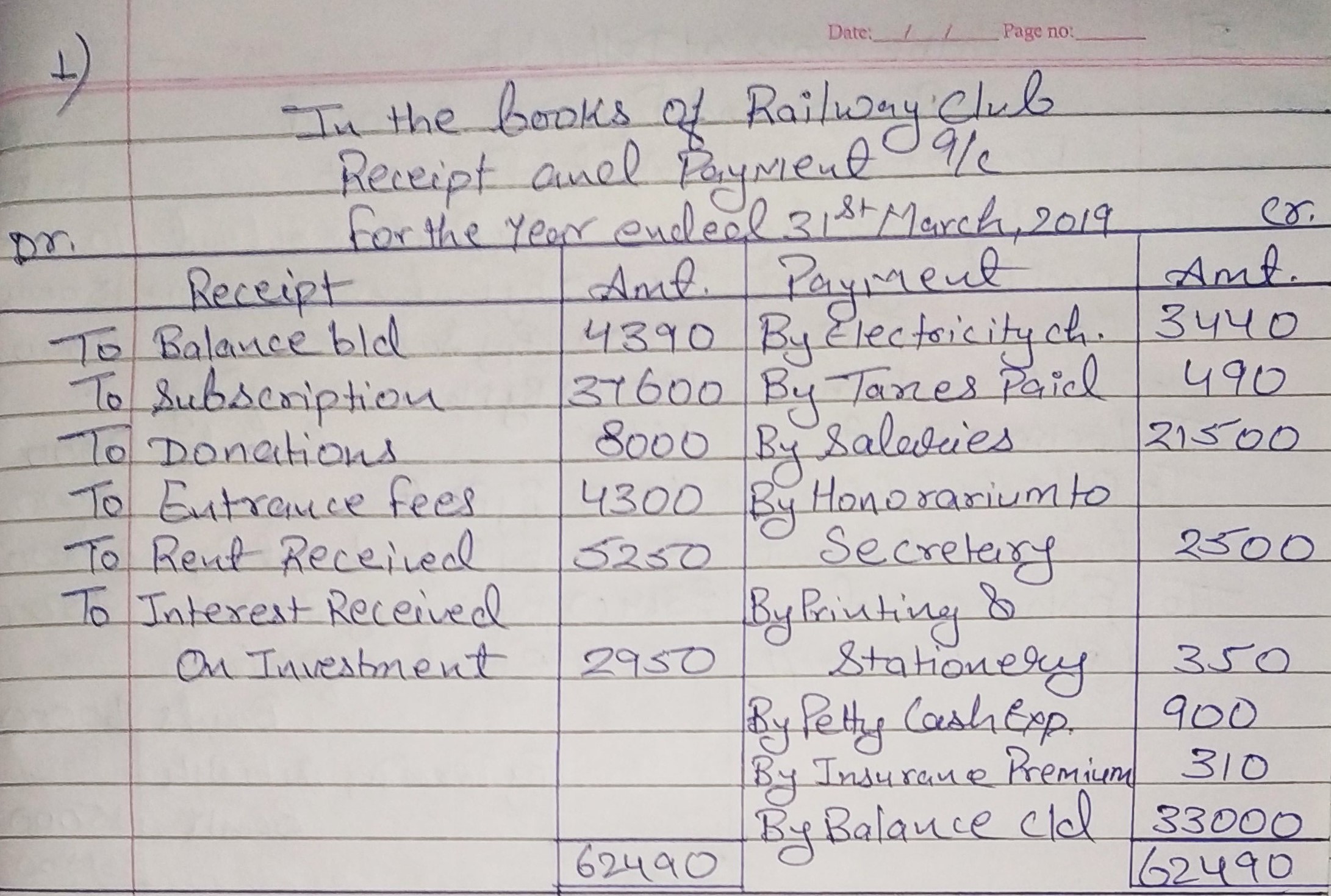

Question 1:

From the information given below, prepare Receipts and Payments Account of Railway Club for the year ended 31st March, 2019:

(₹) |

| (₹) | ||

| Cash in Hand on 1st April, 2018 | 4,390 | Salaries | 21,500 | |

| Subscription | 37,600 | Honorarium to Secretary | 2,500 | |

| Donations | 8,000 | Interest Received on Investments | 2,950 | |

| Entrance Fees | 4,300 | Printing and Stationery | 350 | |

| Rent Received for Club Halls | 5,250 | Petty Cash Expenses | 900 | |

| Electricity Charges | 3,440 | Insurance Premium Paid | 310 | |

| Taxes paid | 490 | |||

ANSWER:

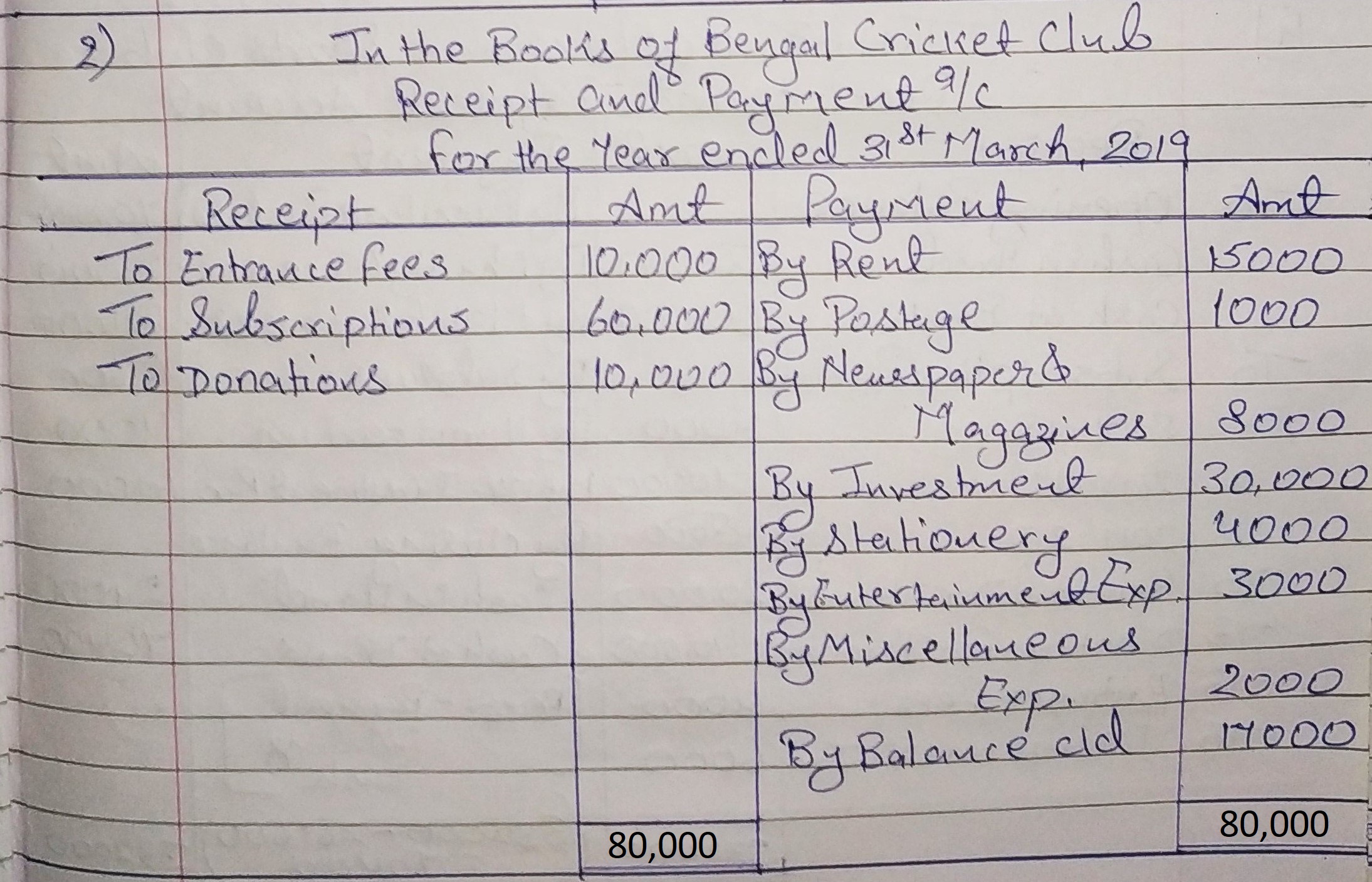

Question 2:

Bengal Cricket Club was inaugurated on 1st April, 2018. It had the following Receipts and Payments during the year ended 31st March, 2019:

Receipts: Entrance Fees ₹ 10,000; Subscriptions ₹ 60,000; Donations ₹ 10,000.

Payments: Rent ₹ 15,000; Postages ₹ 1,000; Newspapers and Magazines ₹ 8,000; Investments ₹ 30,000; Stationery ₹ 4,000; Entertainment Expenses ₹ 3,000; Miscellaneous Expenses ₹ 2,000.

Show the Receipts and Payments Account for the year ended 31st March, 2019.

ANSWER:

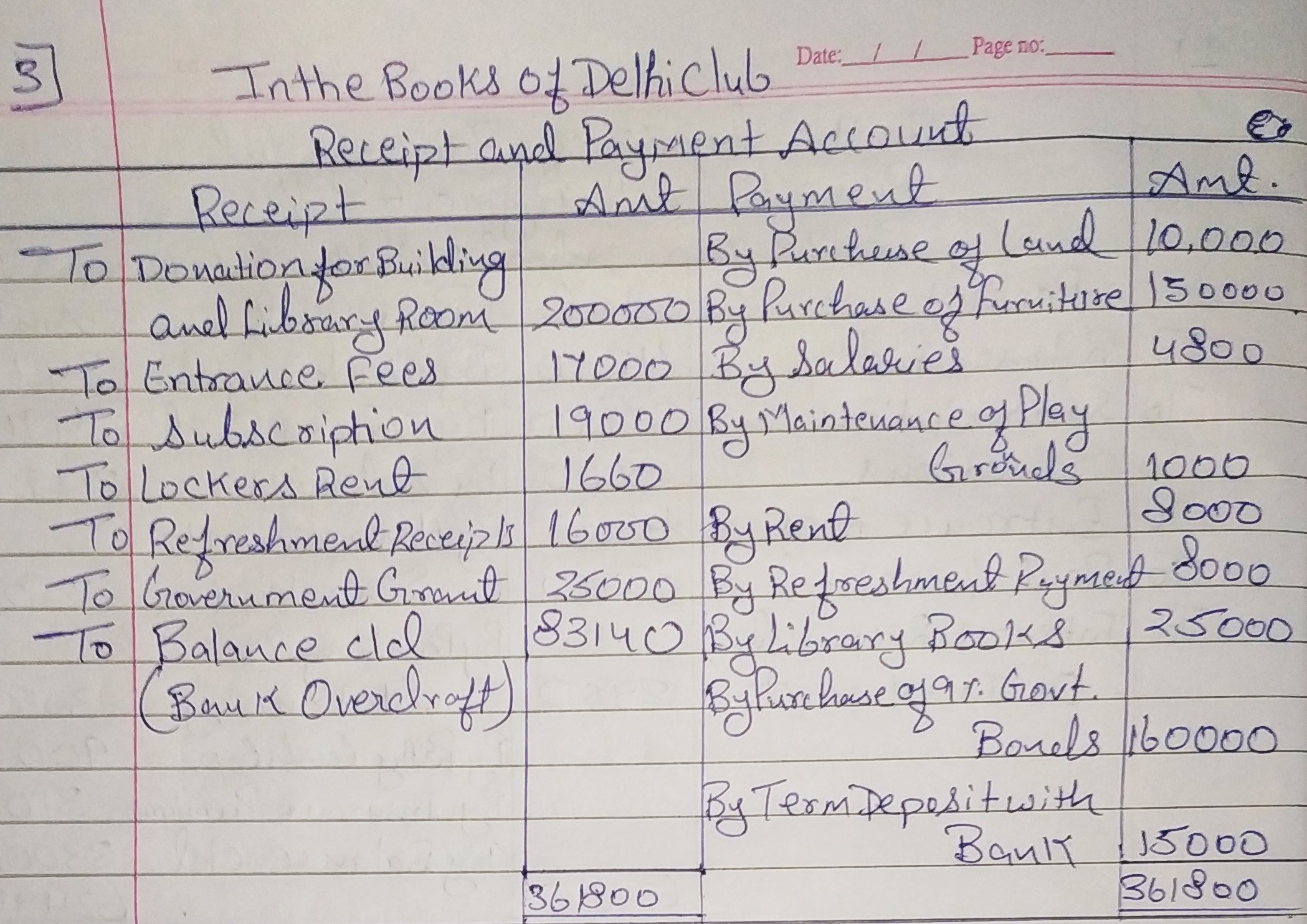

Question 3:

The following information were obtained from the books of Delhi Club as on 31st March, 2019 at the end of the first year of the Club, prepare Receipts and Payment Account for the year ending 31st March, 2019:

| Receipts | (₹) | Payments | (₹) | |

| Donation for Building and Library Room | 2,00,000 | Purchase of Land | 10,000 | |

| Entrance Fees | 17,000 | Purchase of Furniture | 1,30,000 | |

| Subscription | 19,000 | Salaries | 4,800 | |

| Lockers Rent | 1,660 | Maintenance of Play Grounds | 1,000 | |

| Refreshment Receipts | 16,000 | Rent | 8,000 | |

| Government Grant | 25,000 | Refreshment Payments | 8,000 | |

| Library Books | 25,000 | |||

| Purchase of 90% Government Bonds | 1,60,000 | |||

| Term Deposit with Bank | 15,000 | |||

ANSWER:

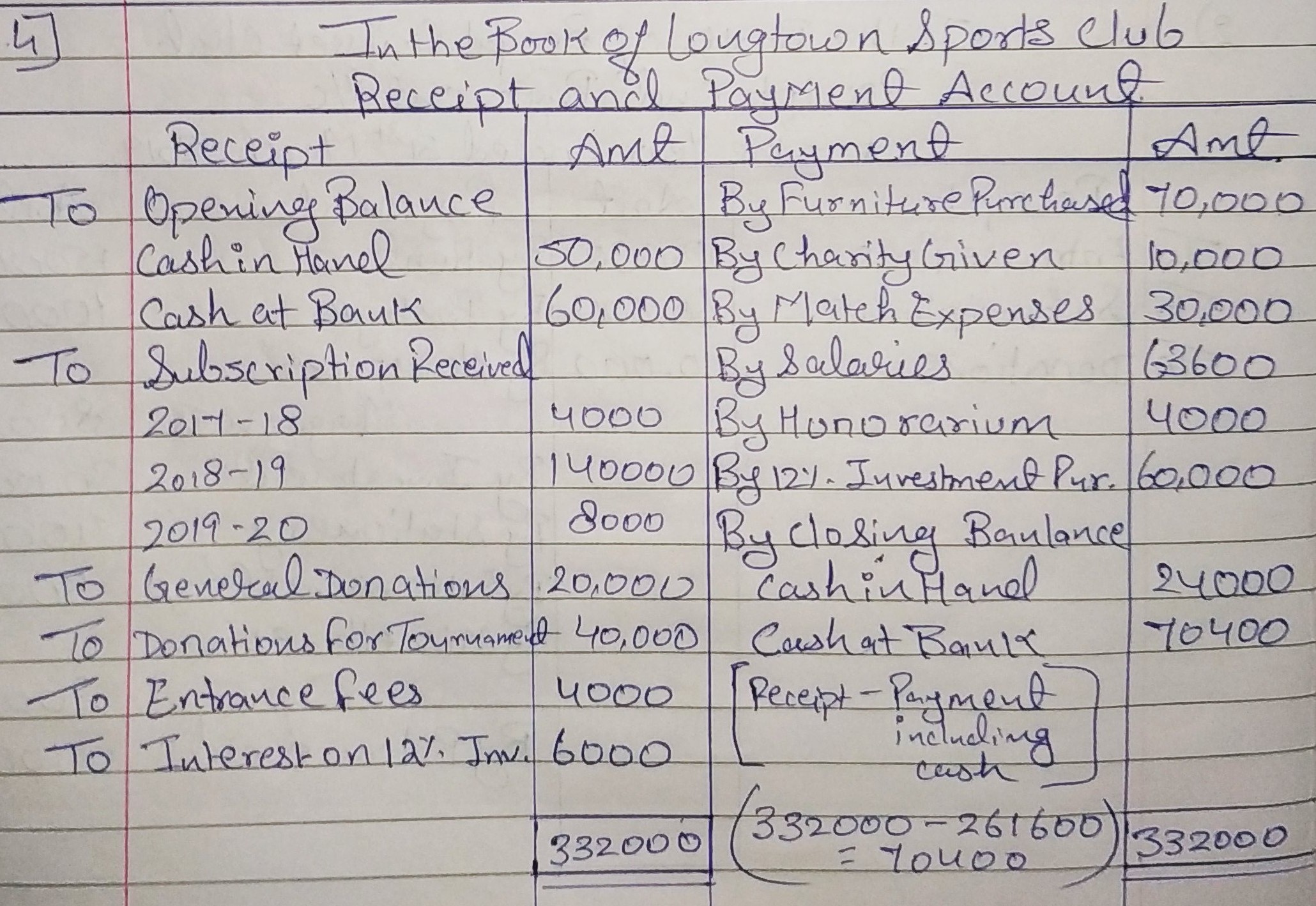

Question 4:

From the following information, prepare Receipts and Payments Account of Long-town Sports Club for the year ending 31st March, 2019:

| Particulars | (₹) | Particulars | (₹) | |

| Opening Balance: | Charity Given | 10,000 | ||

| Cash in Hand | 50,000 | Match Expenses | 30,000 | |

| Cash at bank | 60,000 | Salaries | 63,600 | |

| Subscription Received: | Honorarium | 4,000 | ||

| 2017-18 | 4,000 | 12% Investment Purchased | 60,000 | |

| 2018-19 | 1,40,000 | Entrance Fees | 4,000 | |

| 2019-20 | 8,000 | Interest on 12% Investments | 6,000 | |

| Furniture Purchased | 70,000 | Closing Balance: | ||

| General Donations | 20,000 | Cash in Hand | 24,000 | |

| Donations for Tournament | 40,000 | Cash at Bank | ? | |

ANSWER:

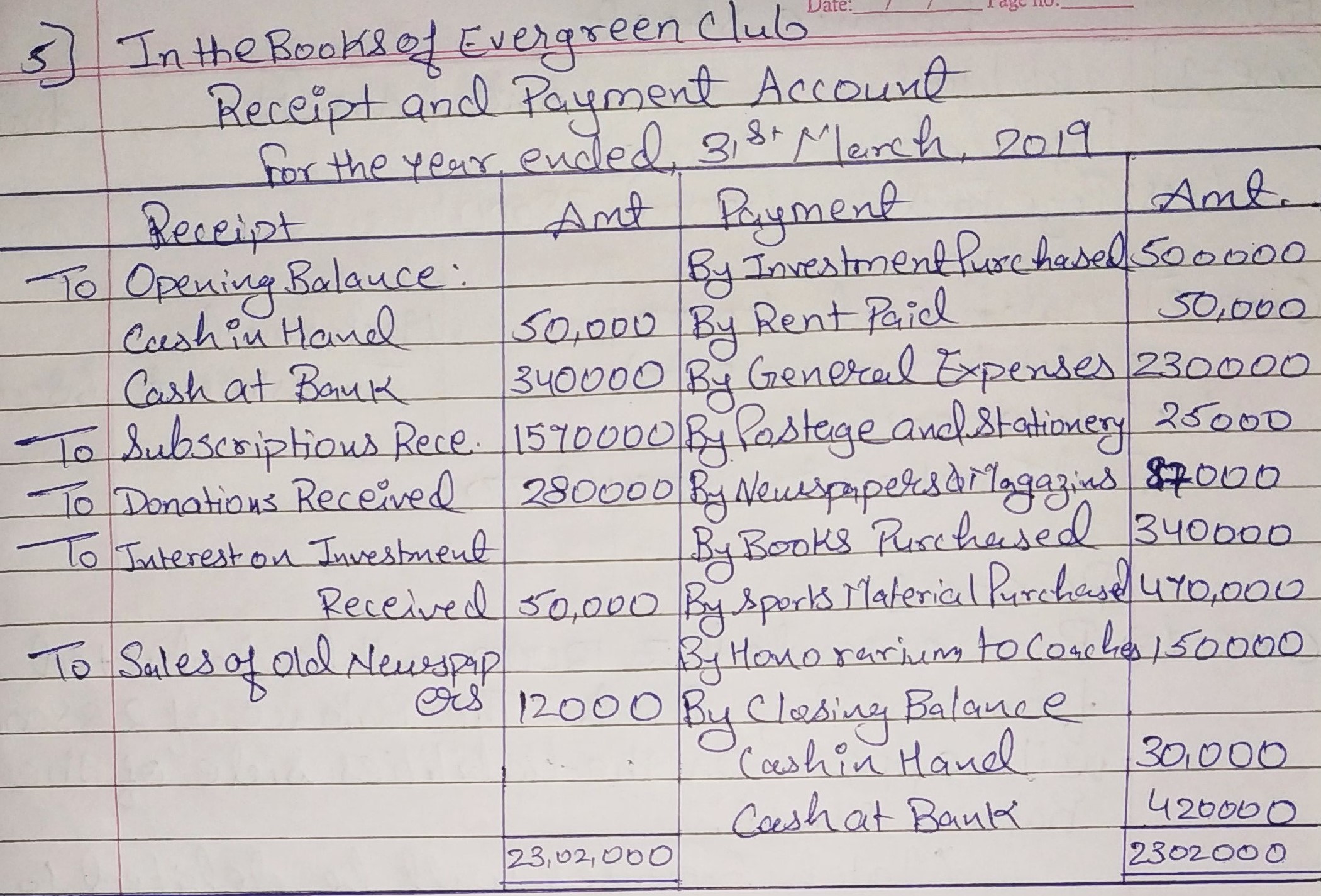

Question 5:

From the following particulars of Evergreen club, prepare Receipts and payments Account for the year ended 31st March,2019:

(₹) |

| (₹) | ||

| Cash in Hand on 1st April,2018 | 50,000 | Newspaper and Magazines | 87,000 | |

| Cash at Bank on 1st April,2018 | 3,40,000 | Sale of Old Newspaper | 12,000 | |

| Subscriptions Received | 15,70,000 | Books Purchased | 3,40,000 | |

| Donations Received | 2,80,000 | Sports Materials Purchased | 4,70,000 | |

| Investments purchased | 5,00,000 | Interest on Investments Received | 50,000 | |

| Rent paid | 50,000 | Honorarium to coaches | 1,50,000 | |

| General Expenses | 2,30,000 | Cash in Hand on 31st March,2019 | 30,000 | |

| Postage and stationery | 25,000 | Cash at Bank on 31st March ,2019 | ? | |

ANSWER:

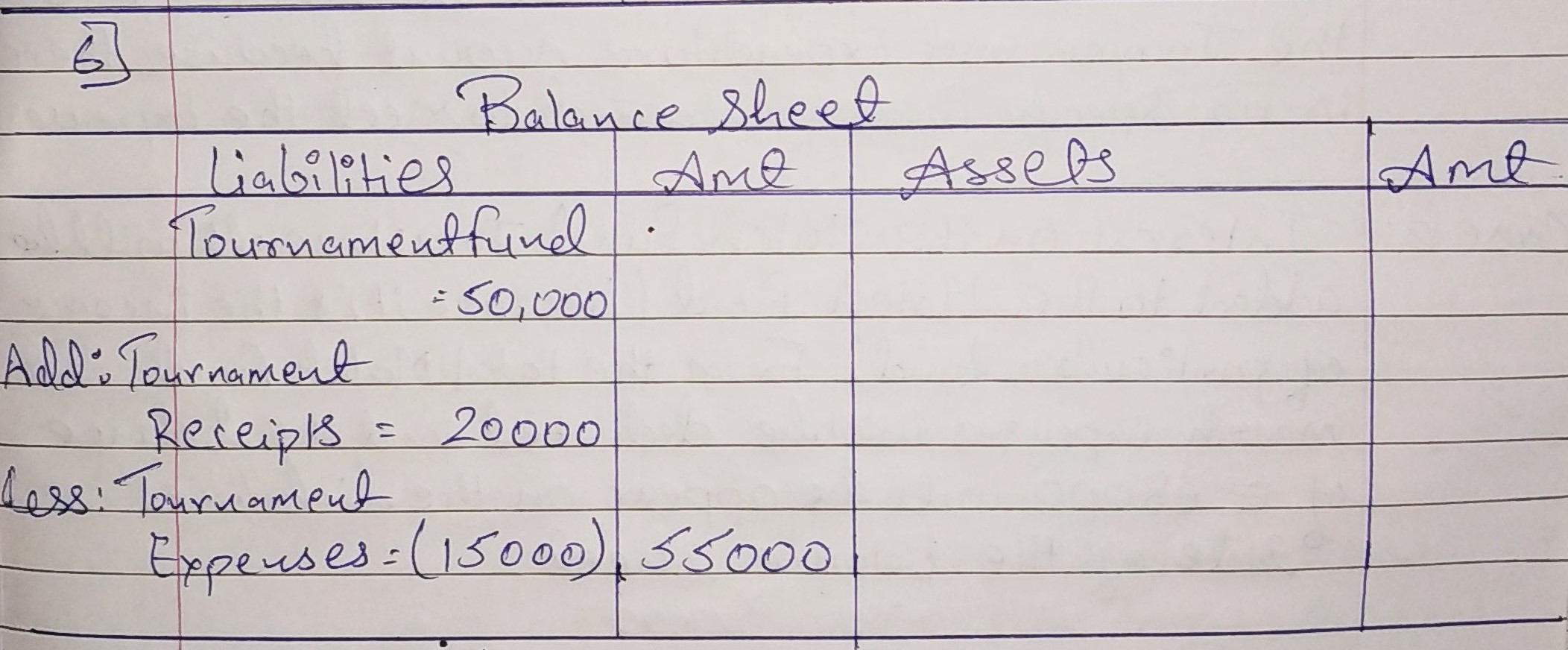

Question 6:

How are the following items shown in the accounts of a Not-for-Profit Organisation ?

| Particular | ₹ |

| Tournament Fund | 50,000 |

| Tournament Expenses | 15,000 |

| Receipts from Tournament | 20,000 |

ANSWER:

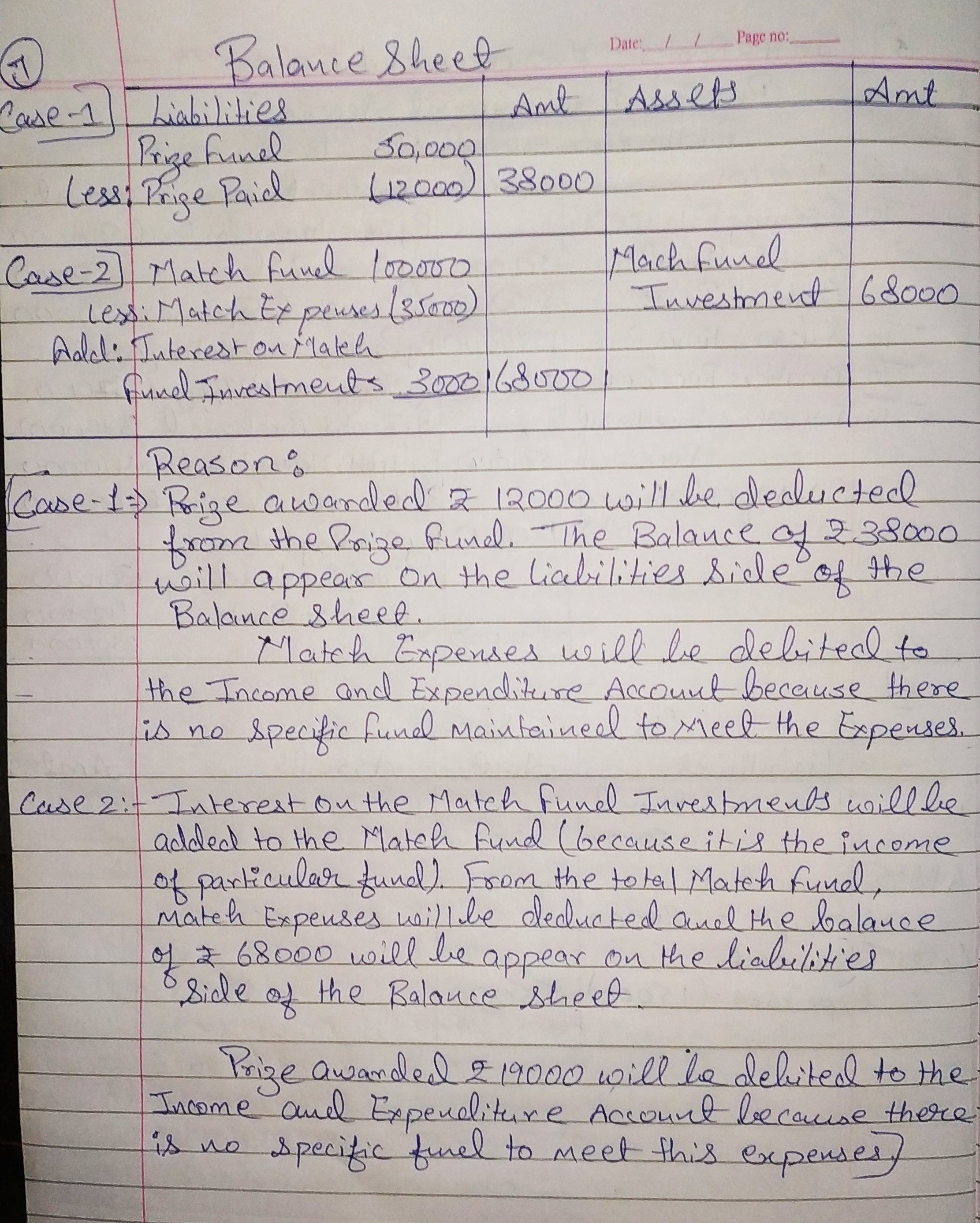

Question 7:

How are the following dealt with in the accounts of a Not-for-Profit Organisation ?

Case I | Dr. (₹) | Cr. (₹) | Case II | Dr. (₹) | Cr. (₹) |

| Prize Fund Prizes Paid Match Expenses | 12,000 15,000 | 50,000 | Match Fund Match Expenses Investments of Match Fund Interest on Match Fund Investments Prizes Paid | 35,000 60,000 19,000 | 1,00,000 3,000 |

ANSWER:

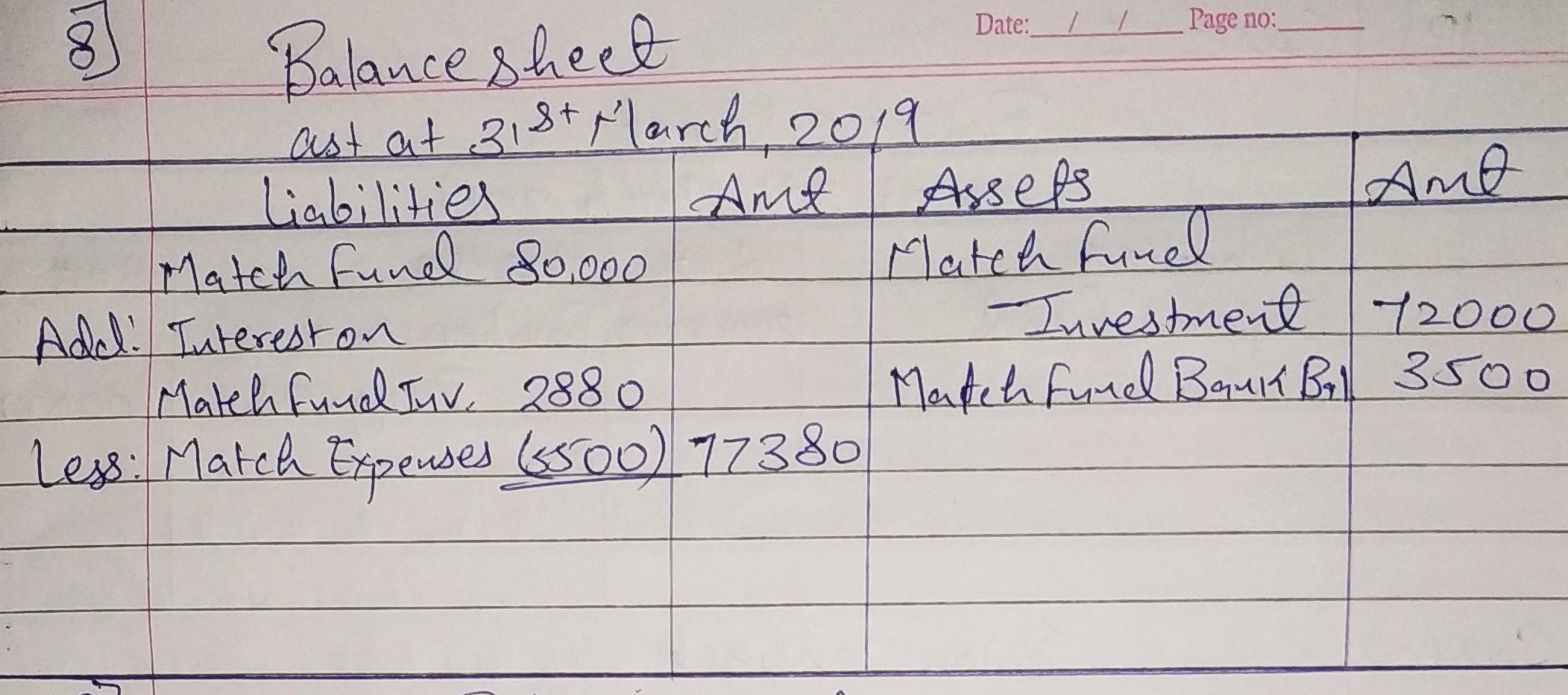

Question 8:

How are the following dealt with while preparing the final accounts of a club?

Particulars | Dr. (₹) | Cr. (₹) |

| Match Fund | …… | 80,000 |

| Match Fund Investments | 72,000 | …. |

| Match Fund Bank Balance | 3,500 | …. |

| Interest on Match Fund Investments | ….. | 2,880 |

| Match Expenses | 5,500 | …. |

ANSWER:

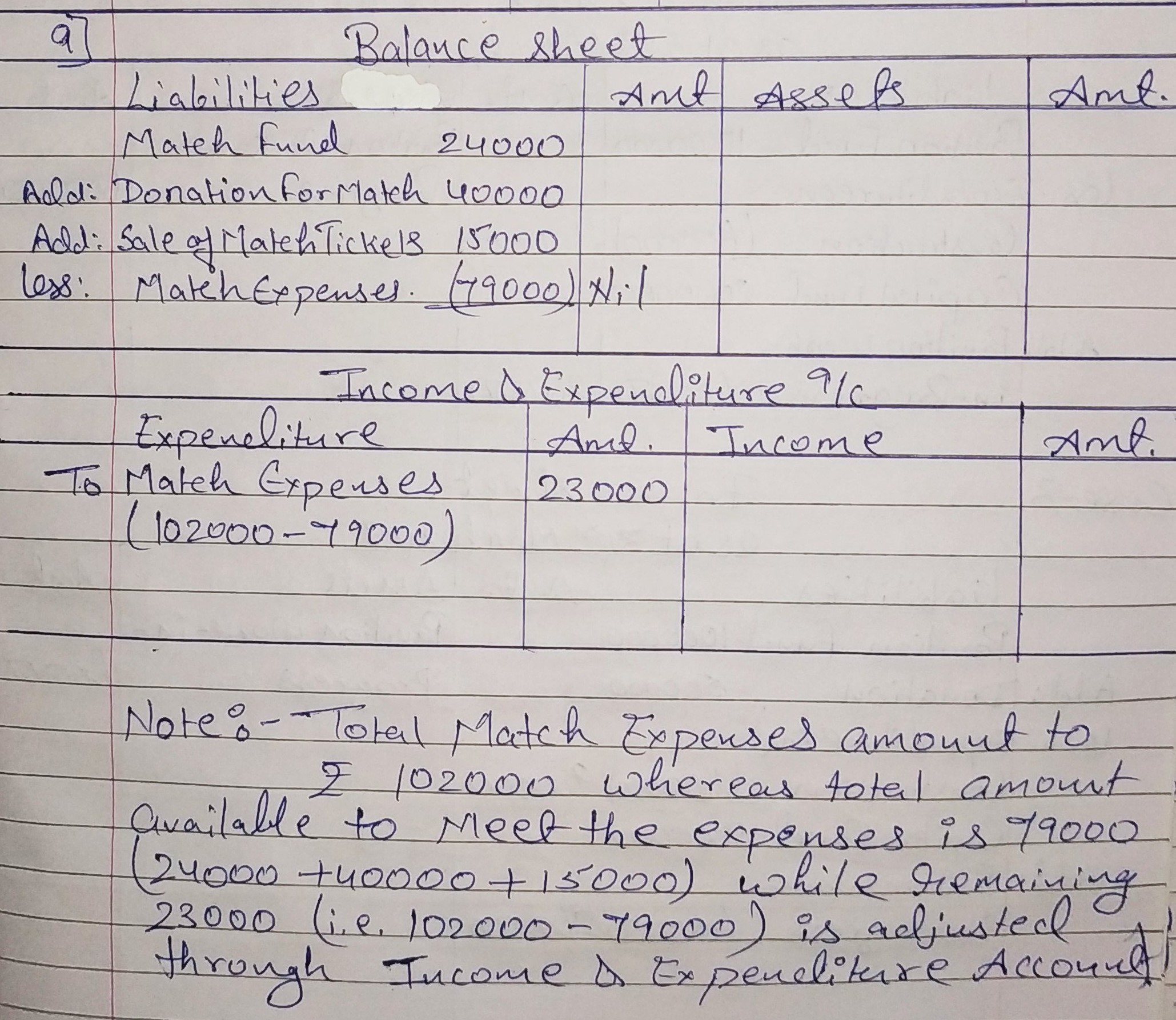

Question 9:

From the following information of a club show the amounts of match expenses and match fund in the appropriate Financial Statements of the club for the year ended on 31st March, 2019:

Particulars | ₹ |

| Match expenses paid during the year ended 31st March, 2019 | 1,02,000 |

| Match Fund as on 31st March, 2019 | 24,000 |

| Donation for Match Fund (Received during the year ended 31st March, 2019) | 40,000 |

| Proceeds from the sale of match tickets (Received during the year ended 31st March, 2019) | 15,000 |

ANSWER:

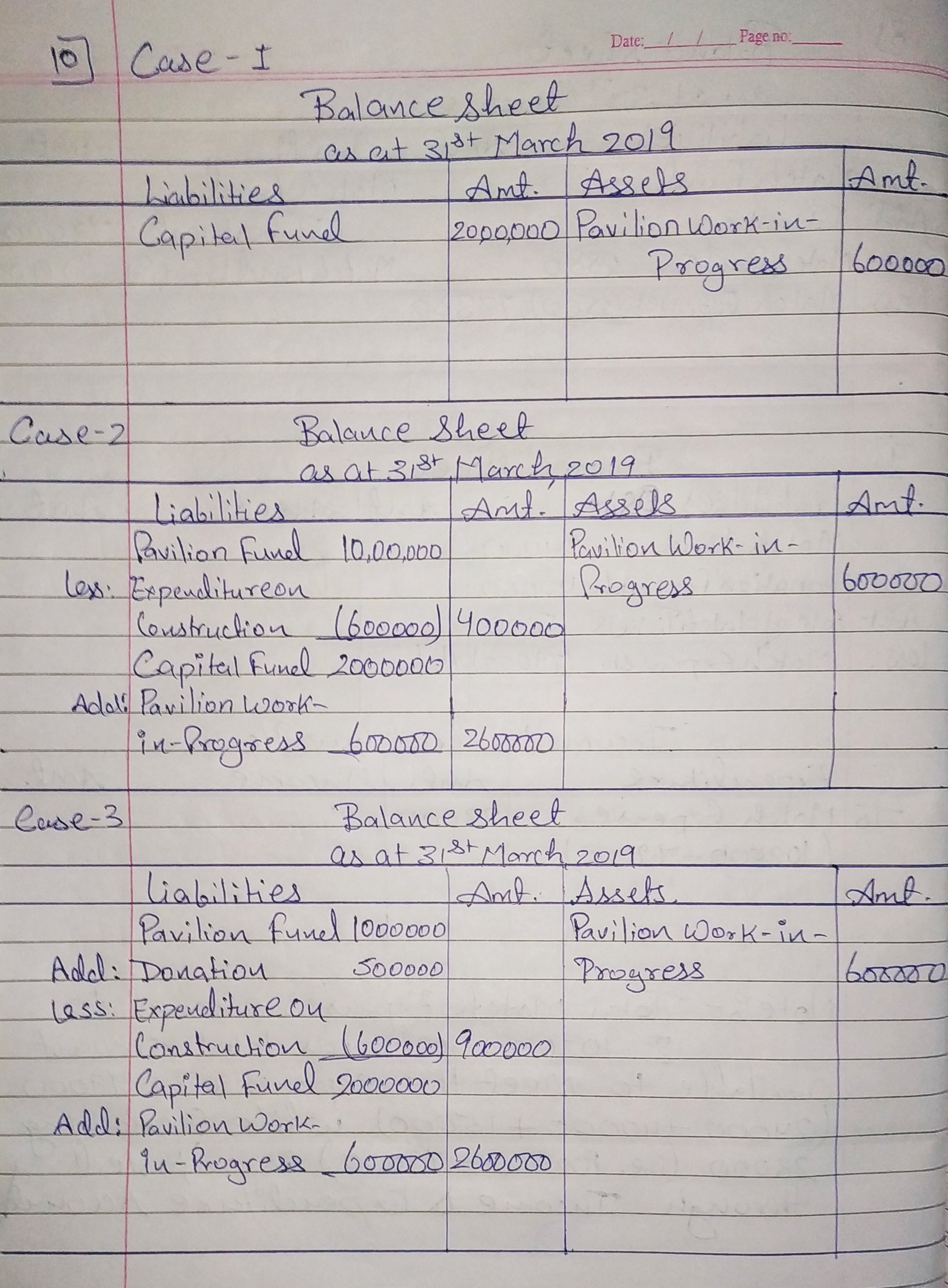

Question 10:

Show how are the following items dealt with while preparing the final accounts for the year ended 31st March, 2019 of a Not-for-profit Organisation:

Case I

Expenditure on construction of Pavilion is ₹ 6,00,000. The construction work is in progress and has not yet completed. Capital Fund as at 31st March, 2018 is ₹ 20,00,000.

Case II

Expenditure on construction of Pavilion is ₹ 6,00,000. The construction work is in progress and has not yet completed. Pavilion Fund as at 31st March, 2018 is ₹ 10,00,000 and Capital Fund as at 31st March, 2018 is ₹ 20,00,000.

Case III

Expenditure on construction of Pavilion is ₹ 6,00,000. The construction work is in progress and has not yet completed. Pavilion Fund as at 31st March, 2018 is ₹ 10,00,000, and Capital Fund as at 31st March, 2018 is ₹ 20,00,000. Donation Received for Pavilion on 1st January, 2019 is ₹ 5,00,000.

ANSWER:

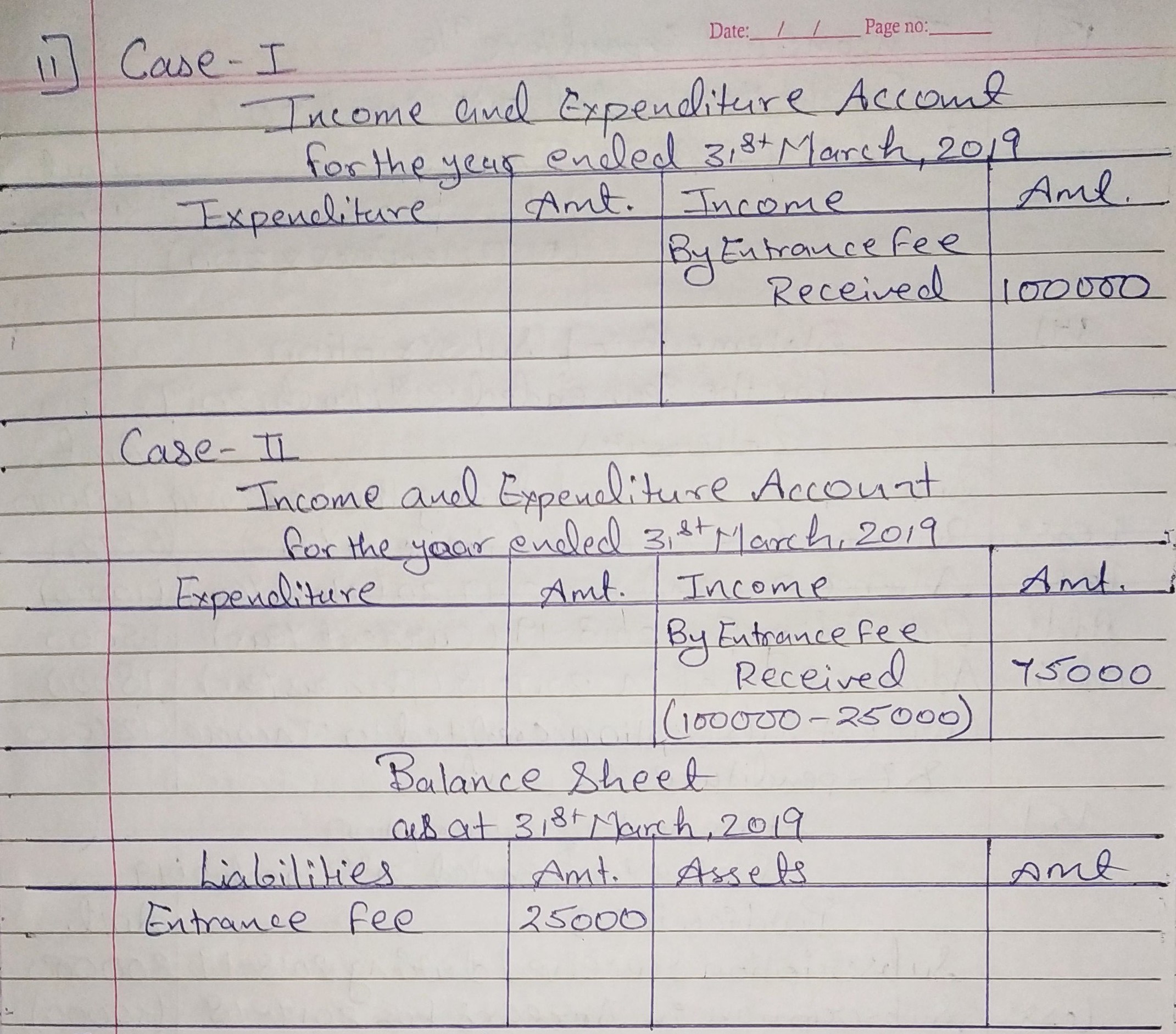

Question 11:

How is Entrance Fees dealt with while preparing the final accounts for the year ended 31st March, 2019 in each of the following alternative cases?

Case I During the year ended 31st March, 2019, Entrance Fees received was ₹ 1,00,000.

Case II During the year ended 31st March, 2019, Entrance Fees received was ₹ 1,00,000.Out of this, ₹ 25,000 was received from individuals whose membership is not yet approved.

ANSWER:

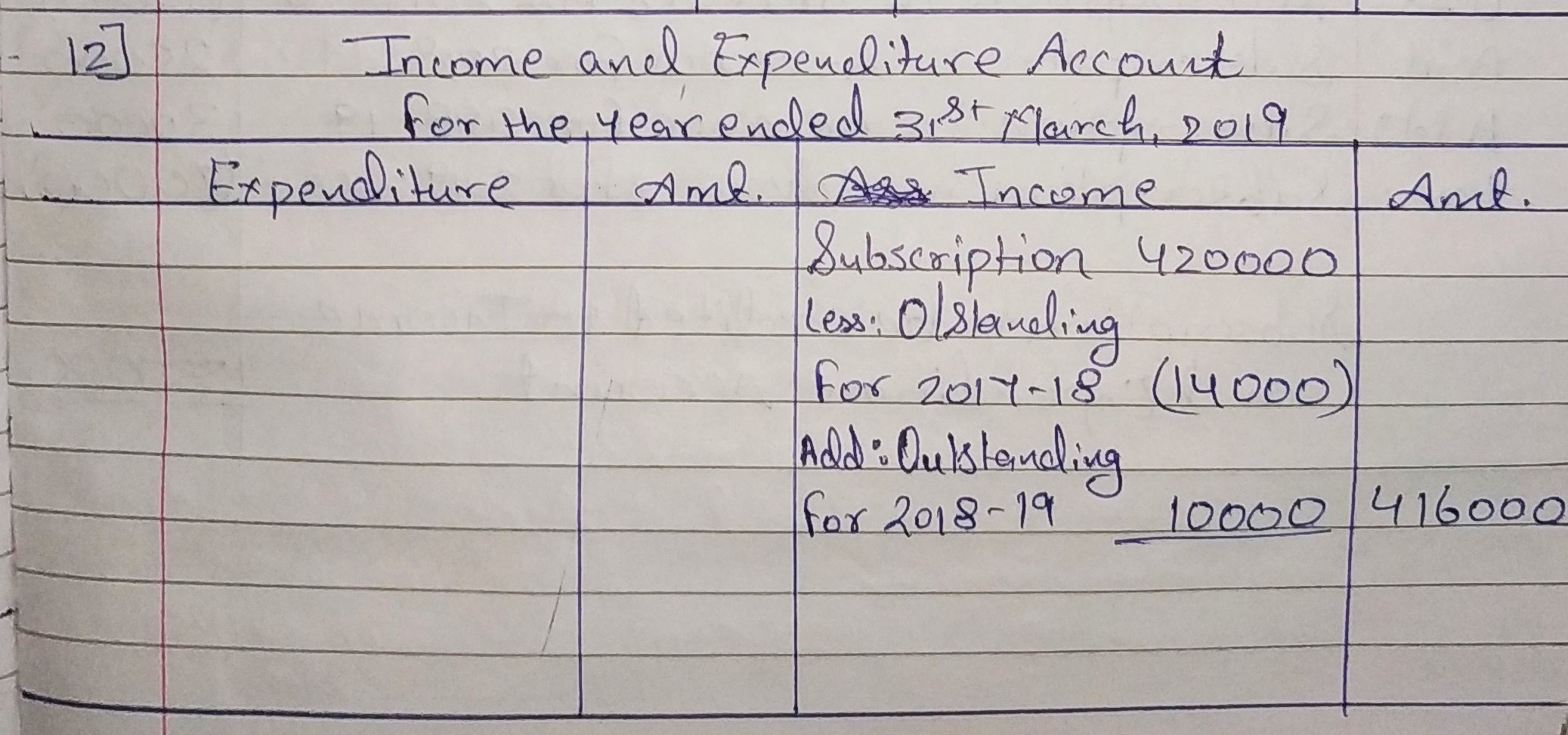

Question 12:

In the year ended 31st March, 2019, subscriptions received by the Jaipur Literary Society were ₹ 4,20,000. These subscriptions include ₹ 14,000 received for the year ended 31st March, 2018. On 31st March, 2019, subscriptions due but not received were ₹ 10,000. What amount should be credited to Income and Expenditure Account for the year ended 31st March, 2019 as subscription?

ANSWER:

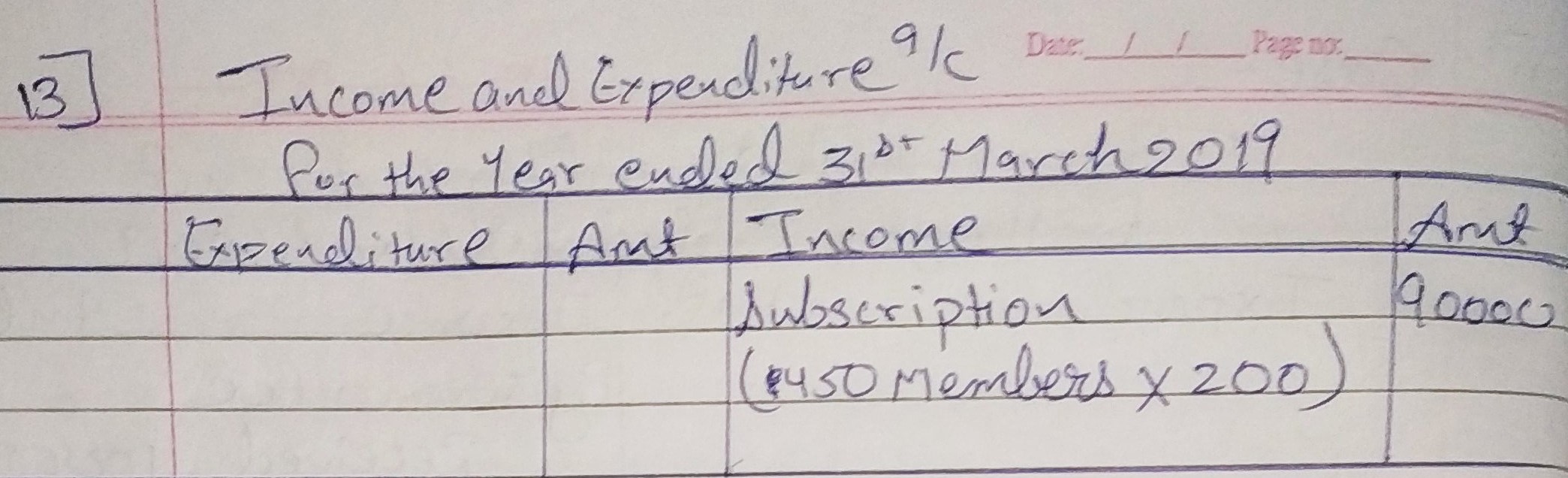

Question 13:

| Subscriptions received during the year ended 31st March , 2019 are: | ₹ | ₹ |

| For the year ended 31st March, 2018 | 1,600 | |

| For the year ended 31st March, 2019 | 84,400 | |

| For the year ended 31st March, 2020 | 3,200 | 89,200 |

There are 450 members, each paying an annual subscription of ₹ 200; ₹ 1,800 were in arrears for the year ended 31st March, 2018.

Calculate amount of subscriptions to be credited to Income and Expenditure Account for the year ended 31st March, 2019.

ANSWER:

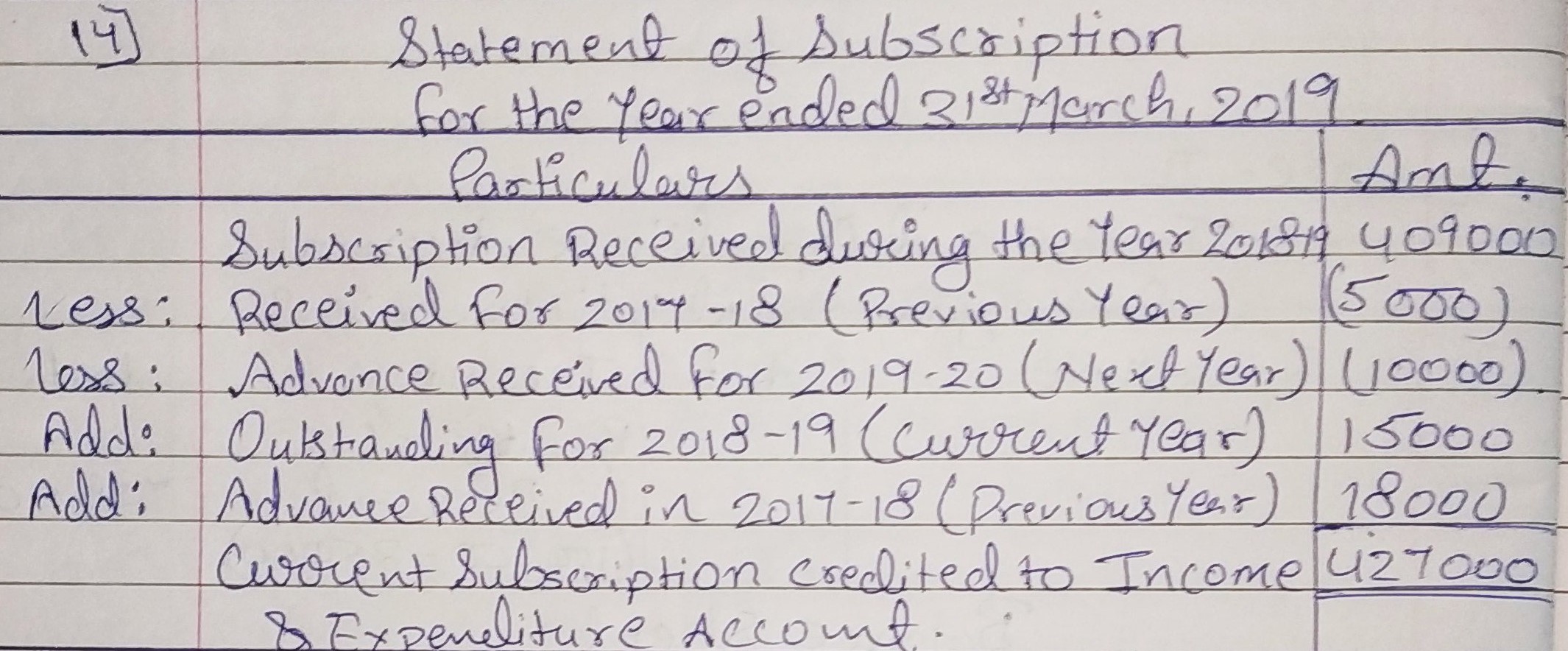

Question 14:

In the year ended 31st March, 2019, subscriptions received by Kings Club, Delhi were ₹ 4,09,000 including ₹ 5,000 for the year ended 31st March, 2018 and ₹ 10,000 for the year ended 31st March, 2020. At the end of the year ended 31st March, 2019, subscriptions outstanding for the year ended 31st March, 2019 were ₹ 15,000. The subscriptions due but not received at the end of the previous year, i.e., 31st March, 2018 were ₹ 8,000, while subscriptions received in advance on the same date were ₹ 18,000.

Calculate amount of subscriptions to be credited to Income and Expenditure Account for the year ended 31st March, 2019.

ANSWER:

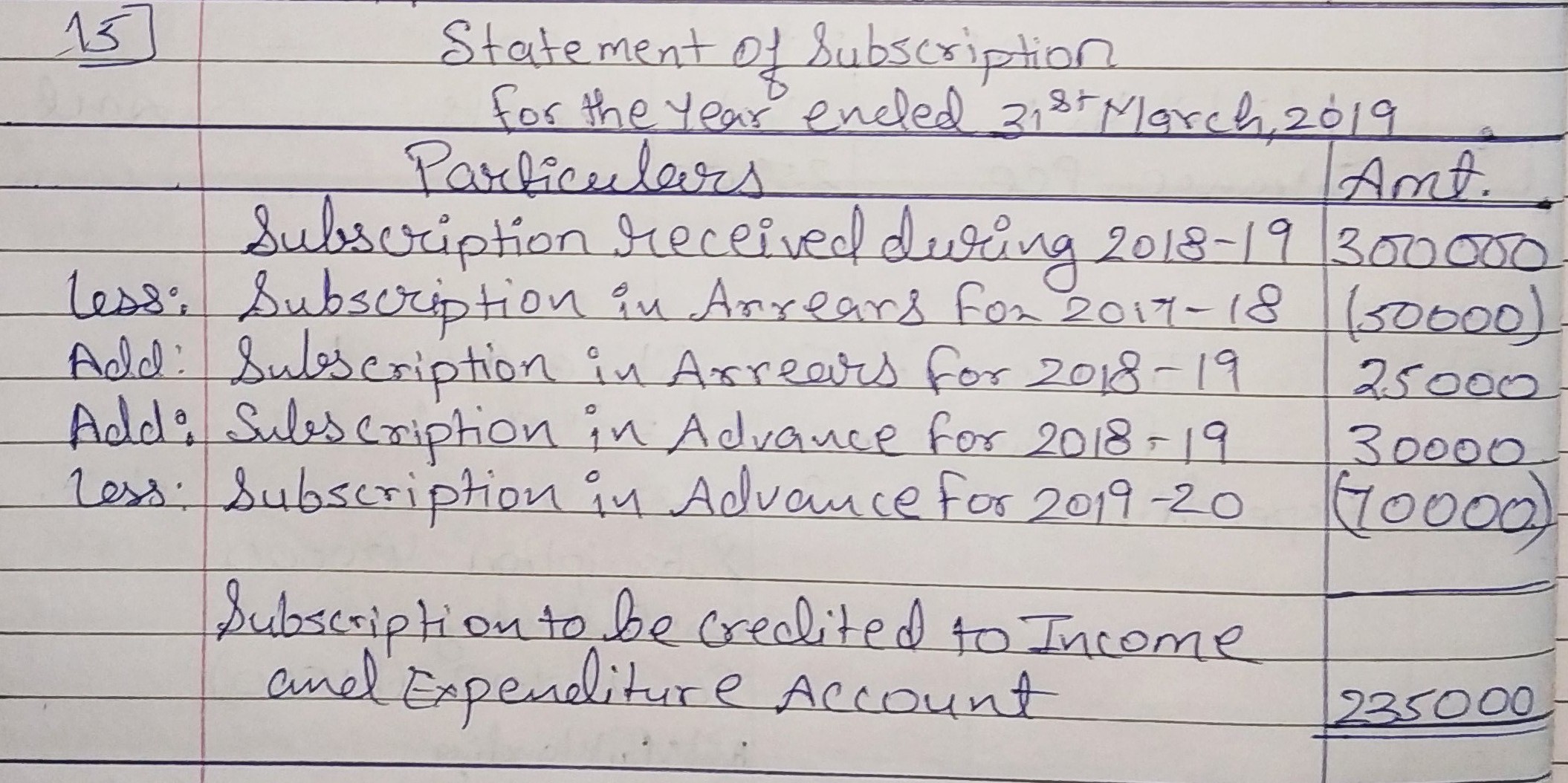

Question 15:

From the following information, calculate amount of subscriptions to be credited to the Income and Expenditure Account for the year ended 31st March, 2019:

| ₹ | ||

| 1st April, 2018 | Subscriptions in Arrears | 50,000 |

| Subscriptions Received in Advance | 30,000 | |

| 31st March, 2019 | Subscriptions in Arrears | 25,000 |

| Subscriptions Received in Advance | 70,000 |

Subscriptions received during the year ended 31st March, 2019 – ₹ 3,00,000

Subscription still in arrears for the year 2017 – 18 – ₹ 10,000.

ANSWER:

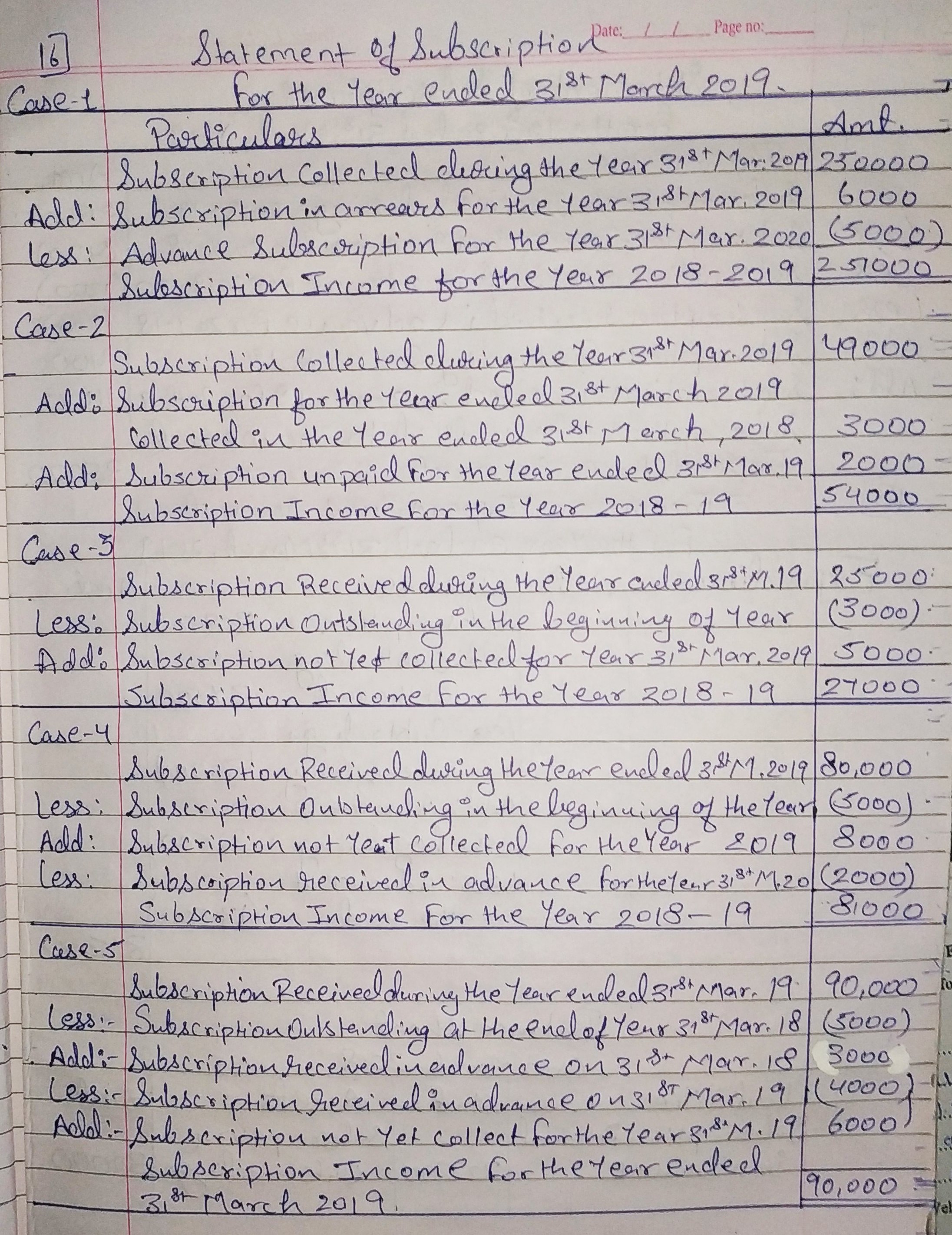

Question 16:

Calculate amount of subscriptions which will be treated as income for the year ended 31st March, 2019 for each of the following cases:

| Particulars | ₹ | |

| Case I. | (i) Subscriptions collected during the year ended 31st March, 2019 (ii) Subscriptions in arrears for the year ended 31st March, 2019 (iii) Subscriptions received in advance for the year ended 31st March, 2020 | 2,50,000 6,000 5,000 |

| Case II. | (i) Subscriptions collected during the year ended 31st March, 2019 (ii) Subscriptions for the year ended 31st March, 2019 collected in the year ended 31st March, 2018 (iii) Subscriptions unpaid for the year ended 31st March, 2019 | 49,000 3,000 2,000 |

| Case III. | (i) Subscriptions received during the year ended 31st March, 2019 (ii) Subscriptions outstanding in the beginning of the year ended 31st March, 2019 (iii) Subscriptions not yet collected for the year ended 31st March, 2019 | 25,000 3,000 5,000 |

| Case IV. | (i) Subscriptions received during the year ended 31st March, 2019 (ii) Subscriptions outstanding in the beginning of the year ended 31st March, 2019 (iii) Subscriptions not yet collected for the year ended 31st March, 2019 (iv) Subscriptions received in advance for the year ended 31st March, 2020 | 80,000 5,000 8,000 2,000 |

| Case V. | (i) Subscriptions received during the year ended 31st March, 2019 (ii) Subscriptions outstanding at the end of the year ended 31st March, 2018 (iii) Subscriptions received in advance on 31st March, 2018 (iv) Subscriptions received in advance on 31st March, 2019 (v) Subscriptions not yet collected for the year ended 31st March, 2019 | 90,000 5,000 3,000 4,000 6,000 |

ANSWER:

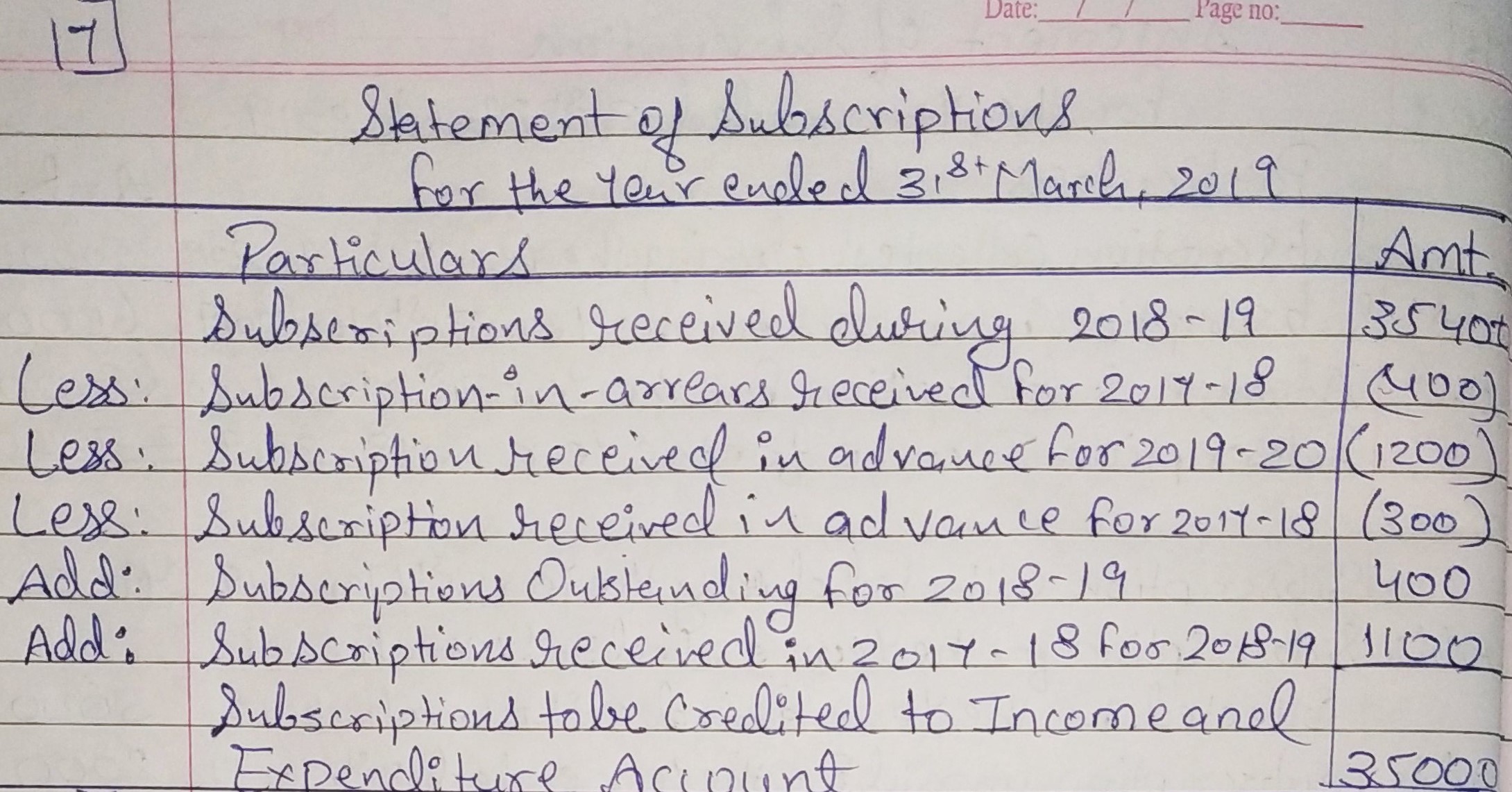

Question 17:

From the following particulars, calculate amount of subscriptions to be credited to the Income and Expenditure Account for the year ended 31st March, 2019:

| ₹ | ||

| (a) | Subscriptions in arrears on 31st March, 2018 | 500 |

| (b) | Subscriptions received in advance on 31st March, 2018 for the year ended on 31st March, 2019 | 1,100 |

| (c) | Total Subscriptions received during the year ended 31st March, 2019 (including ₹ 400 for the year ended 31st March, 2018, ₹ 1,200 for the year ended 31st March, 2020 and ₹ 300 for the year ended 31st March, 2021) | 35,400 |

| (d) | Subscriptions outstanding for year ended 31st March, 2019 | 400 |

ANSWER:

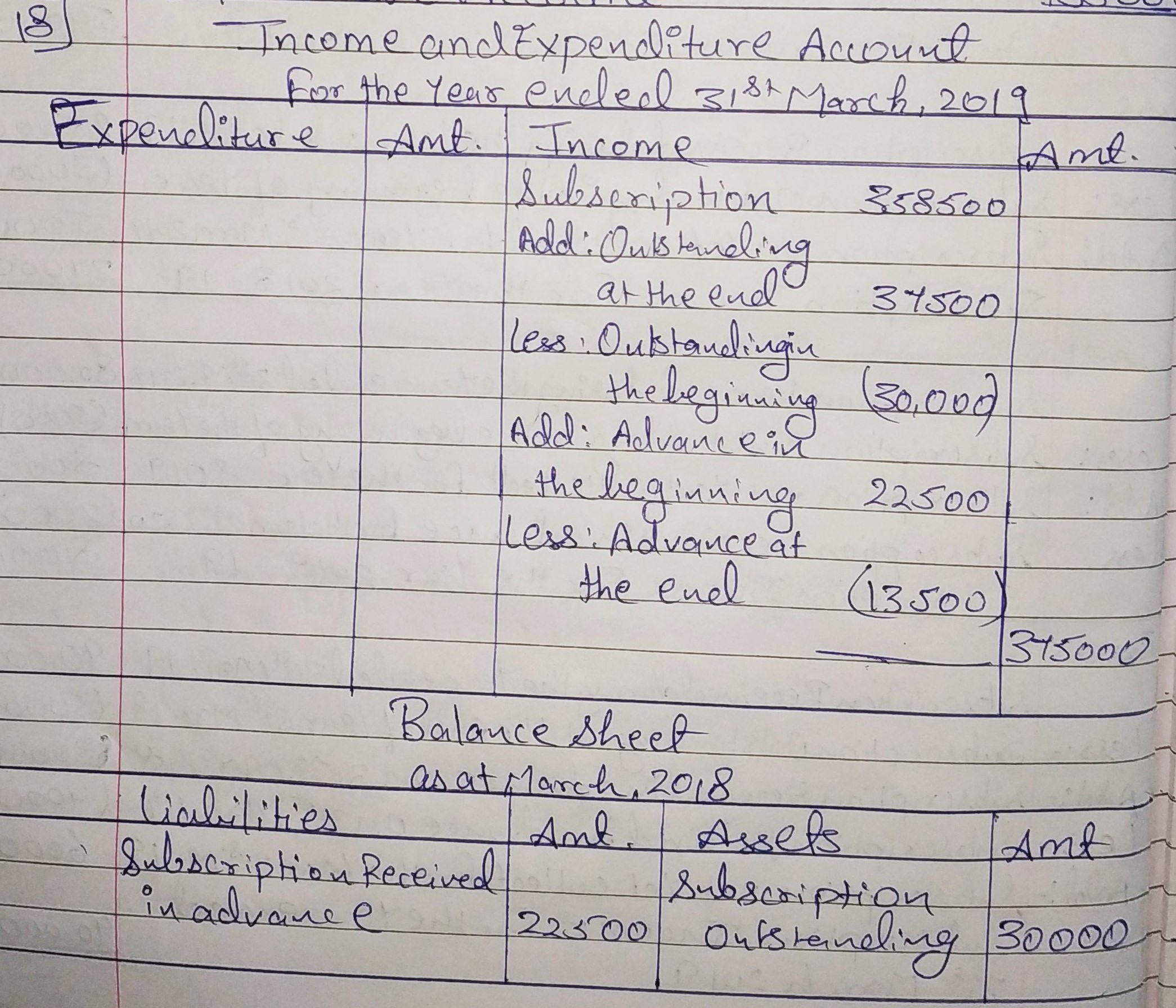

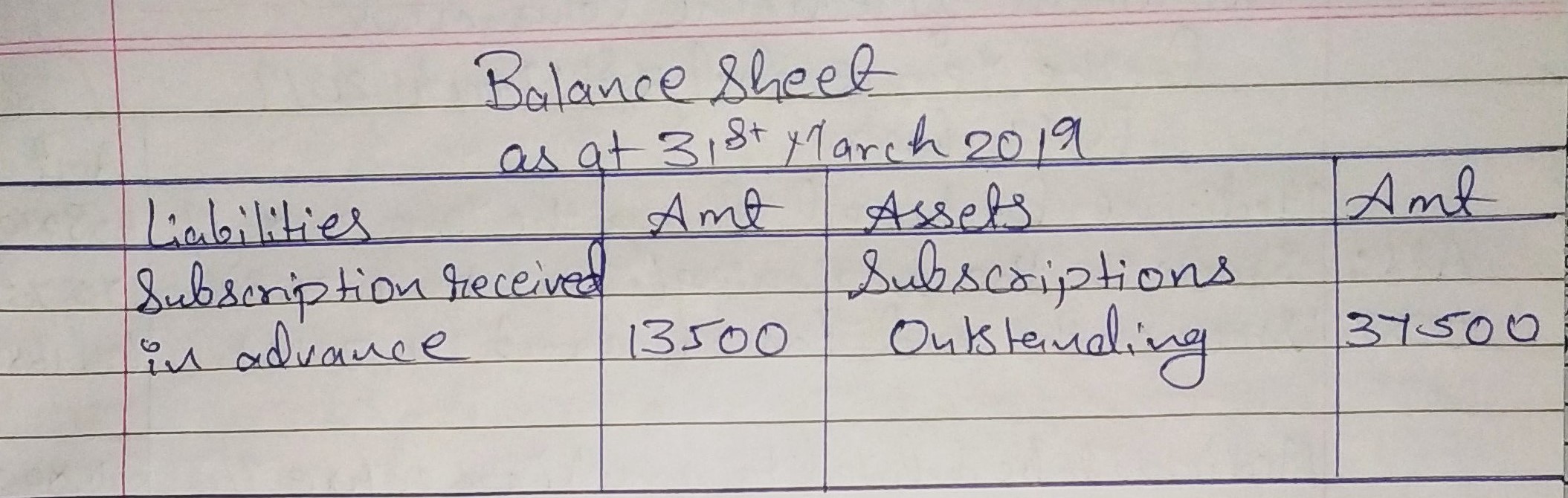

Question 18:

How are the following items of subscriptions shown in the Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheets as at 31st March, 2018 and 2019?

| ₹ | |

| Subscriptions received during the year ended 31st March, 2019 | 3,58,500 |

| Subscriptions outstanding on 31st March, 2018 | 30,000 |

| Subscriptions received in Advance on 31st March,2018 | 22,500 |

| Subscriptions received in Advance on 31st March, 2019 | 13,500 |

| Subscriptions outstanding on 31st March, 2019 | 37,500 |

(including ₹ 12,500 for the year ended 31st March, 2018)

ANSWER:

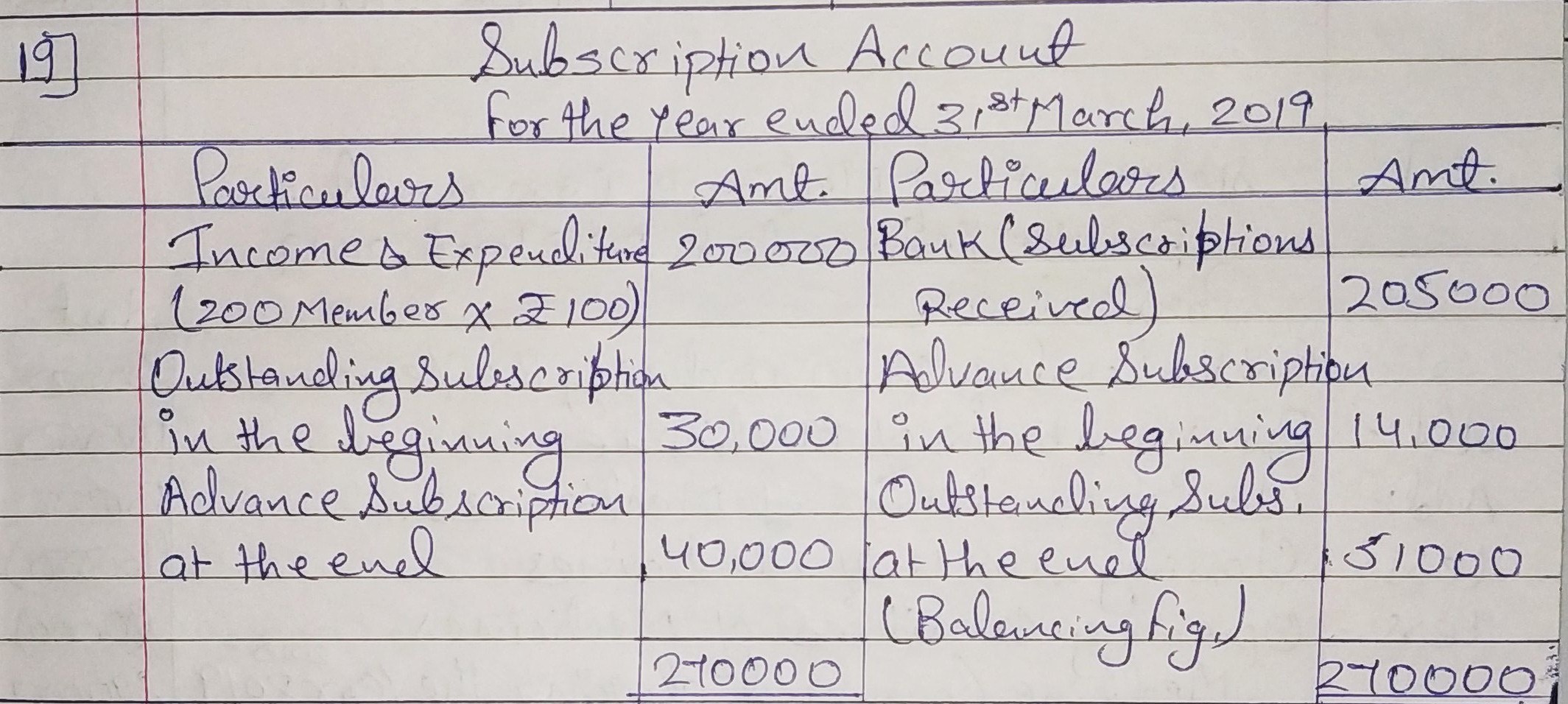

Question 19:

From the following information, calculate amount of subscriptions outstanding for the year ended 31st March, 2019:

A club has 200 members each paying an annual subscription of ₹ 1,000. The Receipts and Payments Account for the year showed a sum of ₹ 2,05,000 received as subscriptions. The following additional information is provided :

| ₹ | |

| Subscriptions Outstanding on 31st March, 2018 | 30,000 |

| Subscriptions Received in Advance on 31st March, 2019 | 40,000 |

| Subscriptions Received in Advance on 31st March, 2018 | 14,000 |

ANSWER:

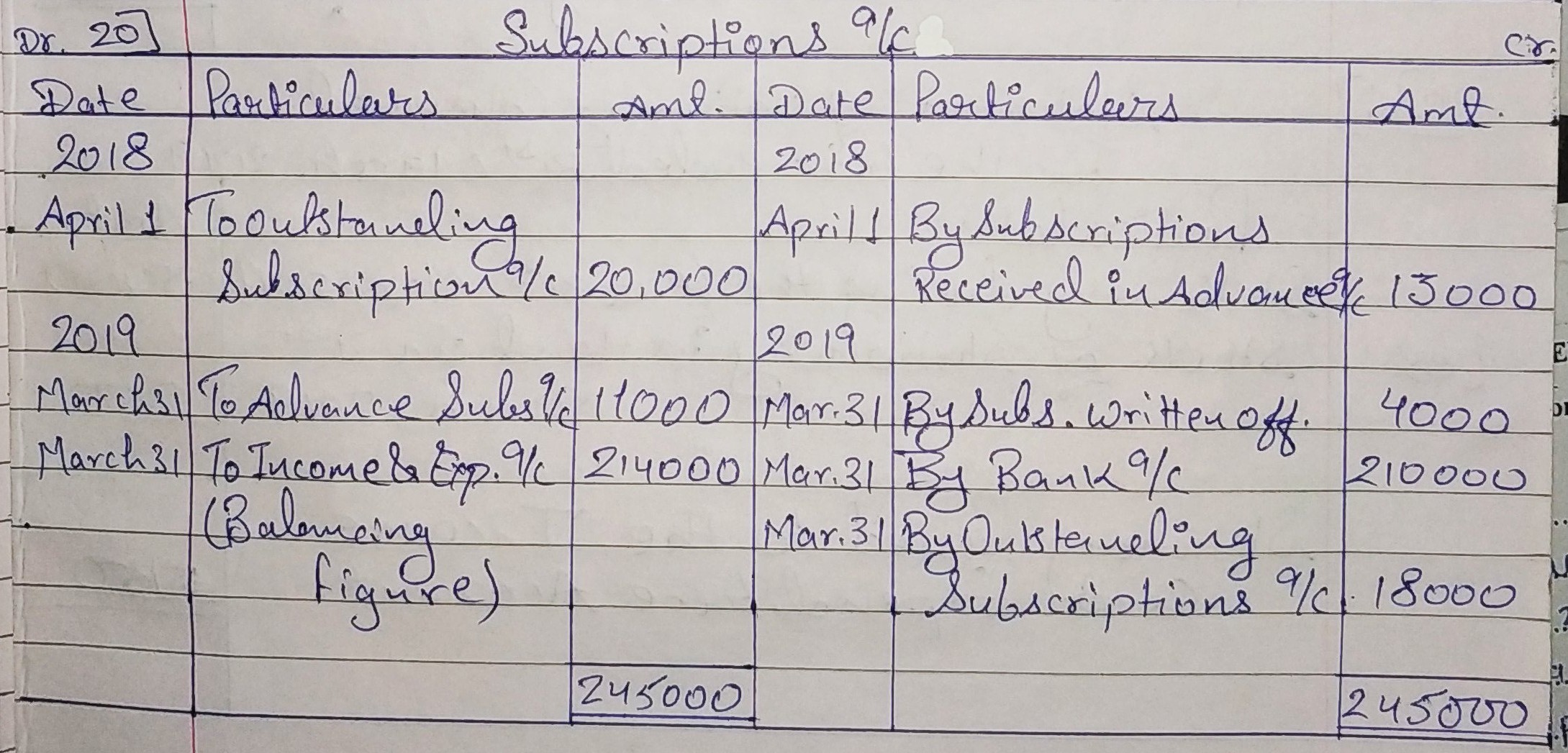

Question 20:

From the following information, prepare Subscription Account for the year ending 31st March, 2019:

| Particulars | 31st March, 2018 (₹) | 31st March, 2019 (₹) |

| Subscription in Arrears | 20,000 | 18,000 |

| Subscription in Advance | 13,000 | 11,000 |

In the year ending 31st March, 2019, subscription received were ₹ 2,10,000 (including ₹ 6,000 of arrears from previous year) and subscription arrears of previous year were written off ₹ 4,000.

ANSWER:

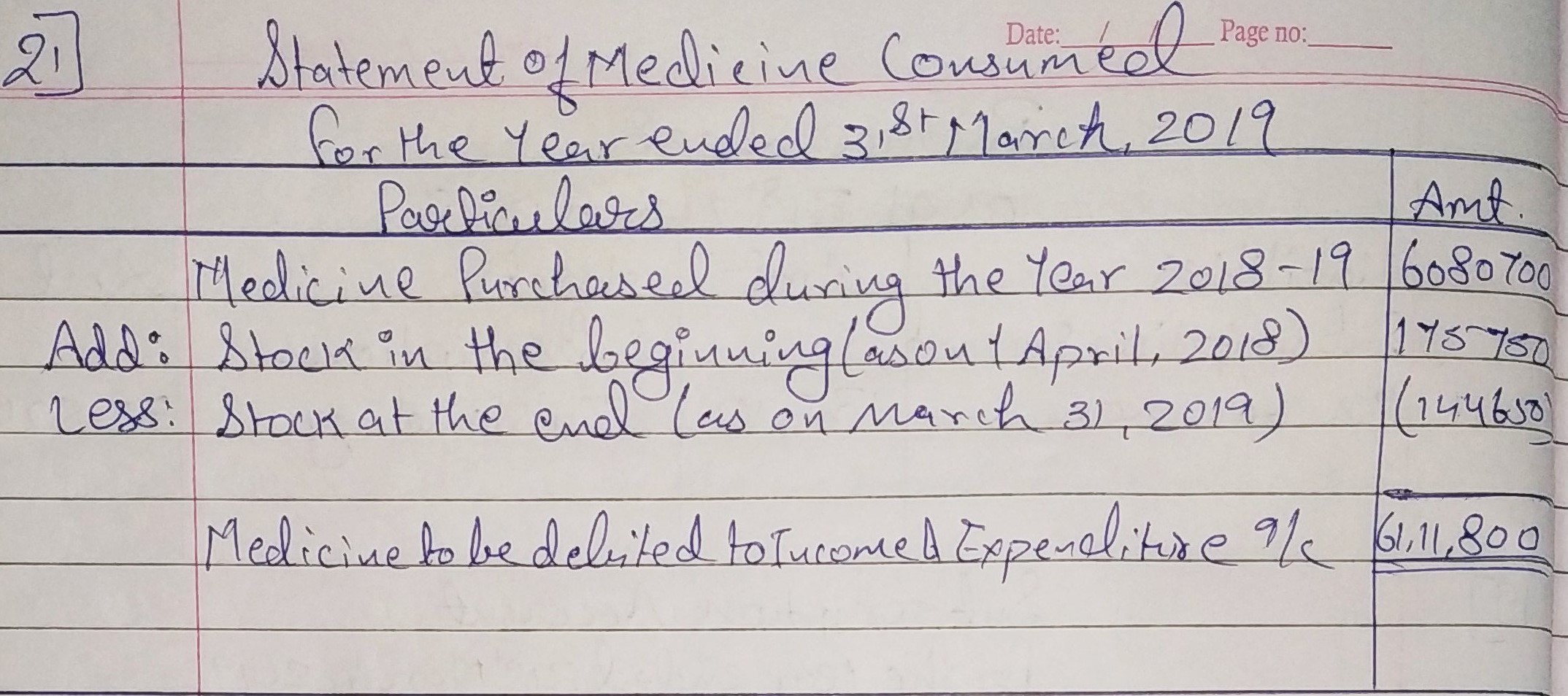

Question 21:

On the basis of information given below, calculate the amount of medicines to be debited to the Income and Expenditure Account of Good Health Hospital for the year ended 31st March, 2019:

| Particulars | 1st April, 2018 (₹) | 31st March, 2019 (₹) |

| Stock of Medicines | 1,75,750 | 1,44,650 |

| Creditors for Medicines | 15,06,900 | 18,20,700 |

Medicines purchased during the year ended 31st March, 2019 were ₹ 60,80,700.

ANSWER:

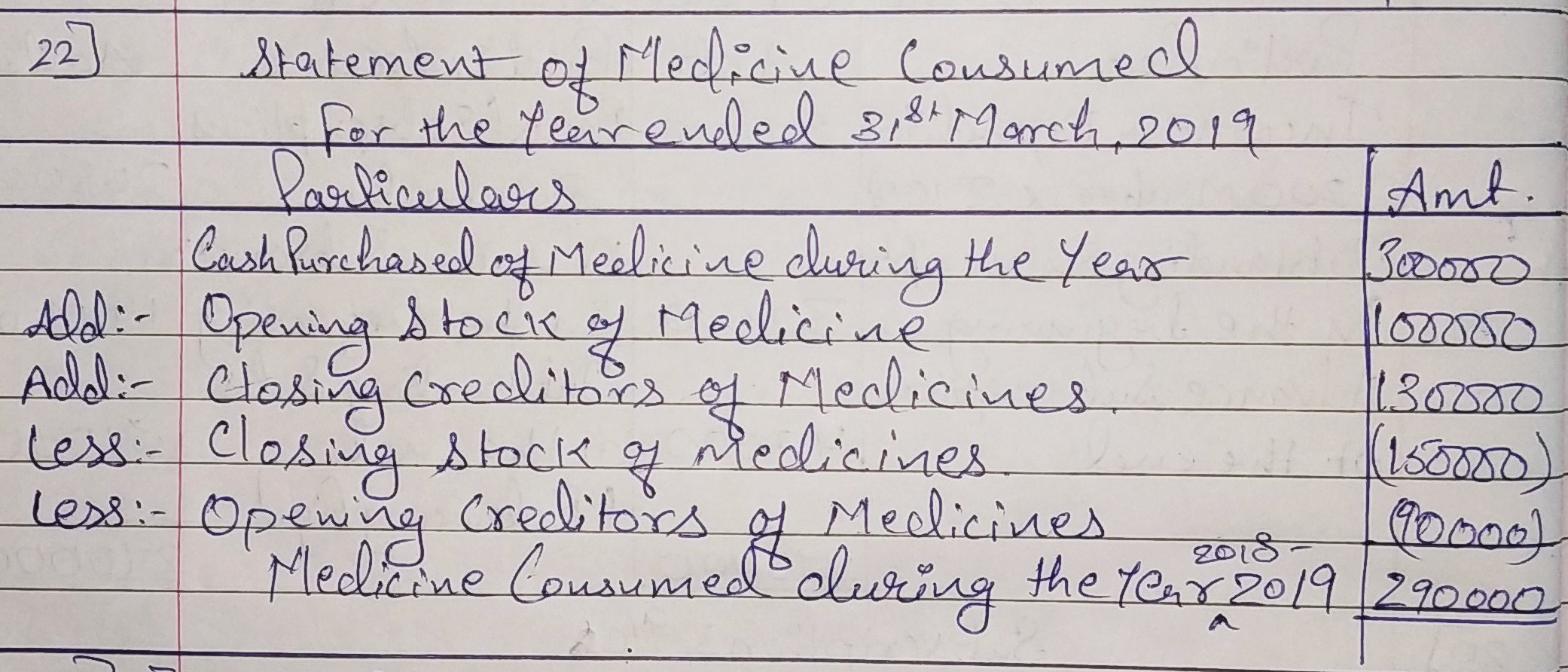

Question 22:

| Calculate amount of medicines consumed during the year ended 31st March, 2019: | ₹ |

| Opening Stock of Medicines | 1,00,000 |

| Opening Creditors for Medicines | 90,000 |

| Cash purchases of Medicines during the year | 3,00,000 |

| Closing Stock of Medicines | 1,50,000 |

| Closing Creditors for Medicines | 1,30,000 |

ANSWER:

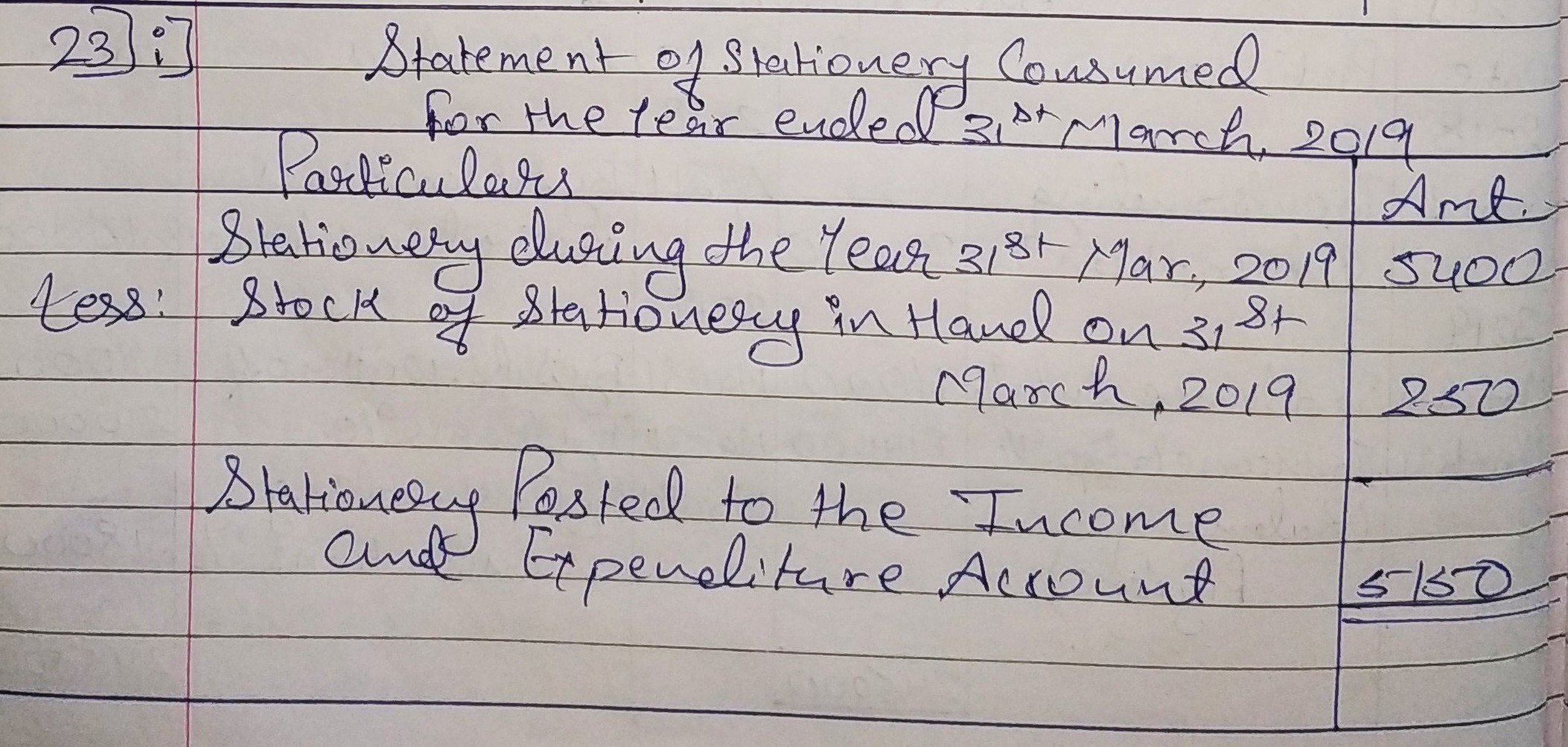

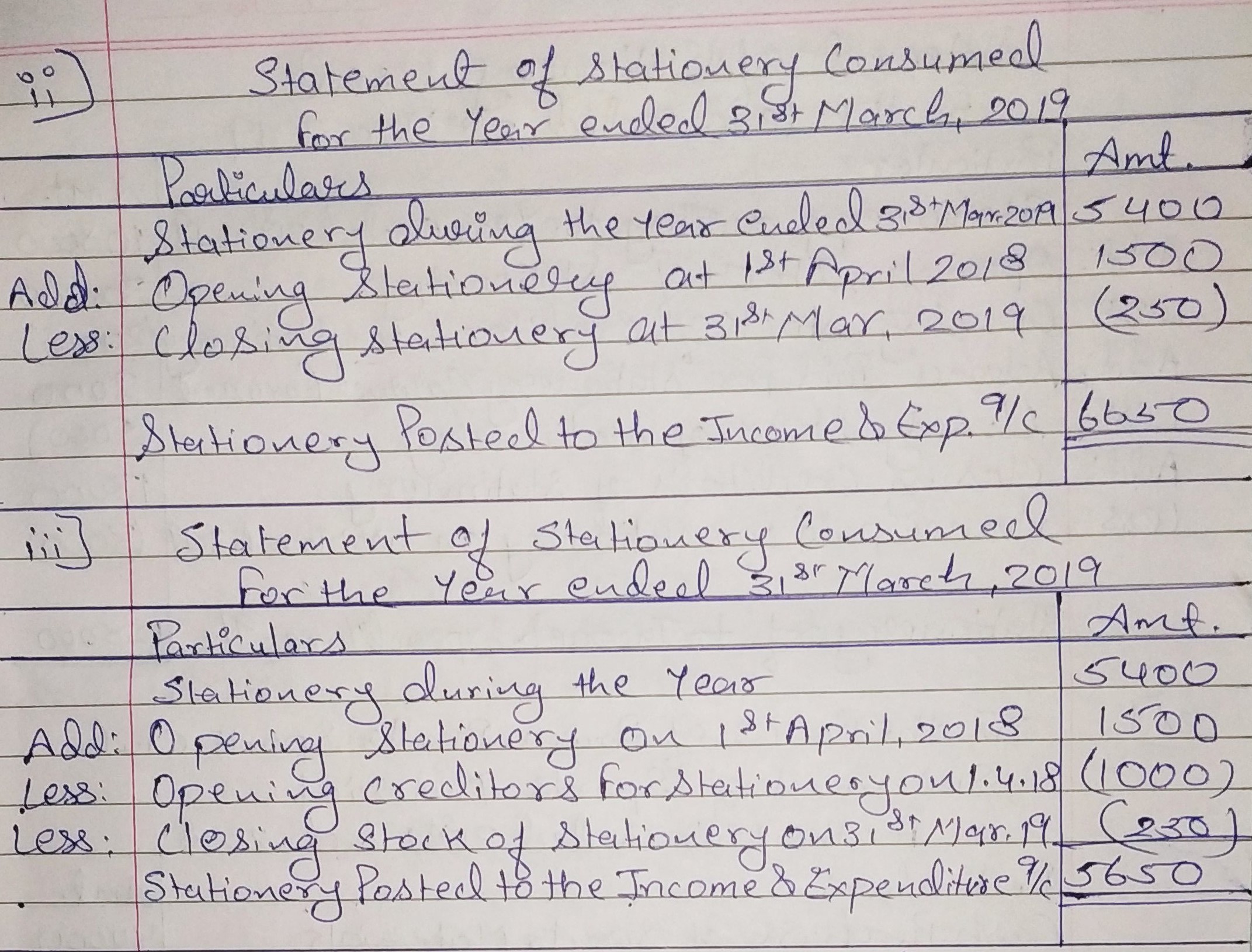

Question 23:

Calculate amount to be posted to the Income and Expenditure Account for the year ended 31st March, 2019:

| (i) | Amount paid for stationery during the year ended 31st March, 2019 – ₹5,400; Stock of Stationery in Hand on 31st March, 2019 – ₹ 250. | |

| (ii) | Stock of Stationery in Hand on 1st April, 2018 – ₹ 1,500; Payment made for Stationery during the year ended 31st March, 2019 – ₹ 5,400; Stock of Stationery in Hand on 31st March, 2019 – ₹ 250. | |

| ₹ | ||

| (iii) | Stock of Stationery on 1st April, 2018 | 1,500 |

| Creditors for Stationery on 1st April, 2018 | 1,000 | |

| Amount paid for Stationery during the year | 5,400 | |

| Stock of Stationery on 31st March, 2019 | 250 |

ANSWER:

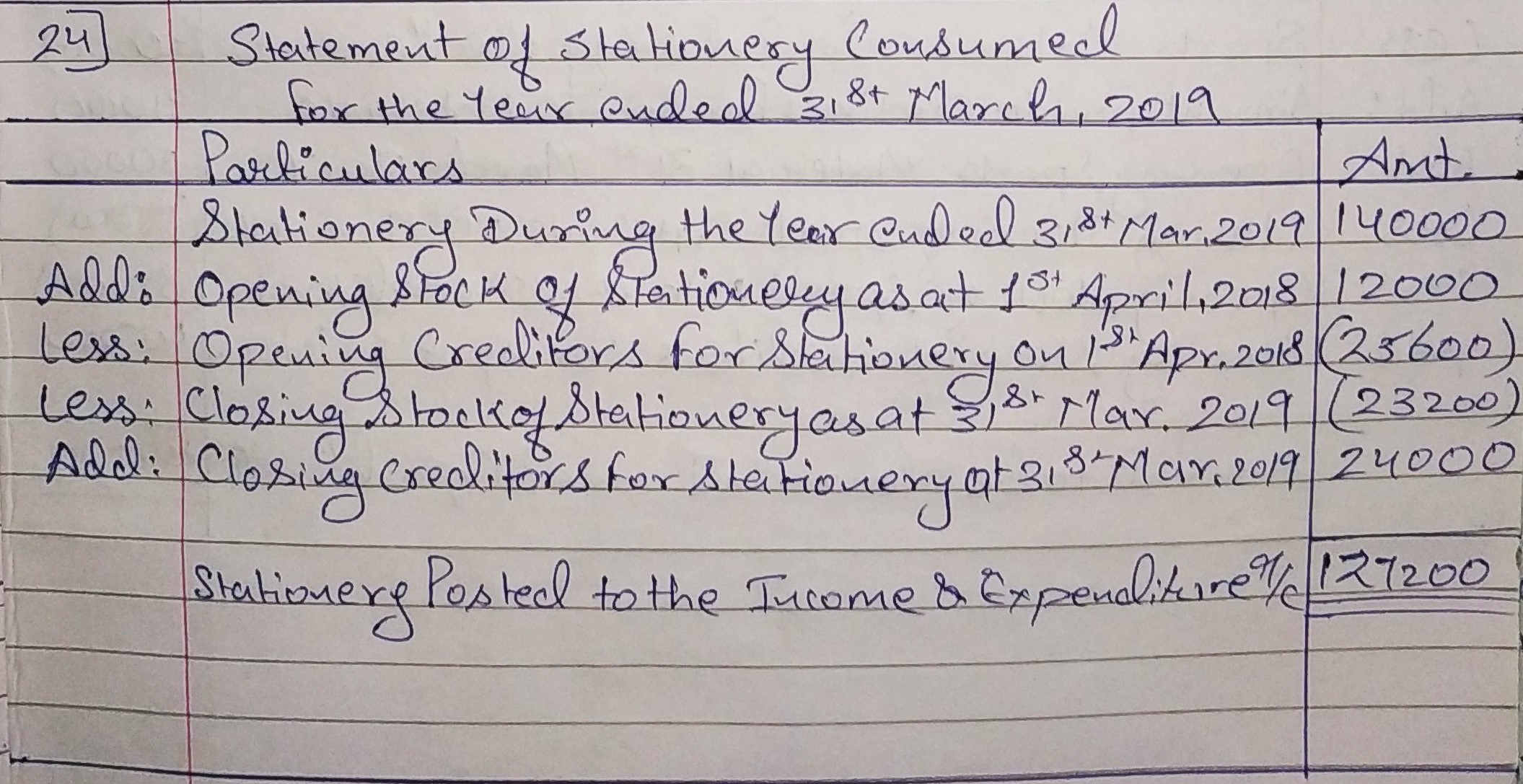

Question 24:

On the basis of the following information, calculate amount that will appear against the term ‘Stationery Used’ in the Income and Expenditure Account for the year ended 31st March, 2019:

| ₹ | |

| Stock of Stationery as at 1st April, 2018 | 12,000 |

| Creditors for Stationery as at 1st April, 2018 | 25,600 |

| Amount paid for Stationery during the year ended 31st March, 2019 | 1,40,000 |

| Stock of Stationery as at 31st March, 2019 | 23,200 |

| Creditors for Stationery as at 31st March,2019 | 24,000 |

ANSWER:

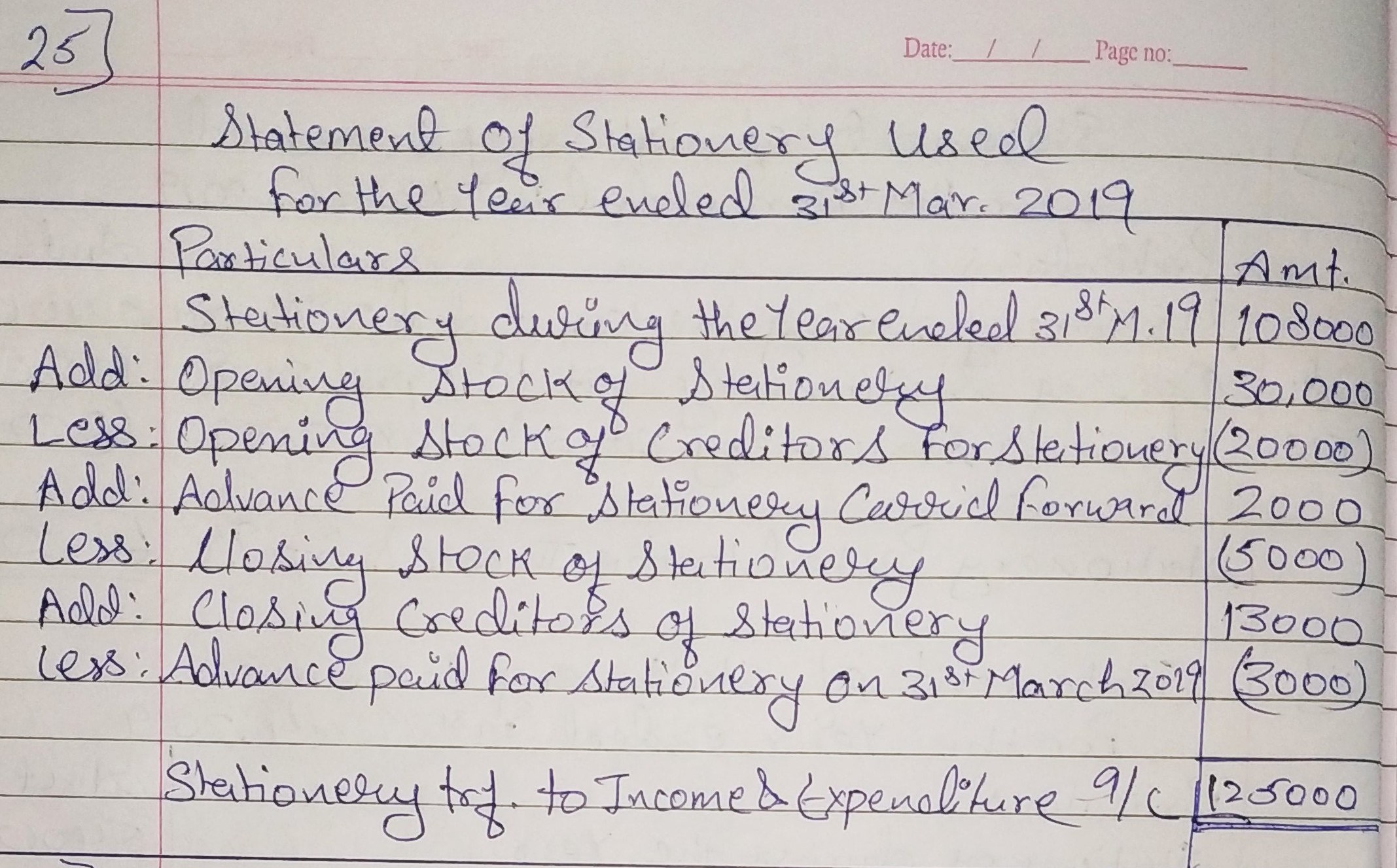

Question 25:

Calculate the amount that will be posted to the income and Expenditure Account for the year ended 31st March, 2019:

| ₹ | |

| Stock of Stationery on 1st April, 2018 | 30,000 |

| Creditors for Stationery on 1st April, 2018 | 20,000 |

| Advances paid for Stationery carried forward from the year ended 31st March, 2018 | 2,000 |

| Amount paid for Stationery during the year ended 31st March, 2019 | 1,08,000 |

| Stock of Stationery on 31st March, 2019 | 5,000 |

| Creditors for Stationery on 31st March, 2019 | 13,000 |

| Advance paid for Stationery on 31st March, 2018 | 3,000 |

ANSWER:

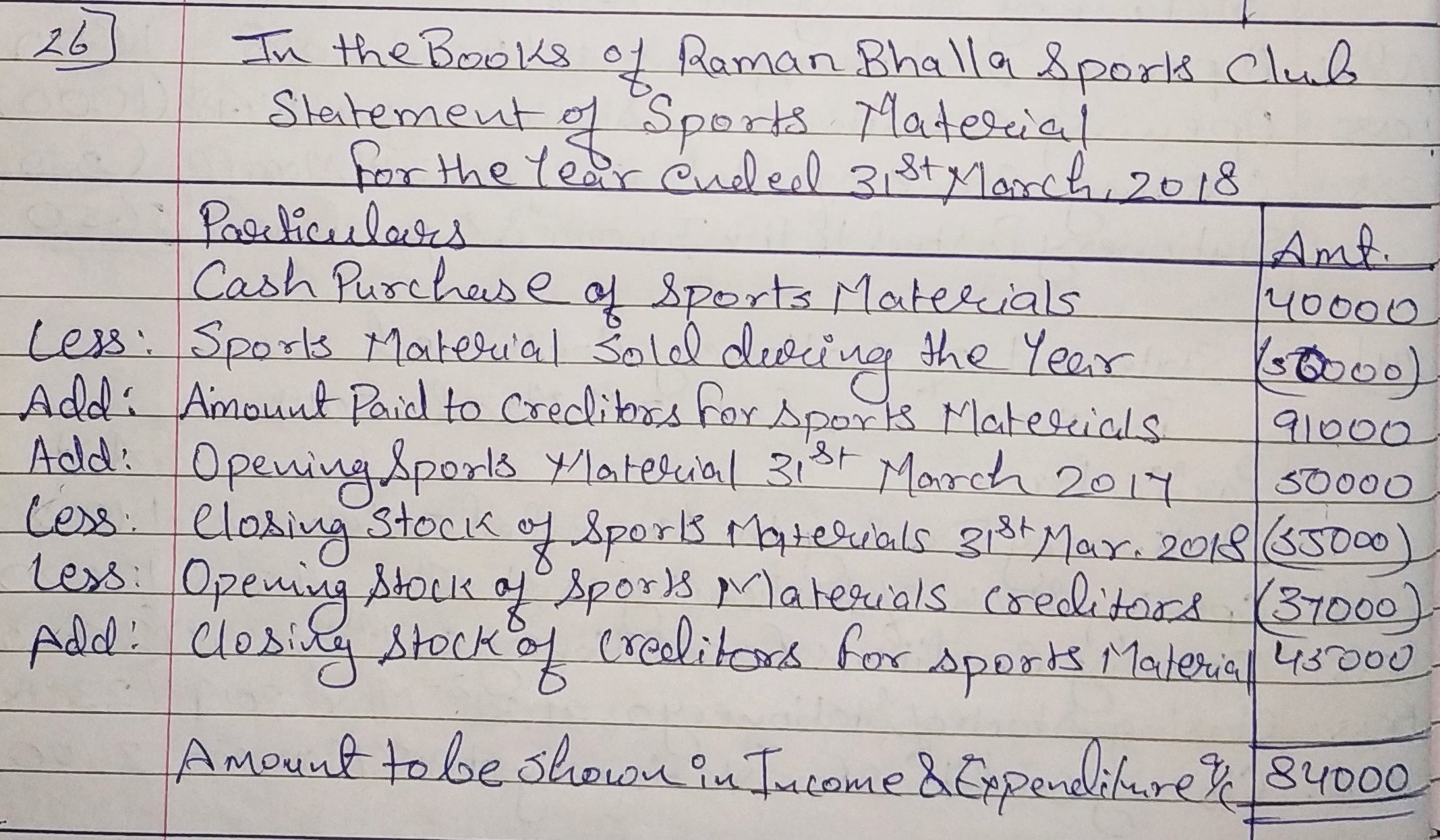

Question 26:

Calculate the amount of sports material to be transferred to income and Expenditure Account of Raman Bhalla Sports Club, Ludhiana, for the year ended 31st March, 2018:

| Particulars | (₹) | |

| (i) | Sports material sold during the year (Book Value ₹ 50,000) | 56,000 |

| (ii) | Amount paid to creditors for sports materials | 91,000 |

| (iii) | Cash purchase of sports material | 40,000 |

| (iv) | Sports material as on 31st March, 2017 | 50,000 |

| (v) | Sports material as on 31st March, 2018 | 55,000 |

| (vi) | Creditors for sports material as on 31st March, 2017 | 37,000 |

| (vii) | Creditors for sports material as on 31st March, 2018 | 45,000 |

ANSWER:

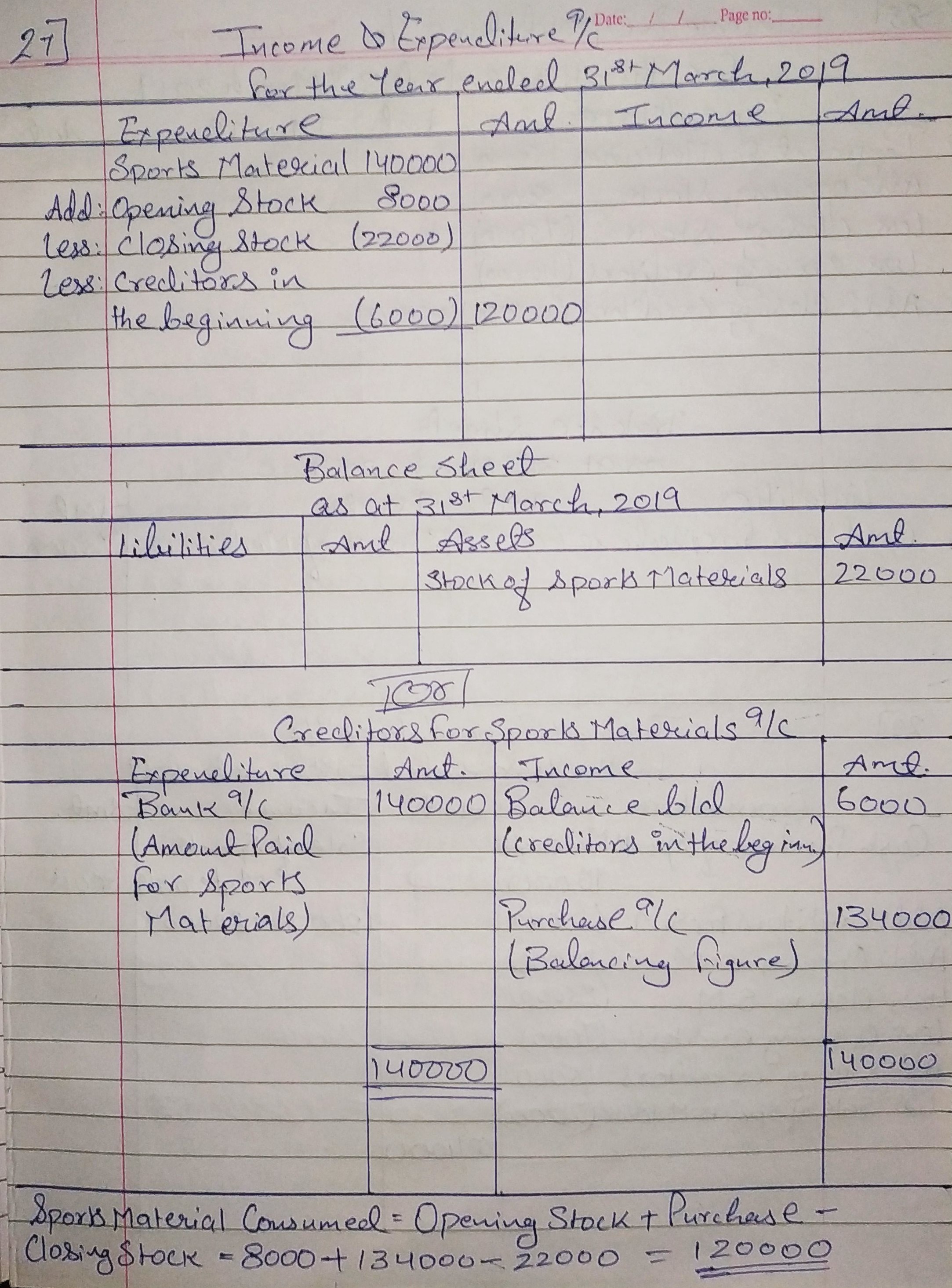

Question 27:

How are the following dealt with while preparing the final accounts for the year ended 31st , 2019?

| RECEIPTS AND PAYMENTS ACCOUNT (AN EXTRACT) for the year ended 31st March, 2019 | ||||

| Dr. | Cr. | |||

| Receipts | ₹ | Payments | ₹ | |

| By Payments for Sports Material | 1,40,000 | |||

| BALANCE SHEET (AN EXTRACT) as at 1st April, 2018 | ||||

Liabilities | ₹ | Assets | ₹ | |

| Creditors for Sports Materials | 6,000 | Sports Materials | 8,000 | |

Additional information :

Sports Materials in Hand on 31st March, 2019 – ₹ 22,000.

ANSWER:

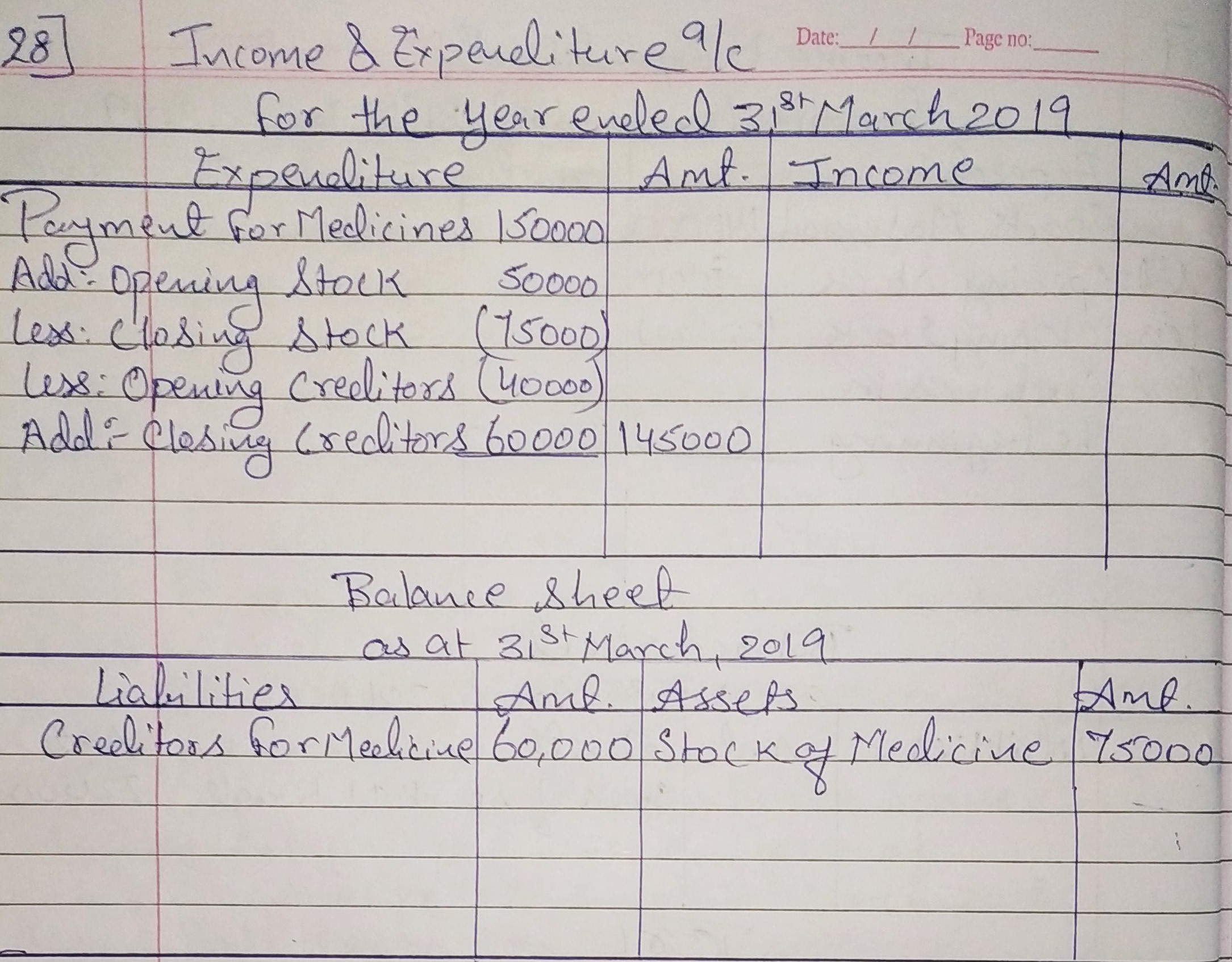

Question 28:

How are the following dealt with while preparing the final accounts for the year ended 31st March, 2019?

RECEIPTS AND PAYMENTS ACCOUNT (AN EXTRACT) | ||||

Dr. |

| Cr. | ||

| Receipts | ₹ | Payments | ₹ | |

| By Payments for Medicines | 1,50,000 | ||

|

| |||

Additional information :

| As at 1st April, 2018 (₹) | As at 31st March, 2019 (₹) | |

| Stock of Medicines | 50,000 | 75,000 |

| Creditors for Medicines | 40,000 | 60,000 |

ANSWER:

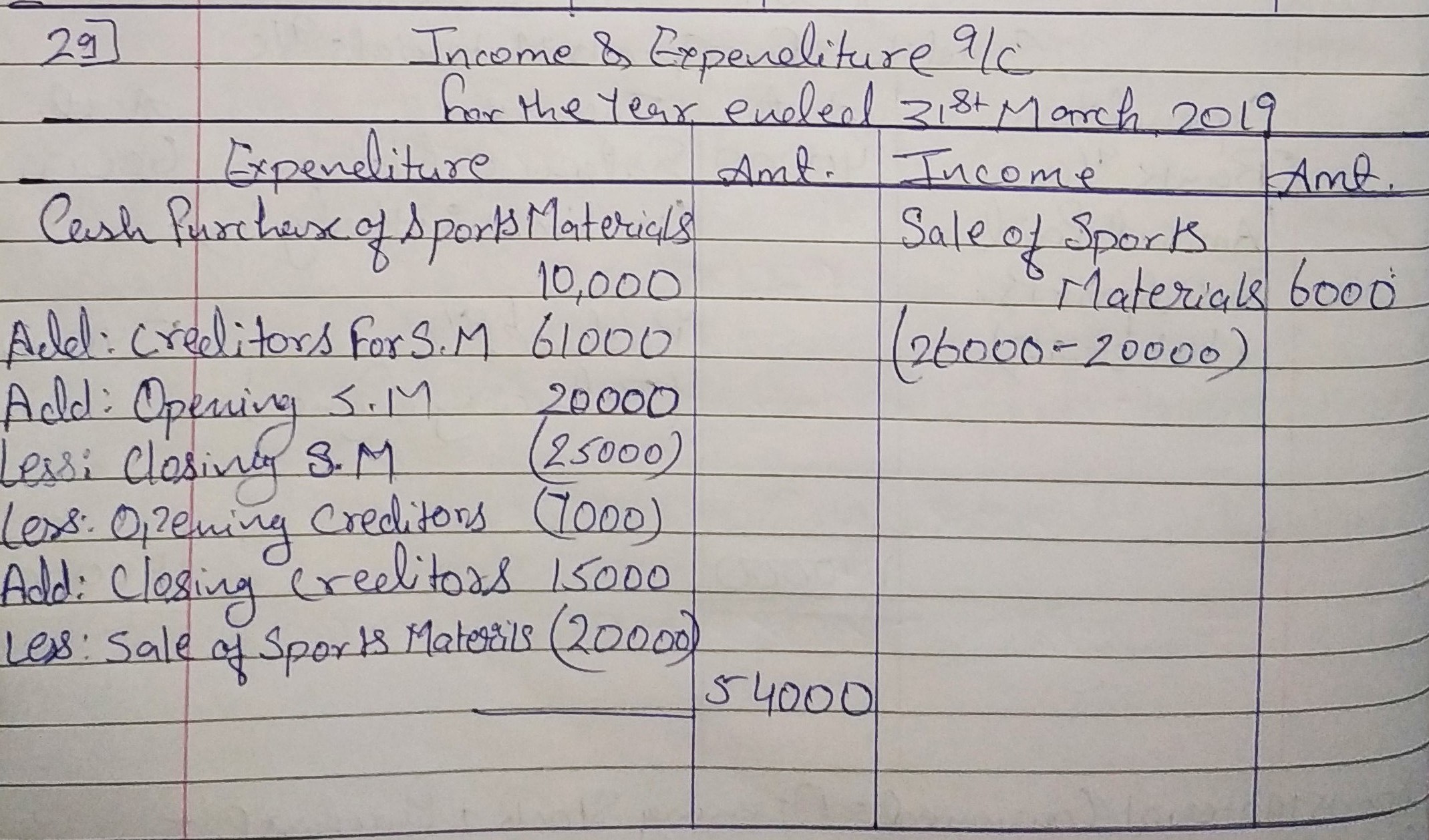

Question 29:

How are the following dealt with while preparing the final accounts of a sports club for the year ended 31st March, 2019?

| Dr. | Cr. | |||

Receipts | ₹ | Payments | ₹ | |

| To Sale of Sports Materials | 26,000 | By Creditors for Sports Materials | 61,000 | |

| (Book value ₹ 20,000) | By Cash purchase of Sports Materials | 10,000 | ||

Additional information :

| As at 31st March, 2018 (₹) | As at 31st March, 2019 (₹) | |

| Sports Materials | 20,000 | 25,000 |

| Creditors for Sports Materials | 7,000 | 15,000 |

ANSWER:

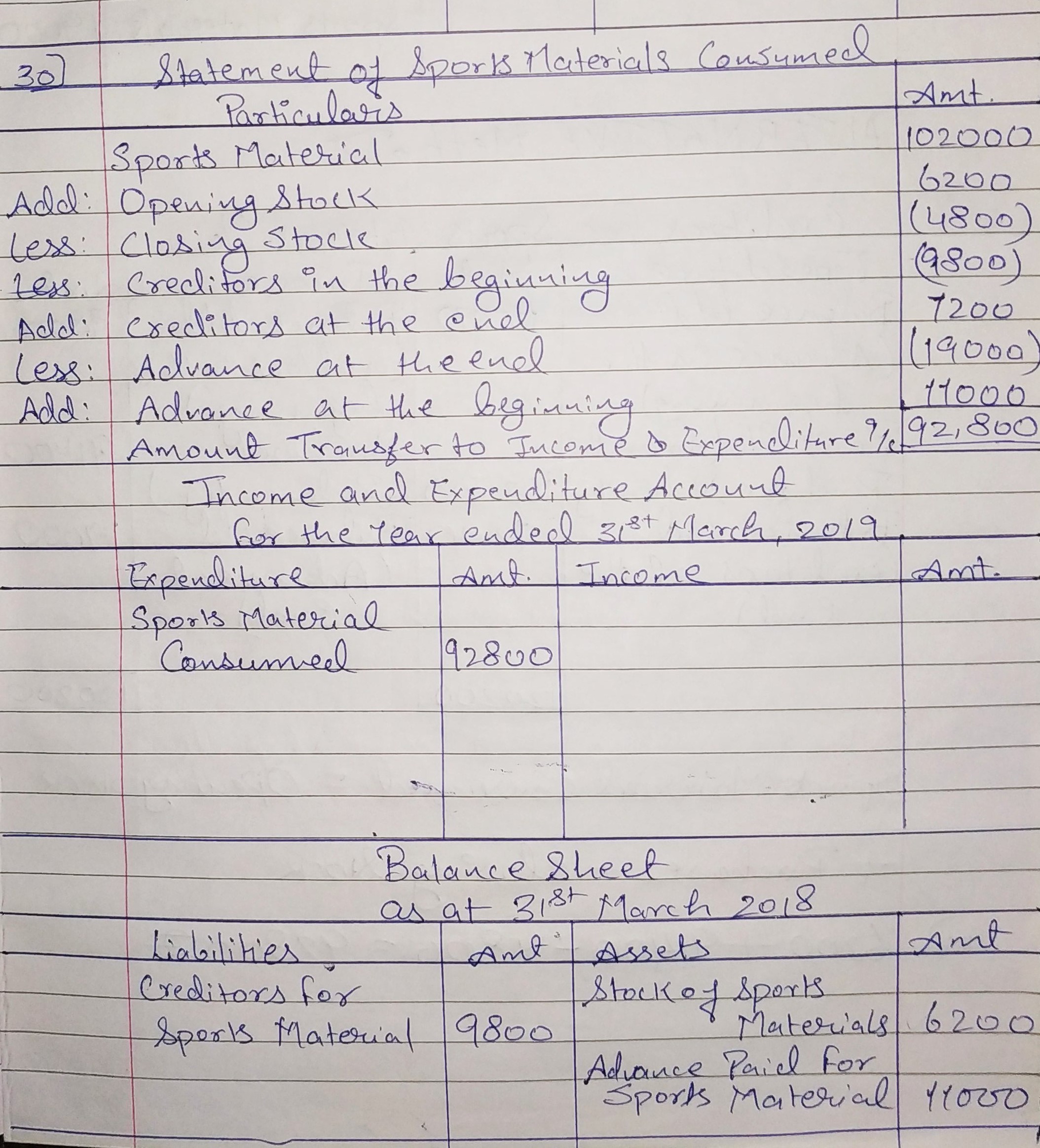

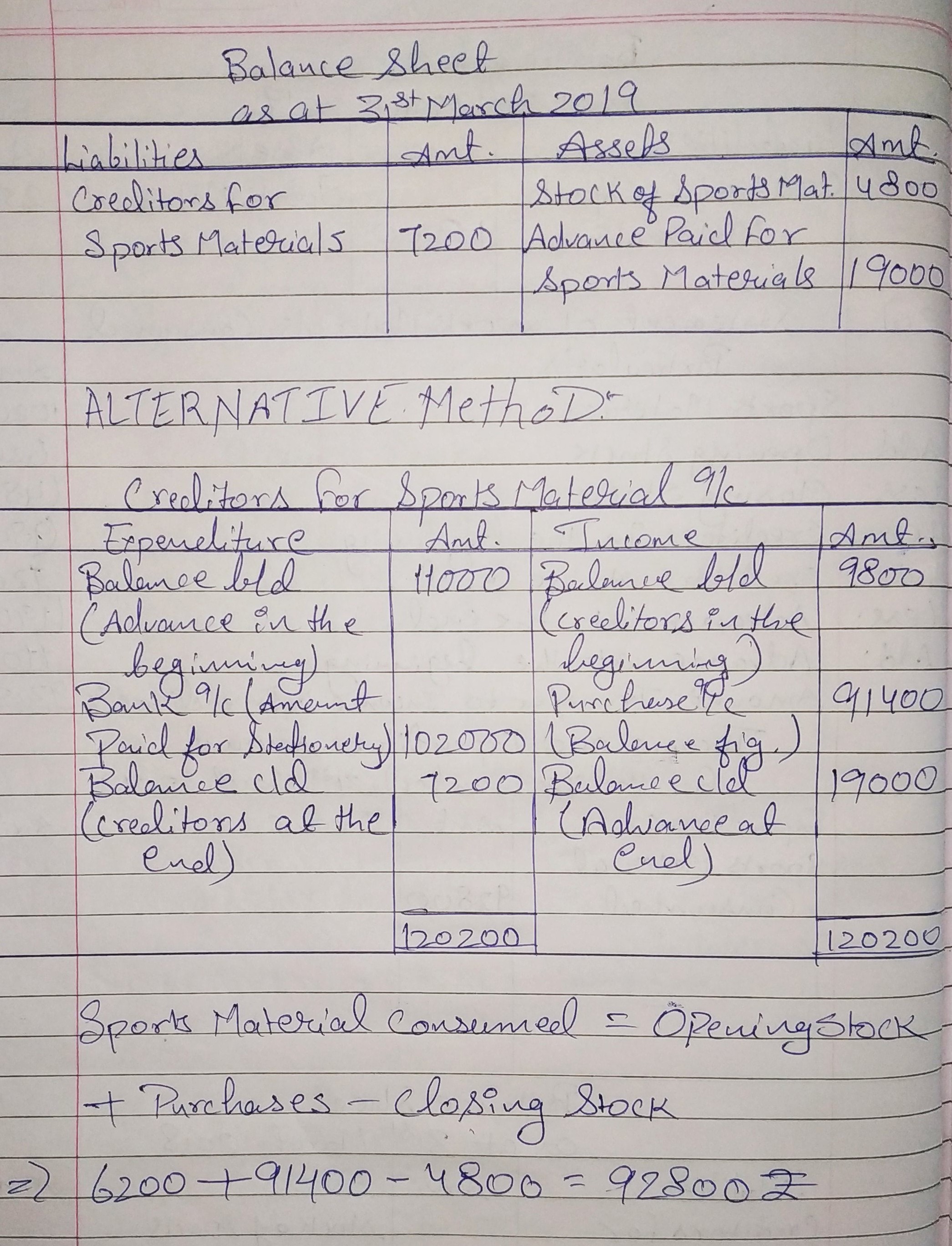

Question 30:

From the following information of a Not-for-Profit Organisation, show the ‘Sports Materials’ item in the Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheets as at 31st March, 2018 and 31st March, 2019:

| Particulars | 31st March, 2018 | 31st March, 2019 ₹ | |

| Stocks of Sports Materials | 6,200 | 4,800 | |

| Creditors for Sports Materials | 9,800 | 7,200 | |

| Advance to Suppliers for Sports Materials | 11,000 | 19,000 | |

Payment to suppliers for Sports Materials during the year was ₹ 1,02,000. There were no cash purchases made.

ANSWER:

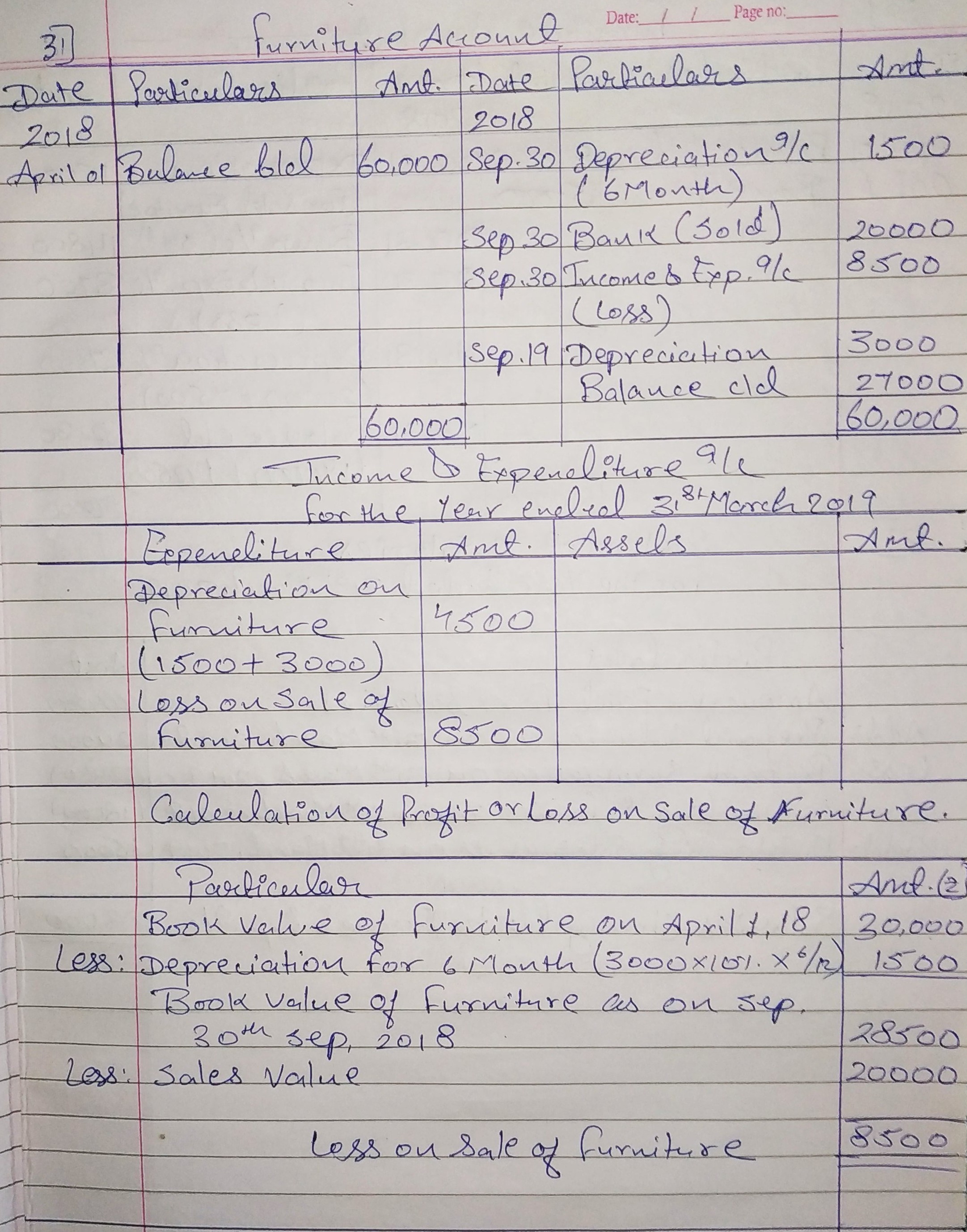

Question 31:

The book value of furniture on 1st April, 2018 is ₹ 60,000. Half of this furniture is sold for ₹ 20,000 on 30th September, 2018. Depreciation is to be charged on furniture @ 10% p.a.

Calculate loss on sale of furniture. Show how the loss on sale and depreciation on furniture will be shown in the Income and Expenditure Account for the year ended 31st March, 2019.

ANSWER:

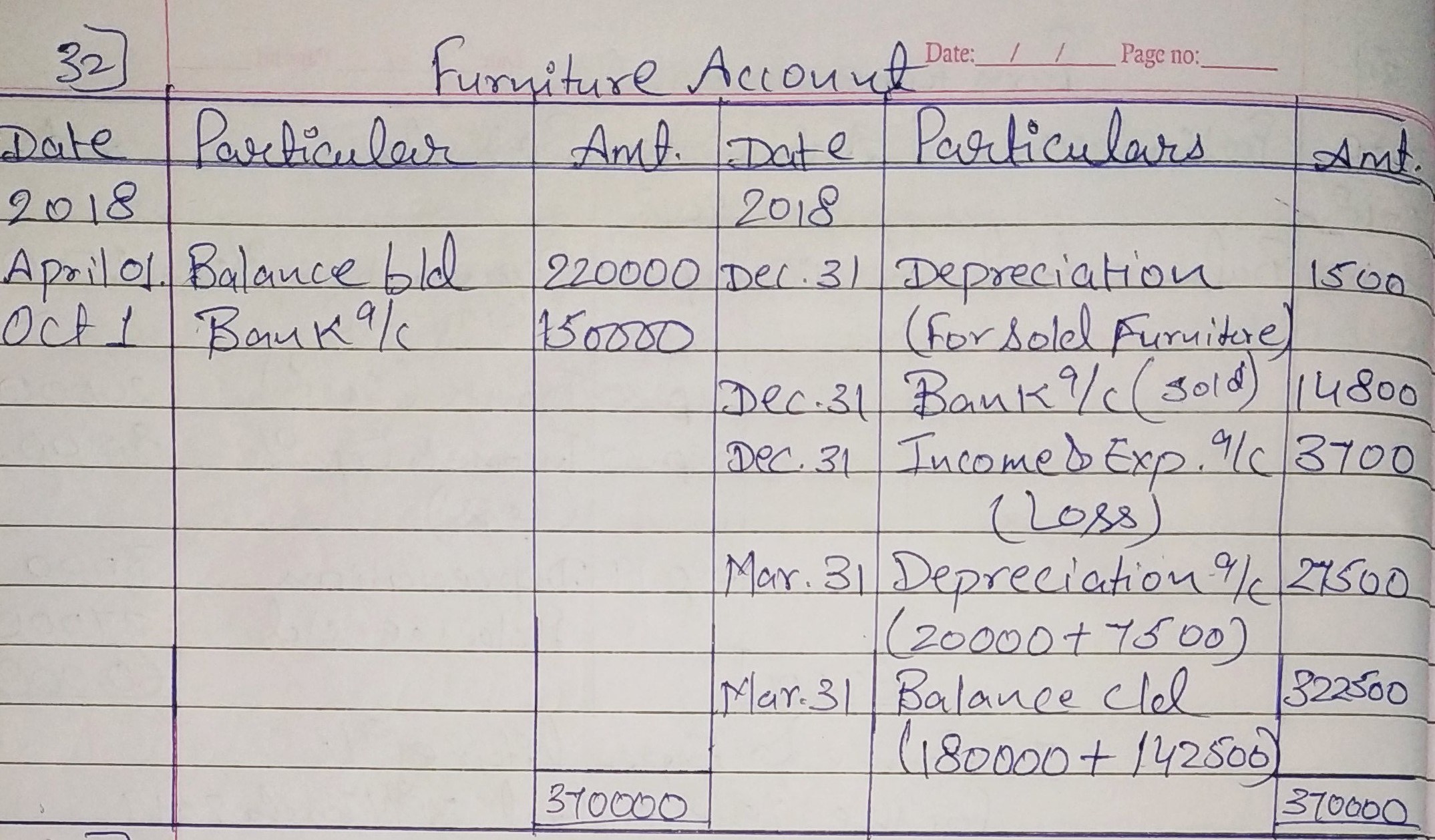

Question 32:

Delhi Youth Club has furniture at a value of ₹ 2,20,000 in its book on 31st March, 2018. It sold old furniture, having book value of ₹ 20,000 as at 1st April , 2018 at a loss of 20% on 31st December, 2018. Furniture is to be depreciated @ 10% p.a. Furniture costing ₹ 1,50,000 was also purchased on 1st October, 2018.

Prepare Furniture Account for the year ended 31st March, 2019.

ANSWER:

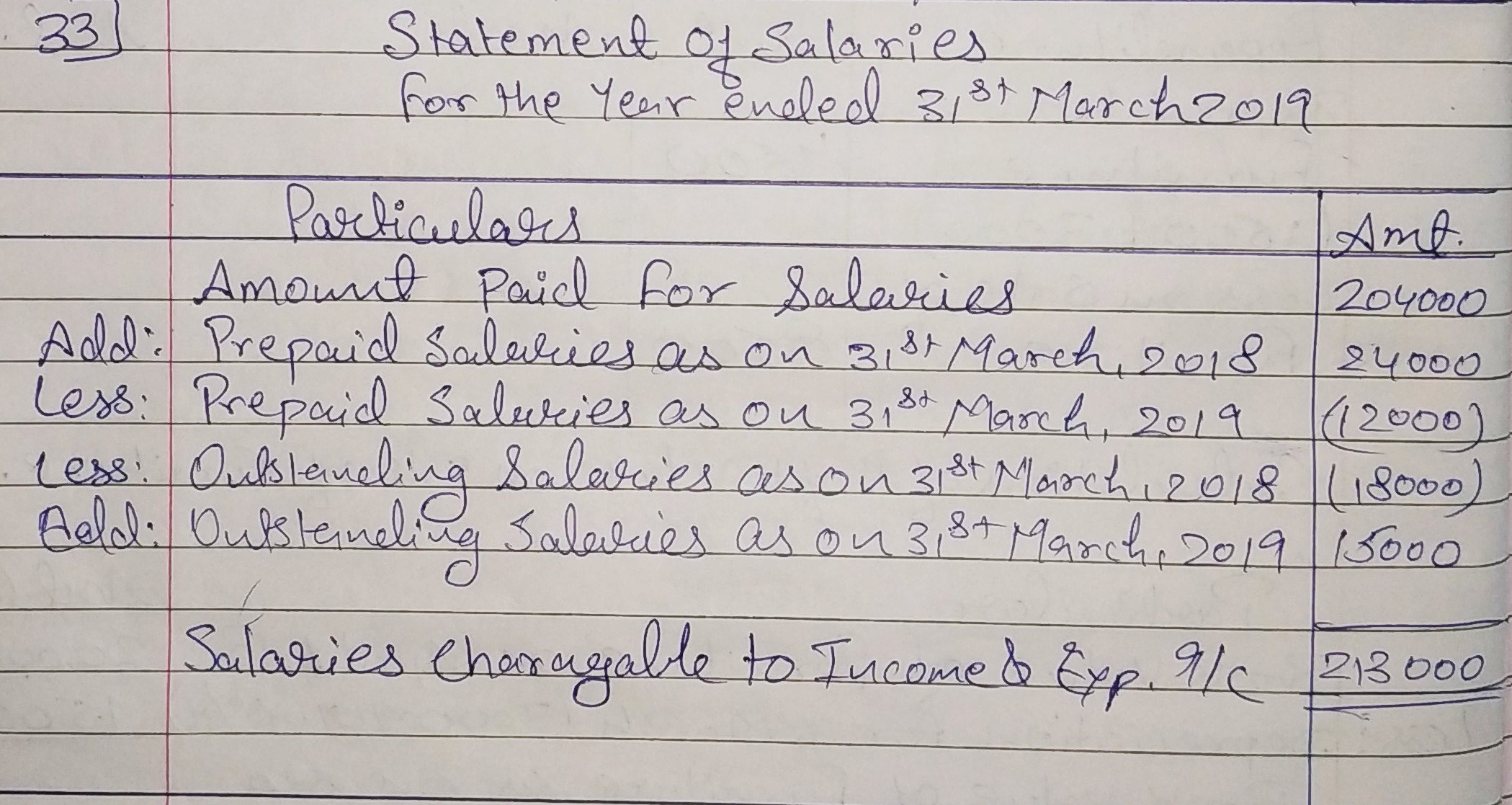

Question 33:

In the year ended 31st March, 2019, salaries paid amounted to ₹ 2,04,000. Ascertain the amount chargeable to the Income and Expenditure Account for the year ended 31st March, 2019 from the following additional information:

| ₹ | |

| Prepaid Salaries on 31st March, 2018 | 24,000 |

| Prepaid Salaries on 31st March, 2019 | 12,000 |

| Outstanding Salaries on 31st March, 2018 | 18,000 |

| Outstanding Salaries on 31st March, 2019 | 15,000 |

ANSWER:

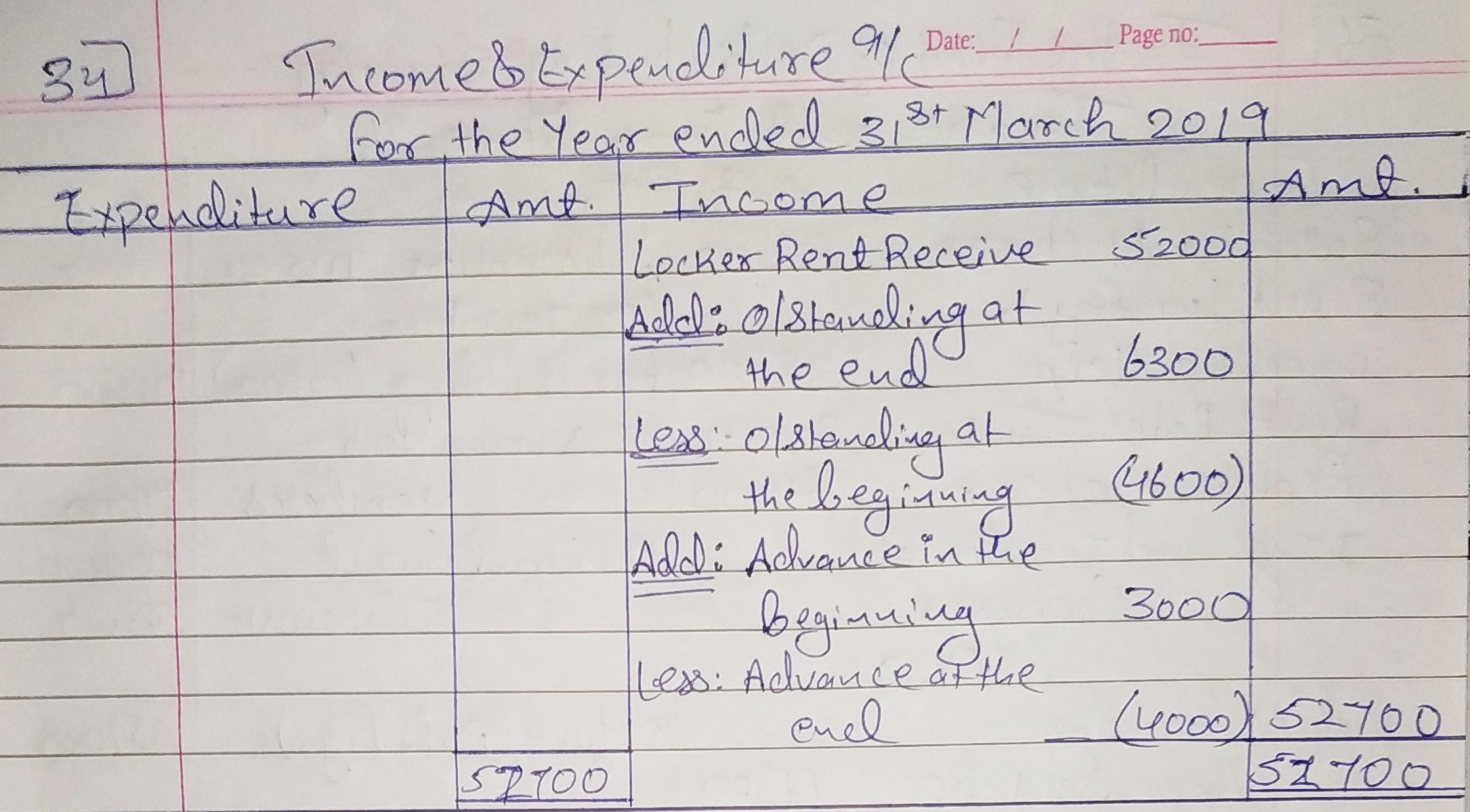

Question 34:

How are the following items dealt with while preparing Income and Expenditure Account of a club for the year ended 31st March, 2019?

| 1st April, 2018 | 31st March, 2019 | |

| Outstanding Locker Rent | ₹ 4,600 | ₹ 6,300 |

| Advance Locker Rent | ₹ 3,000 | ₹ 4,000 |

Locker Rent received during the year ended 31st March, 2019 – ₹ 52,000.

ANSWER:

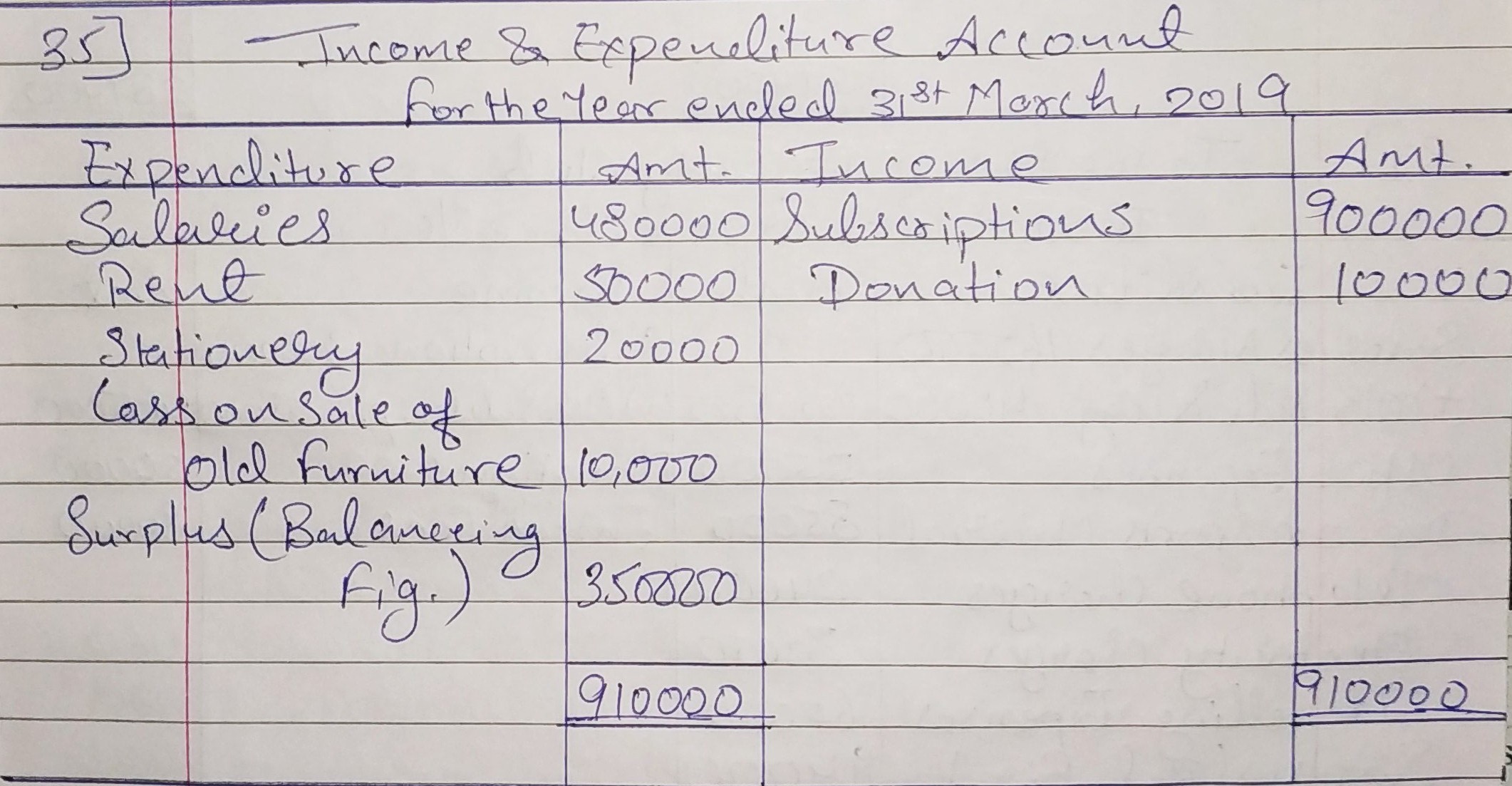

Question 35:

Prepare Income and Expenditure Account for the year ended 31st March, 2019 from the following:

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Balanceb/d (cash) | 1,80,000 | By Salaries | 4,80,000 | ||

| To Subscriptions | 9,00,000 | By Rent | 50,000 | ||

| To Sale of Investments | 2,00,000 | By Stationery | 20,000 | ||

| To Sale of Old Furniture (Book Value ₹ 40,000) | 30,000 | By Defence Bonds | 3,00,000 | ||

| To Donations | 10,000 | By Furniture | 2,00,000 | ||

| By Bicycles | 30,000 | ||||

| By Balance c/d (Cash) | 2,40,000 | ||||

13,20,000 | 13,20,000 | ||||

ANSWER:

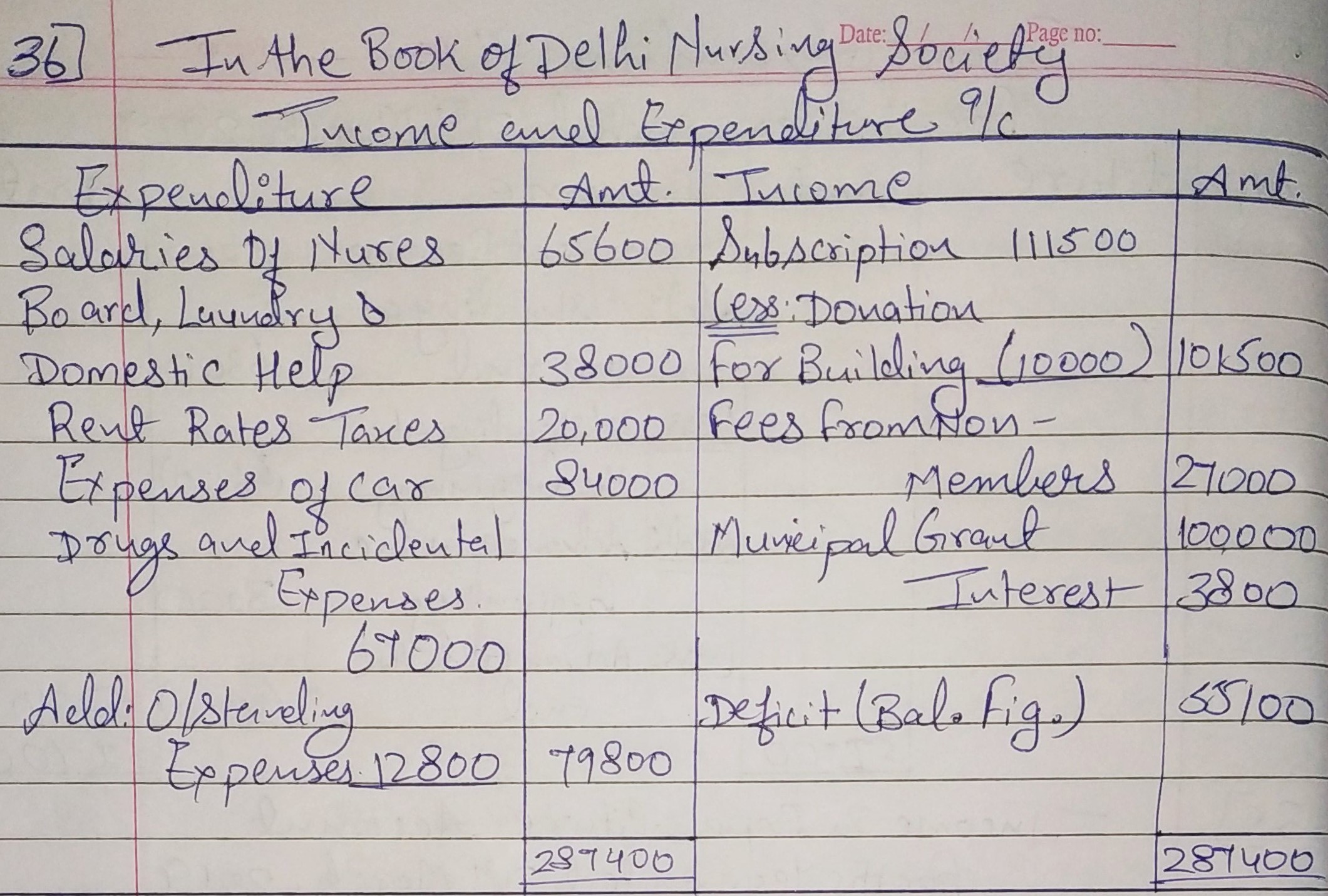

Question 36:

Prepare Income and Expenditure Account from the following Receipts and Payments Account of Delhi Nursing Society for the year ended 31st March, 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Balance b/d (Cash at Bank) | 2,01,000 | By Salaries of Nurses | 65,600 | ||

| 1,11,500 | 38,000 | ||||

| 27,000 | 20,000 | ||||

| 1,00,000 | 2,00,000 | ||||

| 1,56,000 | 84,000 | ||||

| 3,800 | 67,000 | ||||

| 1,24,700 | |||||

5,99,300 | 5,99,300 | ||||

Donation of ₹ 10,000 received for Building Fund was wrongly included in the Subscriptions Account. A bill of medicines purchased during the year amounted to ₹12,800 was outstanding. Government Grant is not for a specific purpose.

ANSWER:

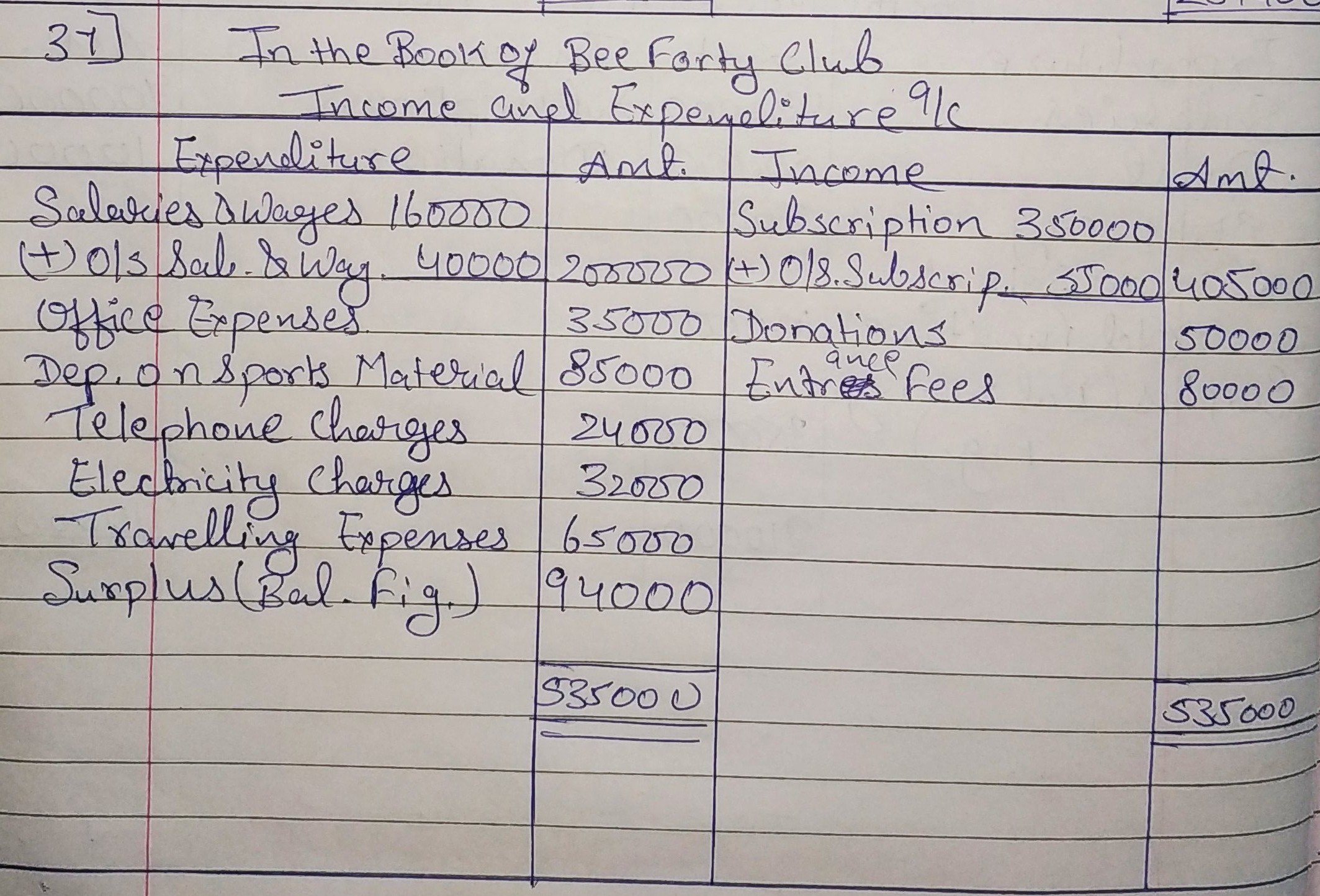

Question 37:

Following is the Receipts and Payments Account of You Bee Forty Club for the year ended 31st March, 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Balance b/d (cash) | 1,50,000 | By Salaries and Wages | 1,60,000 | ||

| To Subscriptions | By Office Expenses | 35,000 | |||

| 2016-2017 | 60,000 | By Sports Equipments | 3,40,000 | ||

| 2018-2019 | 3,50,000 | By Telephone Charges | 24,000 | ||

| To Donations | 50,000 | By Electricity Charges | 32,000 | ||

| To Entrance Fees | 80,000 | By Travelling Expenses | 65,000 | ||

| By Balance c/d (Cash) | 34,000 | ||||

| 6,90,000 | 6,90,000 | ||||

Additional information :

(a) Outstanding Subscriptions for the year ended 31st March, 2019 – ₹ 55,000.

(b) Outstanding Salaries and Wages – ₹ 40,000.

(c) Depreciate Sports Equipments by 25%.

Prepare Income and Expenditure Account of the Club from the above particulars.

ANSWER:

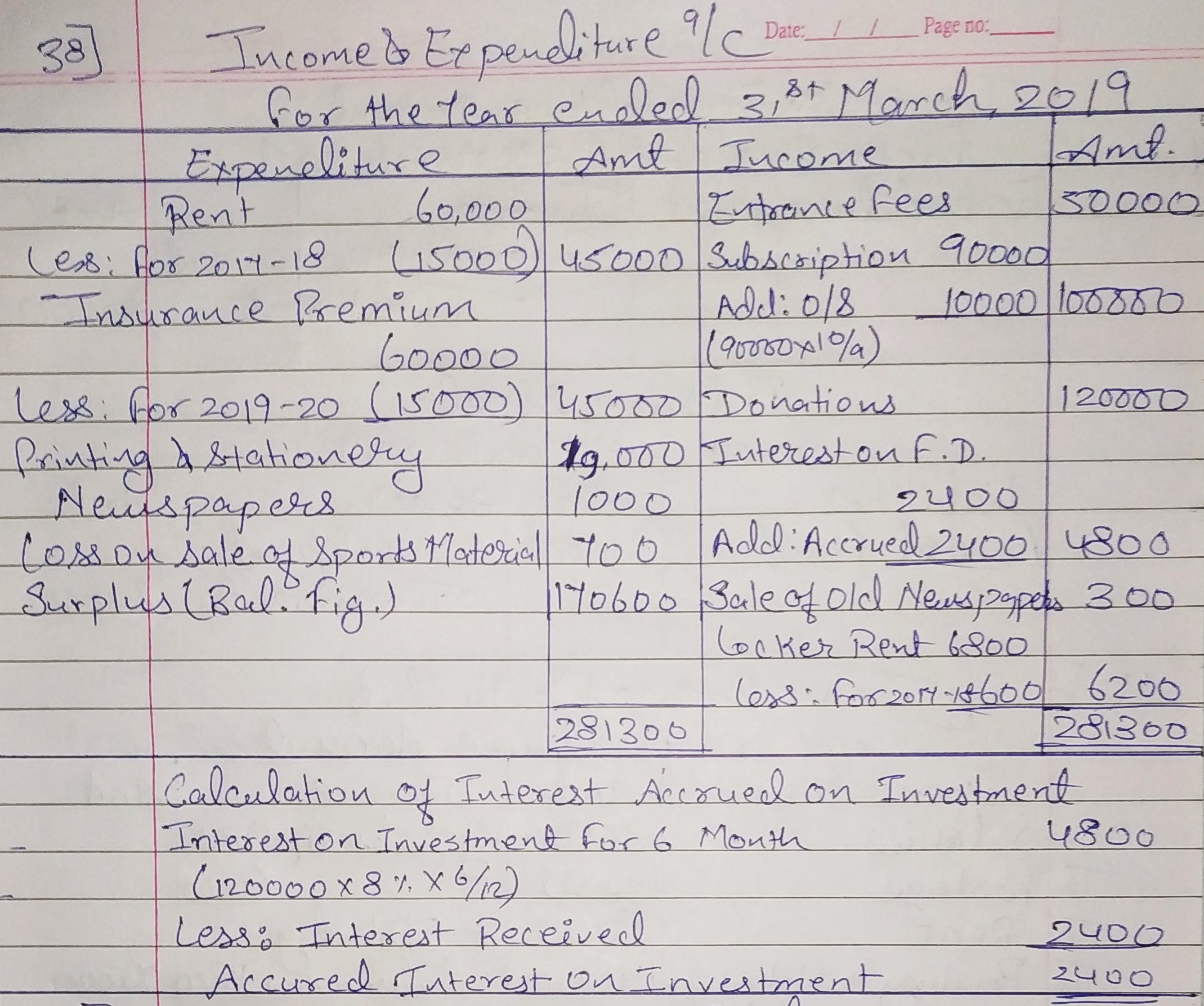

Question 38:

From the following Receipts and Payments Account of Jaipur Sports Club, prepare Income and Expenditure Account for the year ended 31st March, 2019:

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ANSWER:

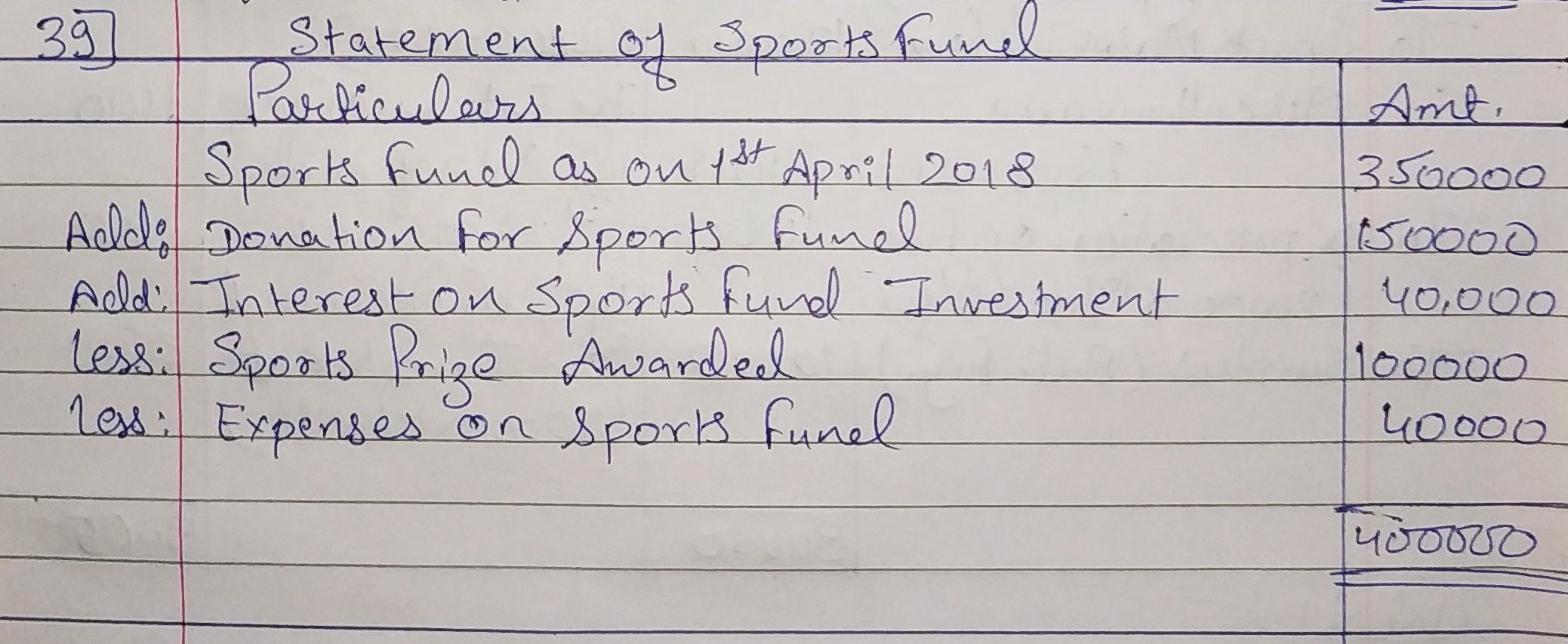

Question 39:

Following is the information given in respect of certain items of a Sports Club. Show these items in the Income and Expenditure Account and the Balance Sheet of the Club as at 31st March, 2019:

| Particulars | ₹ |

| Sports Fund as on 1st April, 2018 | 3,50,000 |

| Sports Fund Investments | 3,50,000 |

| Interest on Sports Fund Investments | 40,000 |

| Donations for Sports Fund | 1,50,000 |

| Sports Prizes awarded | 1,00,000 |

| Expenses on Sports Events | 40,000 |

| General Fund | 8,00,000 |

| General Fund Investments | 8,00,000 |

| Interest on General Fund Investments | 80,000 |

ANSWER:

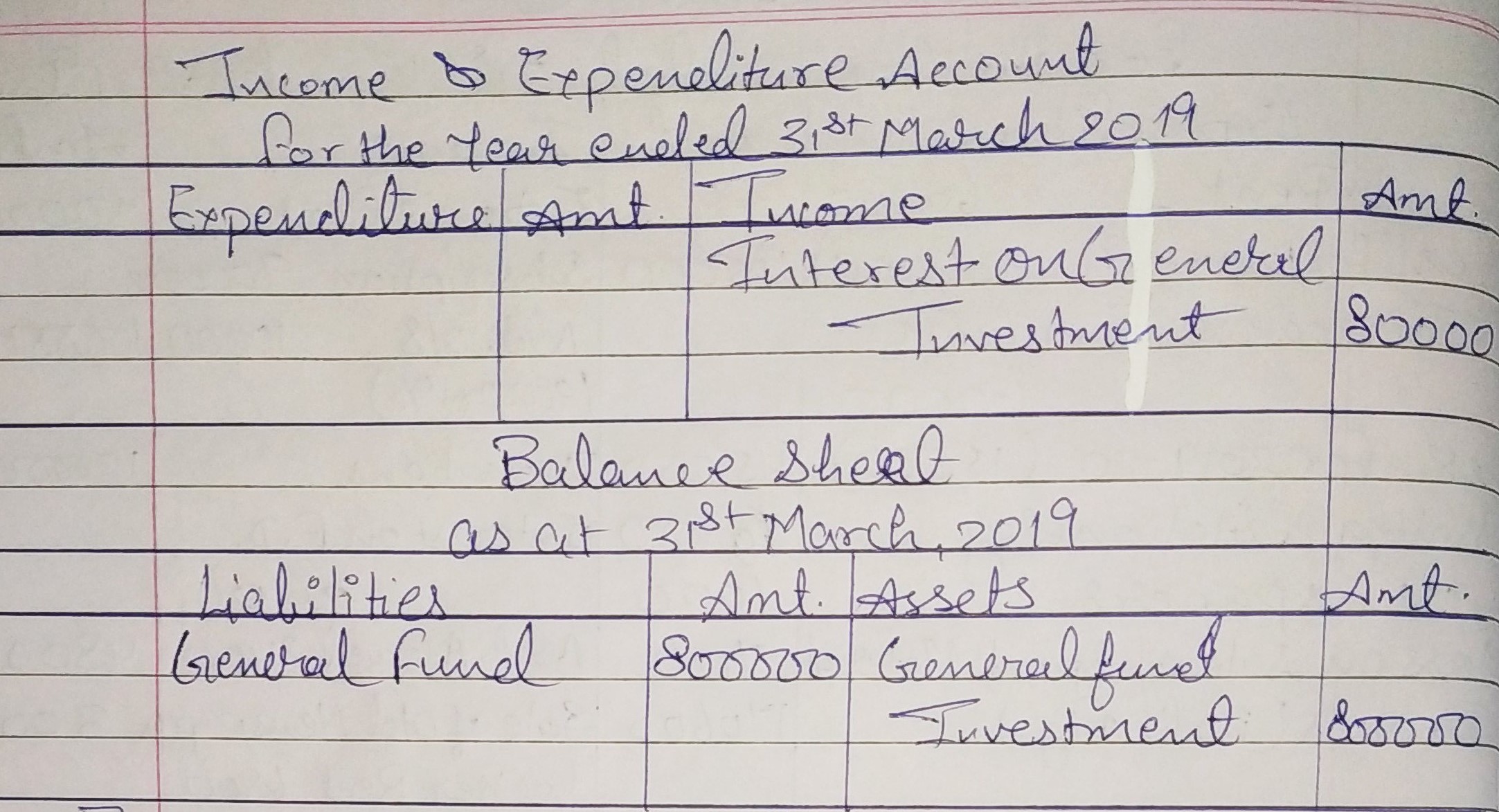

Question 40:

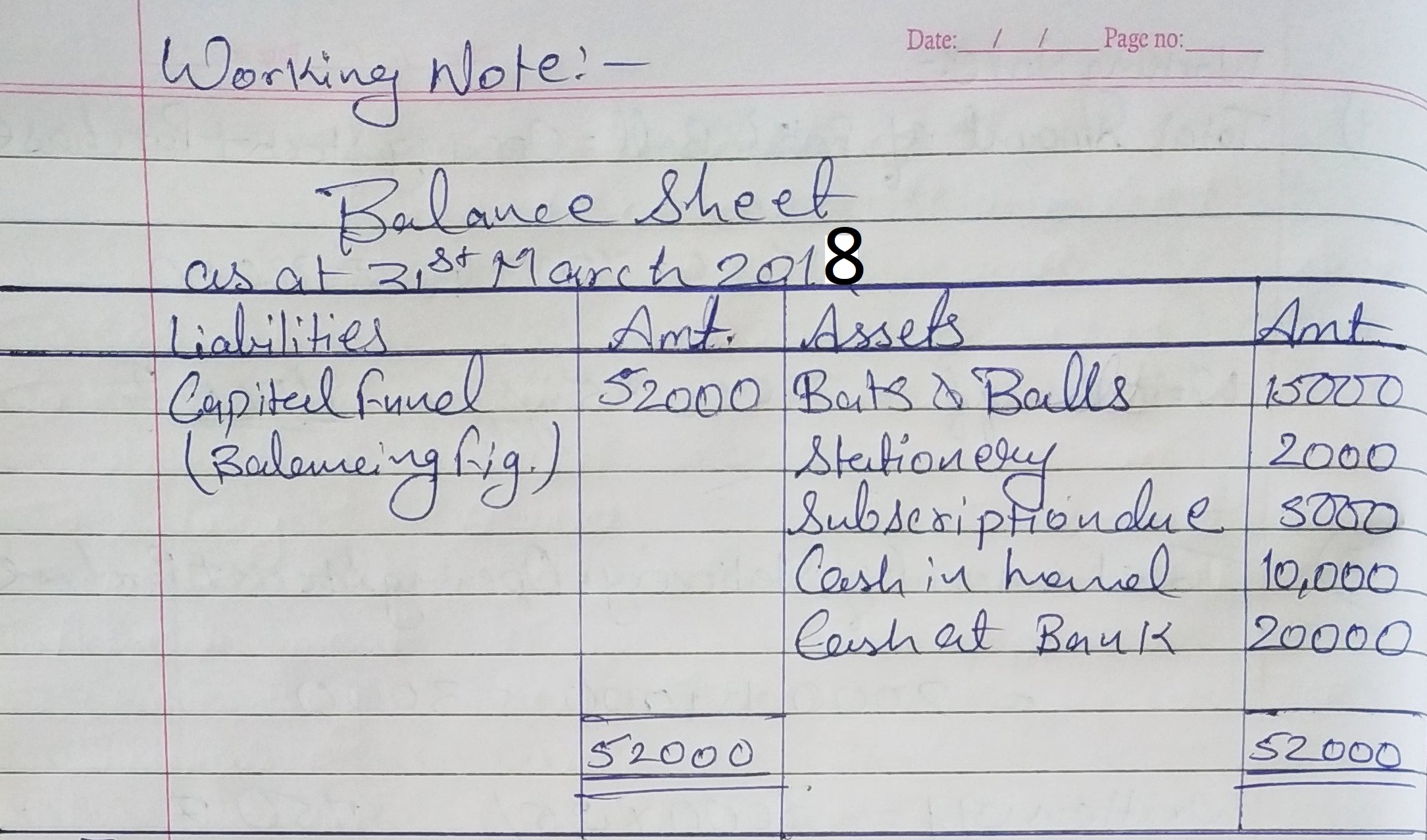

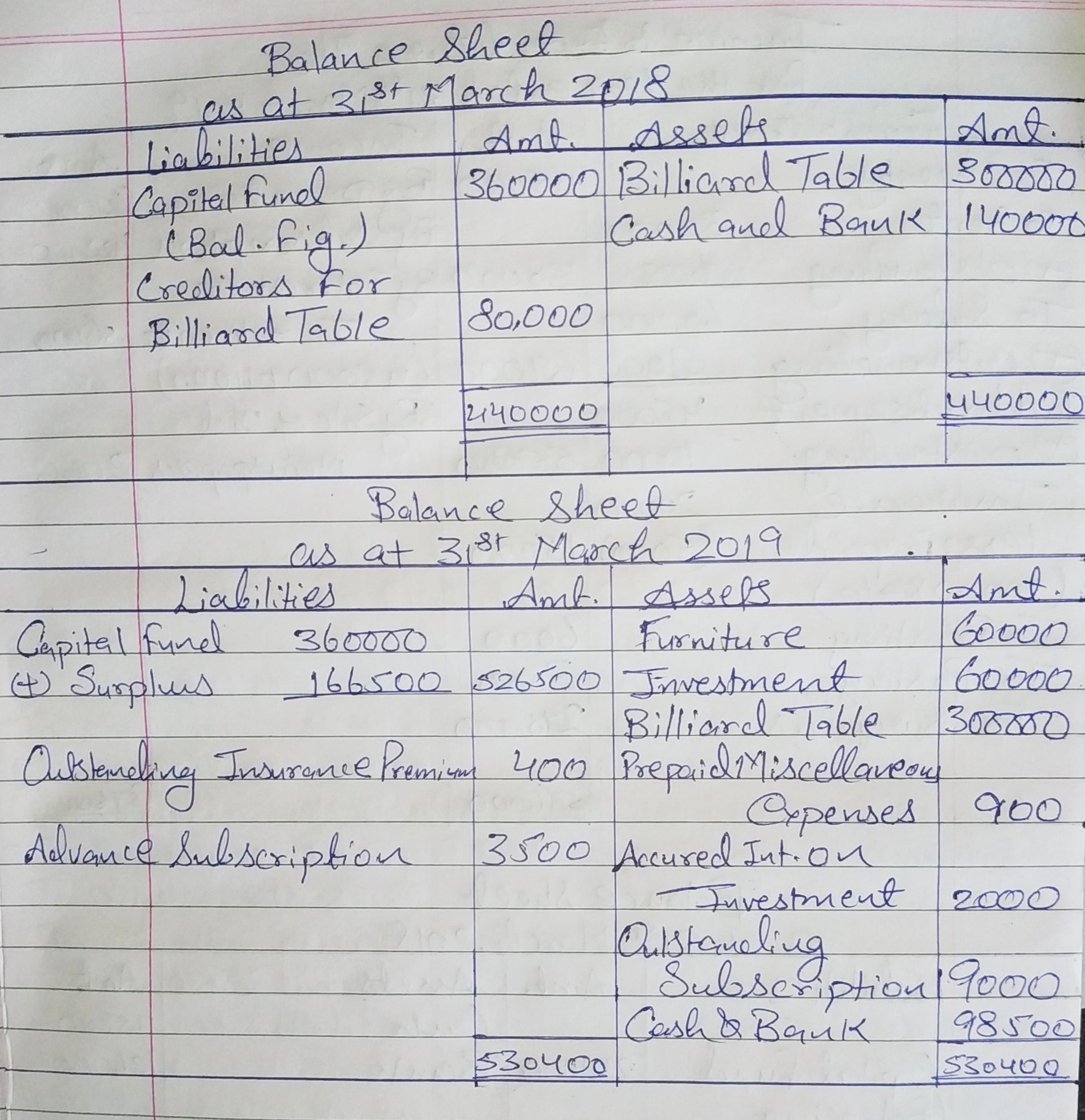

Prepare Income and Expenditure Account from the following particulars of Youth Club for the year ended on 31st March, 2018:

RECEIPTS AND PAYMENTS ACCOUNT | |||||

Dr. |

| Cr. | |||

| Receipts | ₹ | Payments | ₹ | ||

| To Balance b/d (Cash) | 32,500 | By Salaries | 31,500 | ||

| To Subscription: | By Postage | 1,250 | |||

2016-17 | 1,500 | By Rent | 9,000 | ||

2017-18 | 60,000 | By Printing and Stationery | 14,000 | ||

2018-19 | 1,800 | 63,300 | By Sports Material | 11,500 | |

| To Donations (Billiards Table) | 90,000 | Bu Miscellaneous Expenses | 3,100 | ||

| To Entrance Fees | 1,100 | By Furniture (1st October, 2017) | 20,000 | ||

| To Sale of Old Magazines | 450 | By 10% Investment (1st October, 2017) | 70,000 | ||

| By Balance c/d (31st March, 2018) | 27,000 | ||||

| 1,87,350 | 1,87,350 | ||||

Additional Information:

(i) Subscription outstanding as at 31st March, 2018 ₹ 16,200.

(ii) ₹ 1,200 is still in arrears for the year 2016-17 for subscription.

(iii) Value of sports material at the beginning and at the end of the year was ₹ 3,000 and ₹ 4,500 respectively.

(iv) Depreciation to be provided @ 10% p.a. on furniture.

ANSWER:

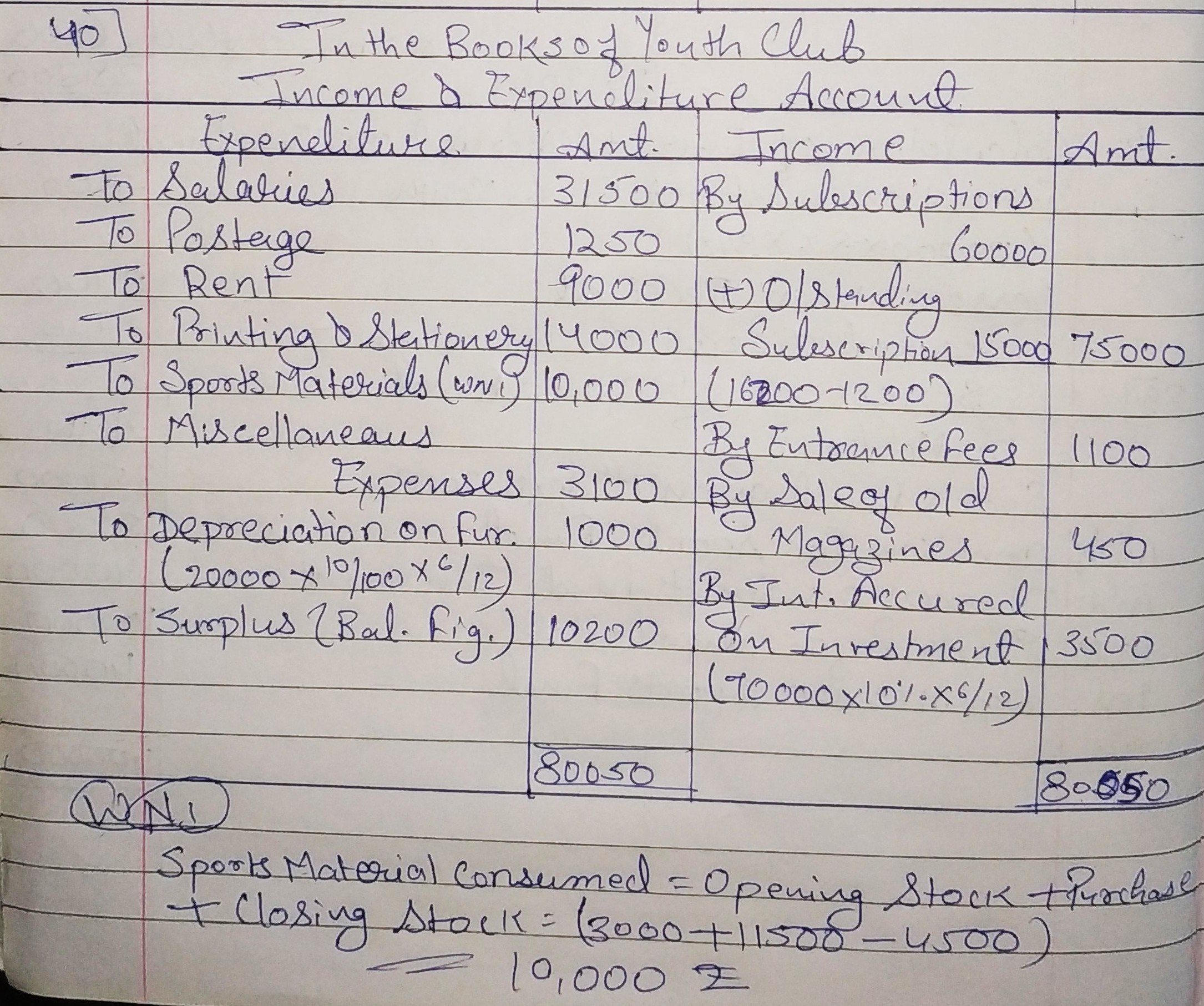

Question 41:

Following is the Receipts and Payments Account of Delhi Football Club for the year ended 31st March, 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Balance b/d (Cash) | 18,000 | By Building | 4,00,000 | ||

| To Donations for Building | 4,50,000 | By Project Expenses | 90,000 | ||

| To Donations | 50,000 | (Young Talent Search and Development) | |||

| To Government Grant | 1,00,000 | By Match Expenses | 90,000 | ||

| (Young Talent Search and Development) | By Furniture | 1,21,000 | |||

| To Life Membership Fees | 40,000 | By 10% Investments | 1,60,000 | ||

| To Match Fund | 80,000 | (Purchased on 1st July, 2018) | |||

| To Subscriptions | 52,000 | By Salaries | 70,000 | ||

| To Locker Rent | 4,000 | By Insurance | 3,500 | ||

| To Interest on Investments | 10,000 | By Sundry Expenses | 4,700 | ||

| To Sale of Furniture | 1,00,000 | By Closing c/d (Cash) | 4,800 | ||

| (Book value ₹ 80,000) | By Bank (Young Talent | 10,000 | |||

| To Entrance Fees | 50,000 | Search and Development | |||

9,54,000 | 9,54,000 | ||||

Additional Information:

(i) During the year ended 31st March, 2019, the club had 550 members and each paying an annual subscription of ₹ 100.

(ii) Salaries Outstanding as at 1st April, 2018 were ₹ 10,000 and as at 31st March, 2019 were ₹ 5,000.

Prepare Income and Expenditure Account of the Club for the year ended 31st March, 2019.

ANSWER:

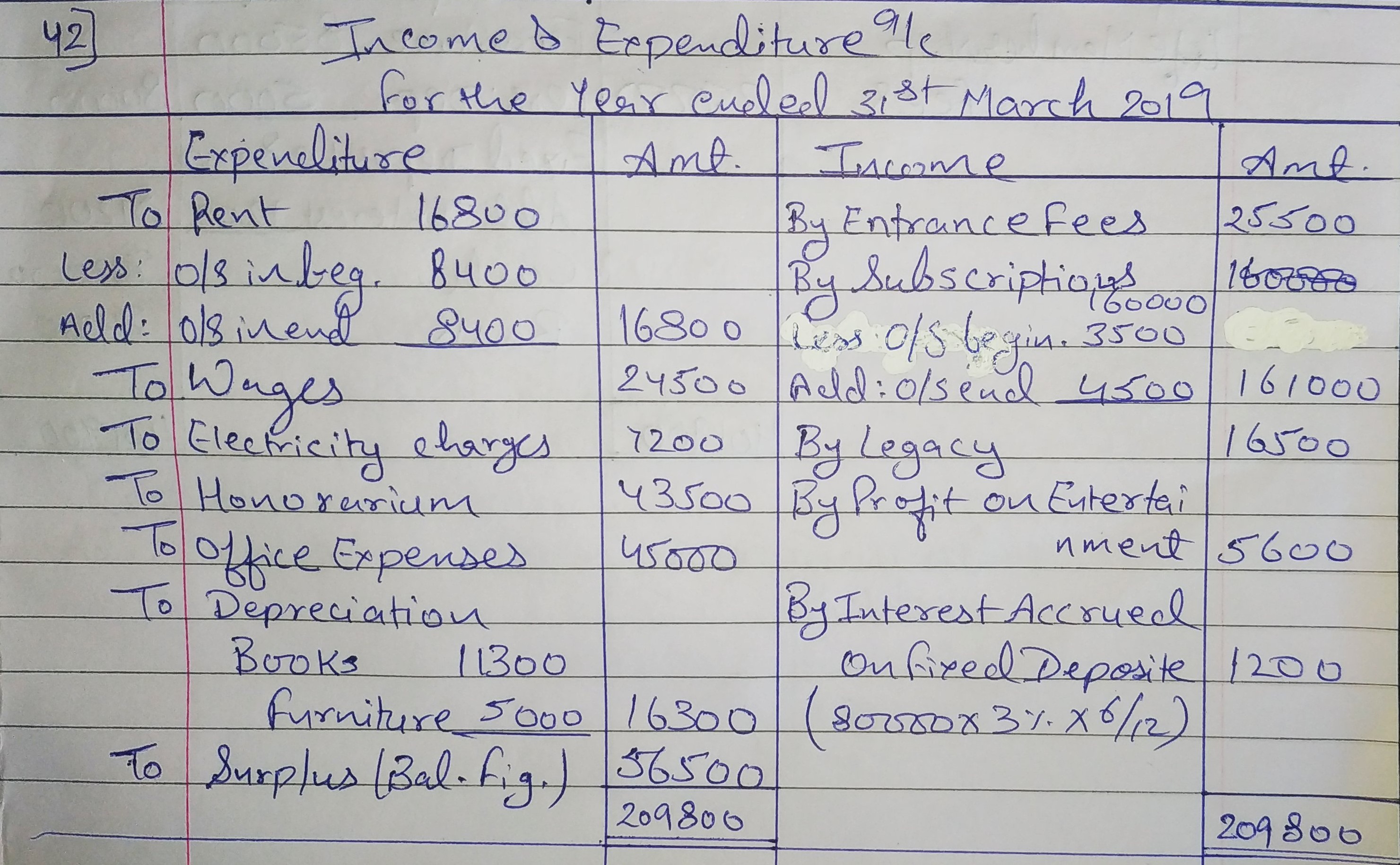

Question 42:

Following is the summary of cash transactions of the Royal Club for the year ended 31st March, 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | ||||||

| Dr. | Cr. | |||||

Receipts | ₹ | Payments | ₹ | |||

| To Balance b/d | By Rent | 16,800 | ||||

Cash in Hand | 10,000 | By Wages | 24,500 | |||

Cash at Bank | 21,900 | 31,900 | By Electricity Charges | 7,200 | ||

| To Entrance Fees | 25,500 | By Honorarium | 43,500 | |||

| To Subscriptions | 1,60,000 | By Books | 21,300 | |||

| To Donations | 16,500 | By Office Expenses | 45,000 | |||

| To Life Membership Fees | 25,000 | By 3% Fixed Deposit | 80,000 | |||

| To Profit on Entertainment | 5,600 | nbsp; (1st October, 2018) | ||||

| By Balance c/d: | 24,200 | |||||

| By Balance c/d | 2,000 | |||||

| Cash in Hand | 2,000 | |||||

| Cash at Bank | 24,200 | 26,200 | ||||

2,64,500 | 2,64,500 | |||||

In the beginning of the year, the club possessed Books of ₹ 2,00,000 and Furniture of ₹ 85,000. Subscriptions in arrears in the beginning of the year amounted to ₹ 3,500 and at the end of the year ₹ 4,500 and six months Rent was due both in the beginning of the year and at the end of the year.

Prepare Income and Expenditure Account of the club for the year ended 31st March, 2019 and its Balance Sheet as at that date after writing off ₹ 5,000 and ₹ 11,300 on Furniture and books respectively.

ANSWER:

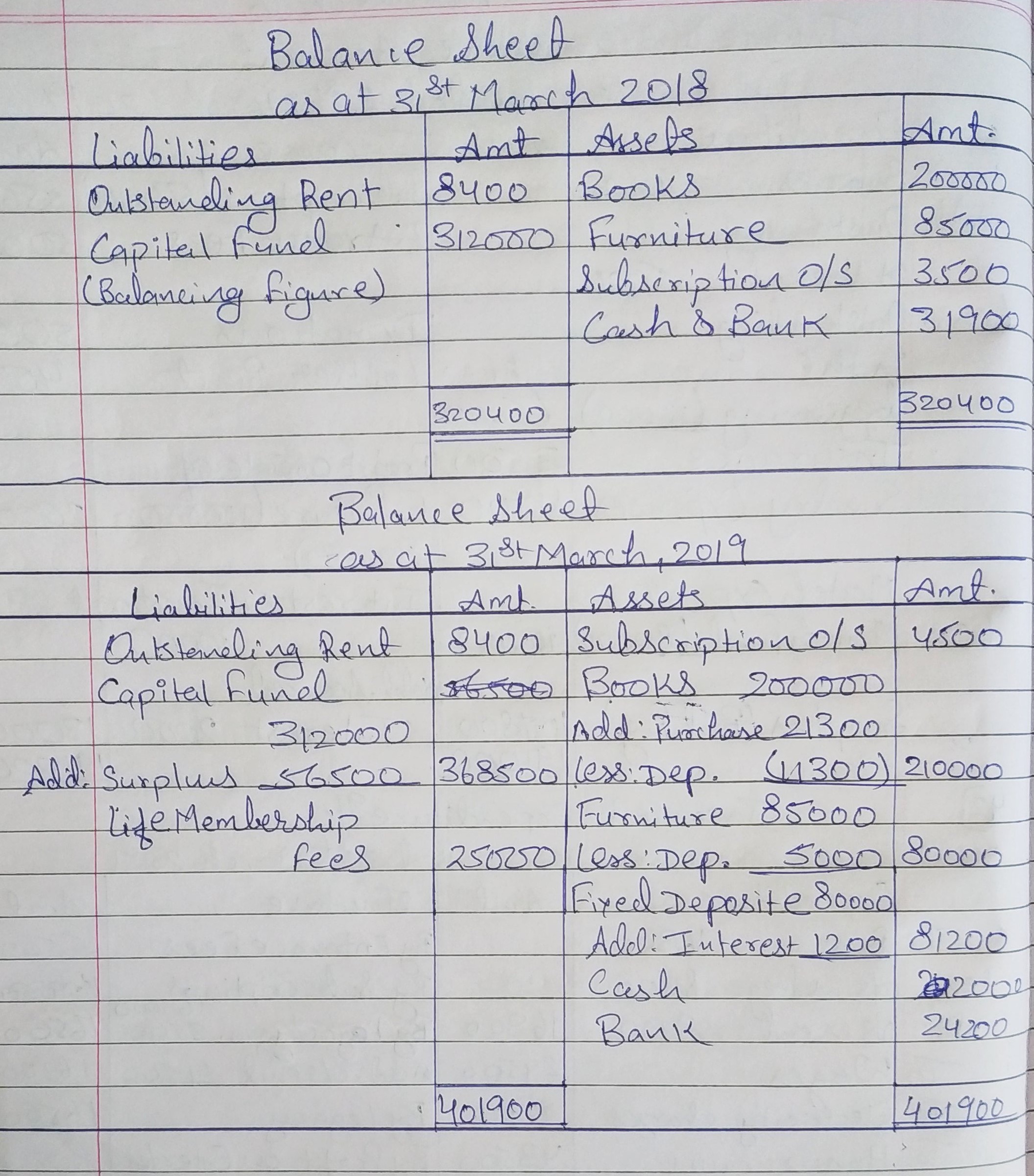

Question 43:

From the following Receipts and Payments Account of Social Club and the information supplied, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date:

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March ,2019 | |||||

| Dr. |

|

| Cr. | ||

| Receipts | (₹) | Payments | (₹) | ||

| To Balance b/d | 7,000 | By Salaries | 28,000 | ||

| To Subscriptions: |

| By General Expenses | 6,000 | ||

2017-18 | 5,000 | By Electricity Charges | 4,000 | ||

2018-19 | 20,000 | By Books | 10,000 | ||

2019-20 | 4,000 | 29,000 | By Newspapers | 8,000 | |

| To Hire of Ground | 14,000 | By Balance c/d | 4,000 | ||

| To Surplus from Entertainment Events | 8,000 | ||||

| To Sale of Old Newspapers | 2,000 |

| |||

60,000 | 60,000 | ||||

(a) The club has 50 members each paying an annual subscription of ₹ 500. Subscriptions Outstanding on 31st March,2018 were ₹ 6,000.

(b) On 31st March, 2019, Salaries Outstanding amounted to ₹ 2,000. Salaries paid in the year ended 31st March, 2019 included ₹ 6,000 for the year ended 31st March, 2018.

(c) On 1st April, 2018, the club owned Building valued at ₹ 2,00,000; Furniture ₹ 20,000 and Books ₹ 20,000.

(d) Provide depreciation on Furniture at 10%.

ANSWER:

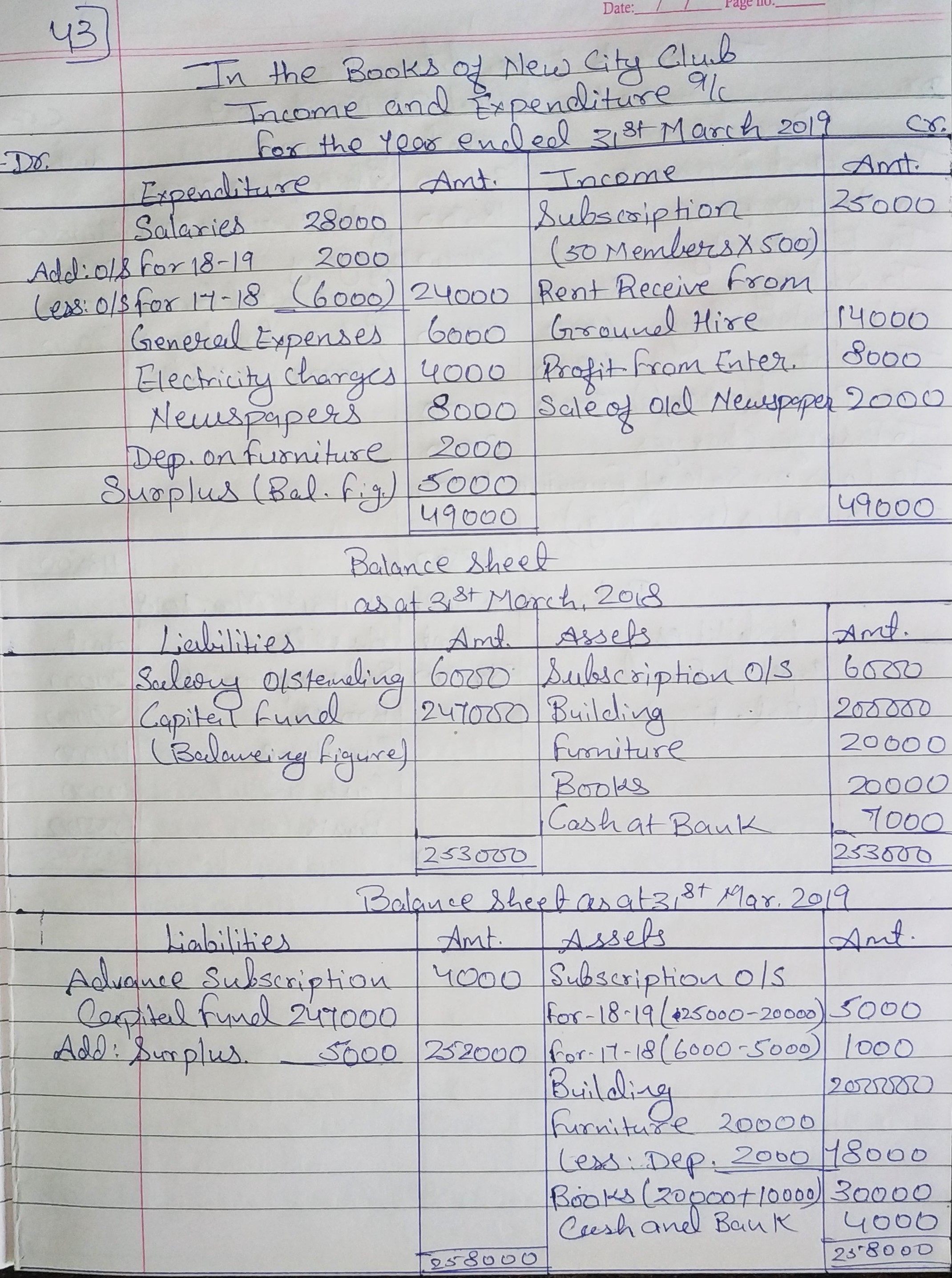

Question 44:

From the following Receipts and Payments Account and additional information given below, prepare Income and Expenditure Account and Balance Sheet of Rural Literacy Society as on 31st March, 2019:

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31 st March, 2019 | |||||

| Dr. |

|

| Cr. | ||

| Receipts | Amount | Payments | Amount | ||

| To Balance b/d: | By General Expenses | 32,000 | |||

Cash in Hand | 40,000 | By Newspaper | 18,500 | ||

Cash at Bank | 1,55,500 | By Electricity | 30,000 | ||

| To Subscriptions: |

| By Fixed Deposit with Bank | 1,80,000 | ||

2017-18 | 12,000 | (On 30th September, 2018 @ 10% p.a.) | |||

2018-19 | 2,65,000 | By Books | 70,000 | ||

2019-20 | 5,000 | 2,82,000 | By Salary | 36,000 | |

| To Legacy | 12,500 | By Rent | 65,000 | ||

| To Government Grant | 1,20,000 | By Postage Charges | 3,000 | ||

| To Sale of Old Furniture | 37,000 | By Furniture (purchased) | 1,05,000 | ||

| (Book value ₹ 50,000) | By Balance c/d: | ||||

| To Interest received on Fixed Deposit | 4,500 | Cash in Hand | 30,000 | ||

Cash at Bank | 82,000 | ||||

6,51,500 | 6,51,500 | ||||

Additional information:

(i) Subscription outstanding as on 31st March, 2018 ₹ 20,000 and on 31st March, 2019 ₹ 15,000.

(ii) On 31st March, 2019, salary outstanding ₹ 6,000 and one month rent paid in advance.

(iii) On 1st April, 2018, society owned furniture ₹ 1,20,000 and books ₹ 50,000.

ANSWER:

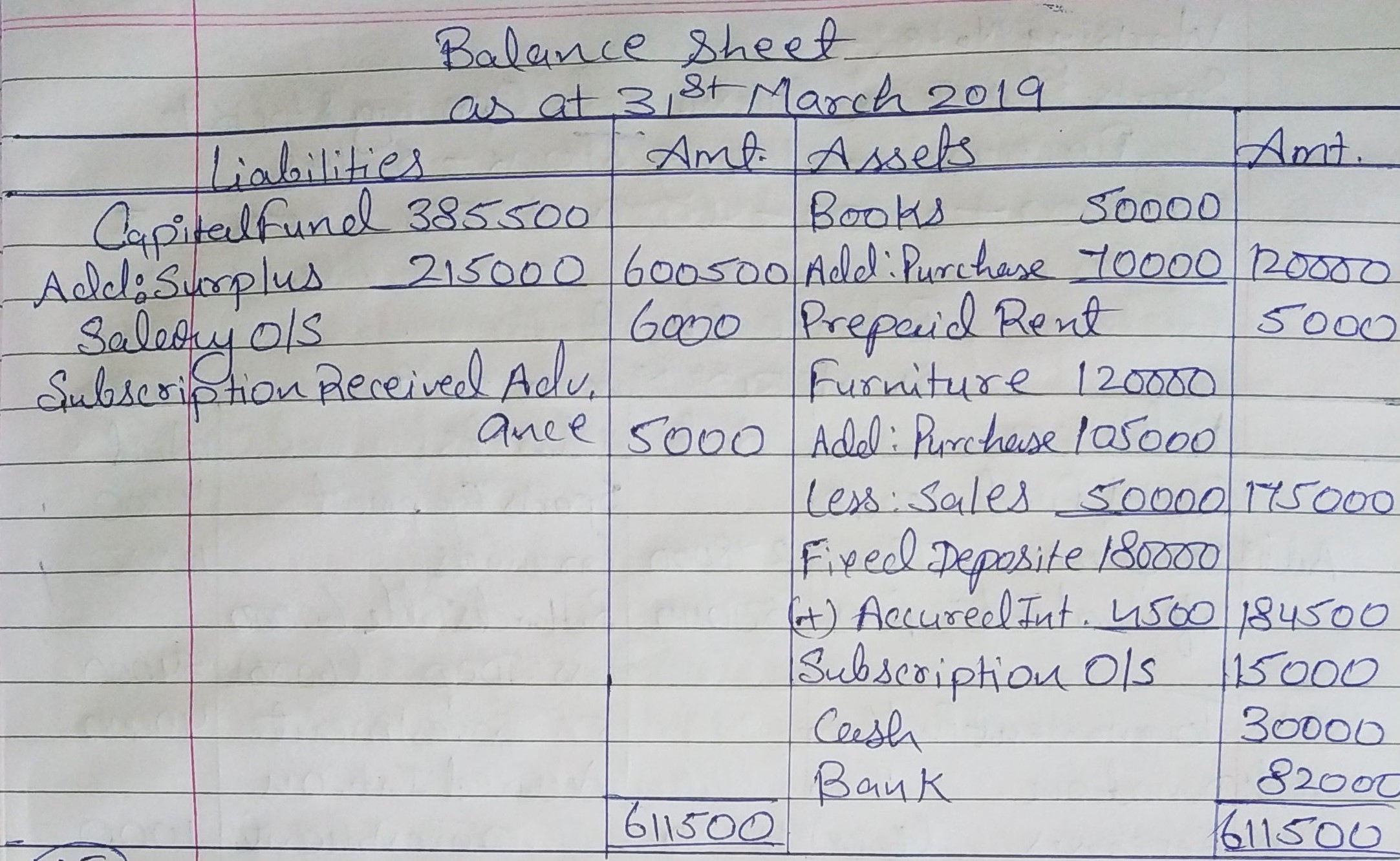

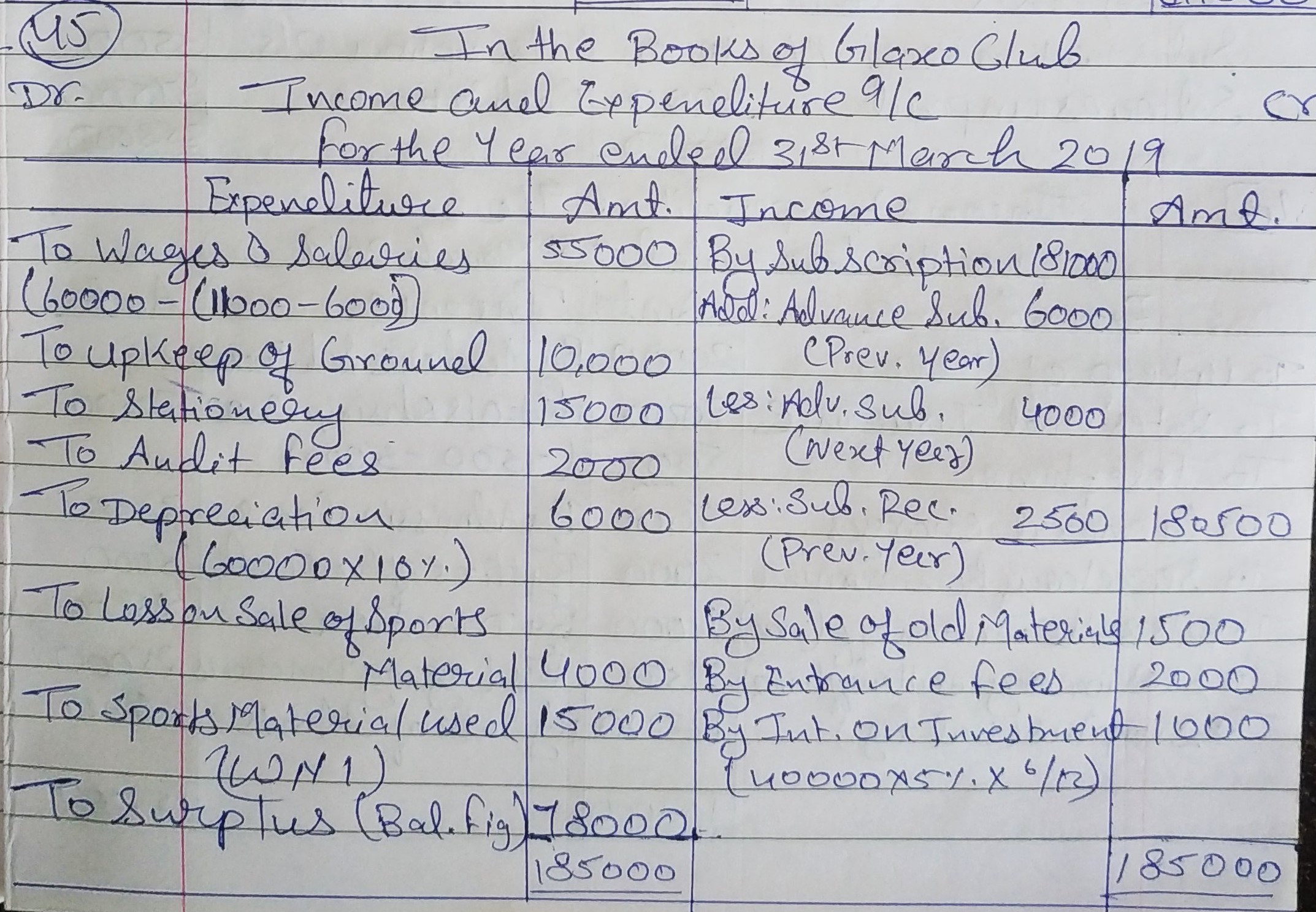

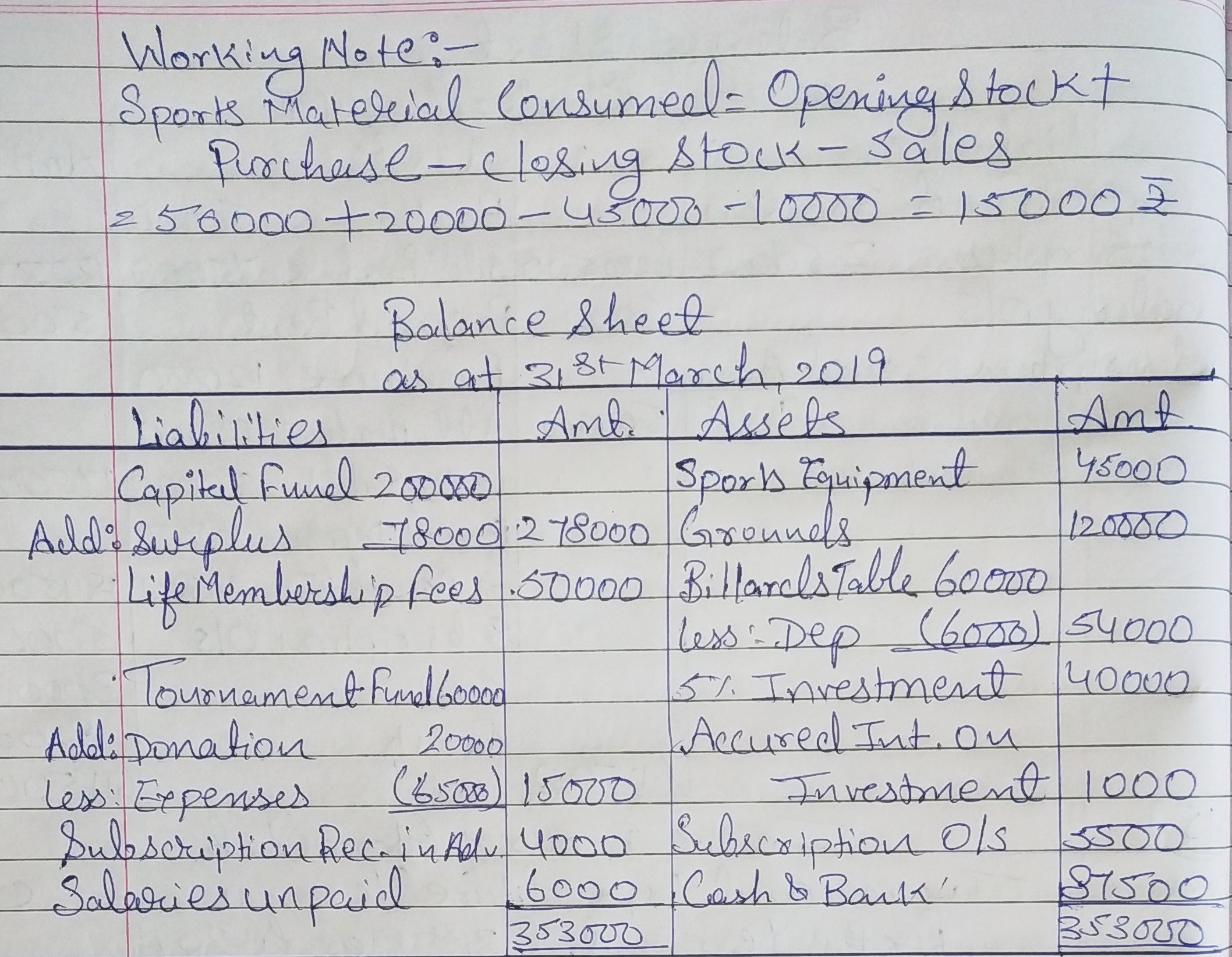

Question 45:

Glaxo Club’s Balance Sheet as at 1st April, 2018 was as under:

Liabilities | (₹) | Assets | (₹) | |

| Capital Fund | 2,00,000 | Sports Equipments | 50,000 | |

| Tournament Fund | 60,000 | Grounds | 1,20,000 | |

| Subscriptions in Advance | 6,000 | Billiards Tables | 60,000 | |

| Salaries Unpaid | 11,000 | Subscriptions Outstanding | 8,000 | |

| Cash and Bank Balances | 39,000 | |||

| 2,77,000 | 2,77,000 | |||

|

|

|

| |

Receipts and Payments Account for the year ended 31st March, 2019 was:

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. |

|

| Cr. | ||

| Receipts | (₹) | Payments | (₹) | ||

| To Opening Balance | 39,000 | By Wages and Salaries | 60,000 | ||

| To Subscriptions | 1,81,000 | By Upkeep of Grounds | 10,000 | ||

| To Sale of Old Materials | 1,500 | By Stationery | 15,000 | ||

| To Sale of Sports Equipment | 6,000 | By Audit Fee | 2,000 | ||

| (Book value ₹ 10,000) | By Expenses on Tournament | 65,000 | |||

| To Entrance Fees | 2,000 | By Sports Equipments | 20,000 | ||

| To Life Membership Fees | 50,000 | By 5% Investments | 40,000 | ||

| To Donations for Tournament | 20,000 | (On 1st October, 2018) | |||

| By Cash and Bank Balances | 87,500 | ||||

| 2,99,500 | 2,99,500 | ||||

Subscriptions still to be received are ₹ 5,500 but subscriptions already received include ₹ 4,000 for next year. Salaries still unpaid are ₹ 6,000. Sports Equipments are now valued at ₹ 45,000. Prepare Income and Expenditure Account and the Balance Sheet, after charging 10% depreciation on Billiards Tables.

ANSWER:

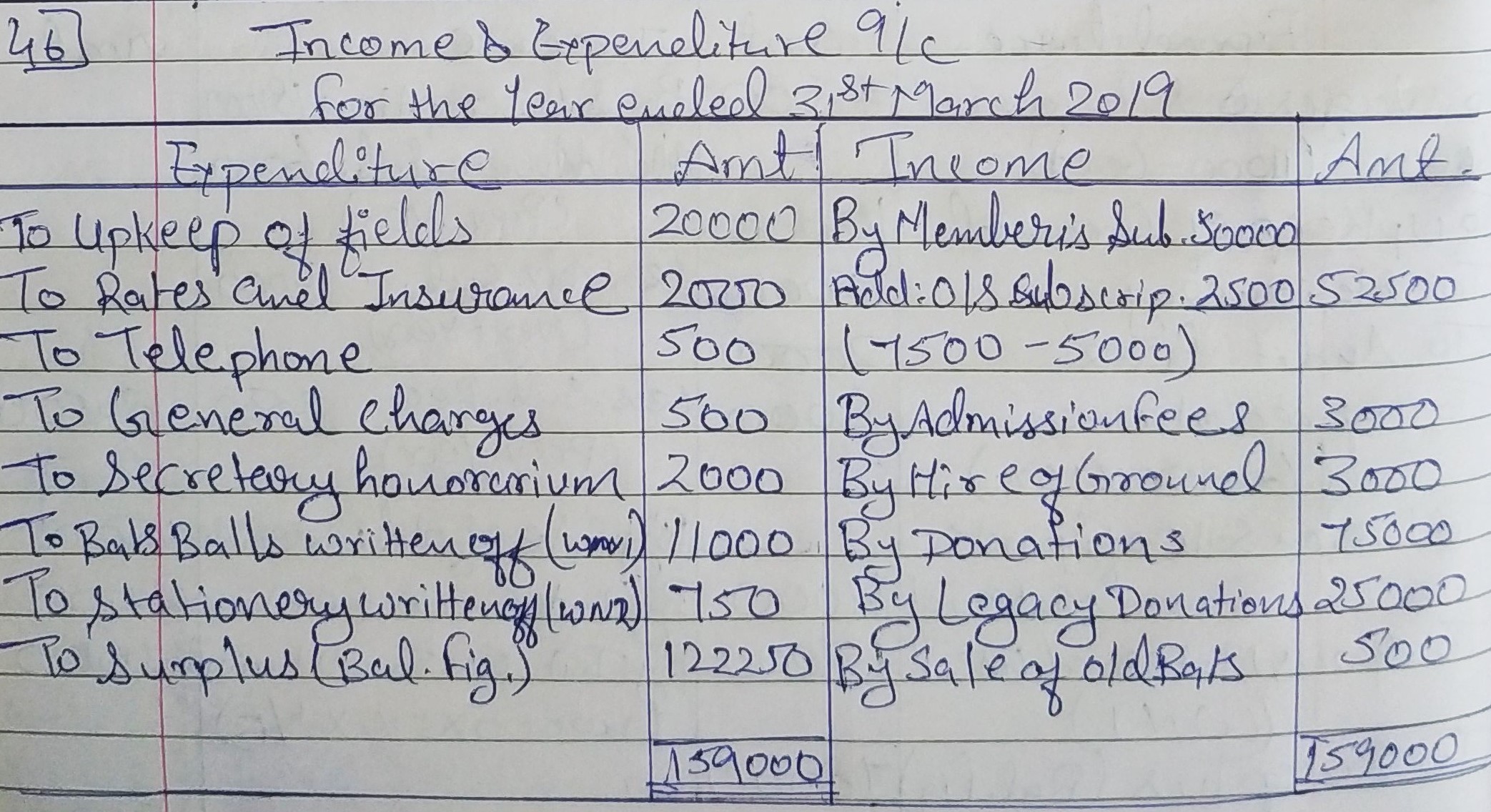

Question 46:

From the following Receipts and Payments Account and additional information relating to the star Cricket Club, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date:

RECEIPTS AND PAYMENTS ACCOUNT | |||||

| Dr. |

|

| Cr. | ||

| Receipts | (₹) | Payments | (₹) | ||

| To Balance b/d: | By Upkeep of Fields | 20,000 | |||

Cash in Hand 1st April, 2018 | 10,000 | By Tournament Expenses | 7,000 | ||

Cash at Bank as per Pass Book | 20,000 | 30,000 | By Rates and Insurance | 2,000 | |

| To Members’ Subscriptions | 50,000 | By Telephone | 500 | ||

| To Admission Fee | 3,000 | By Stationery | 1,000 | ||

| To Sale of Old Bats, etc. | 500 | By General Charges | 500 | ||

| To Hire of Ground | 3,000 | By Secretary’s Honorarium | 2,000 | ||

| To Subscriptions for Tournament | 10,000 | By Bats, Balls, etc. | 7,000 | ||

| To Donations | 75,000 | By Balance c/d: | |||

| To Legacy Donations | 25,000 | Cash in Hand 31st March, 2019 | 1,00,000 | ||

Cash at Bank as per Pass Book | 56,500 | 1,56,500 | |||

| 1,96,500 | 1,96,500 | ||||

| Assets on 1st April, 2018: | ₹ | |

| Stock of Bats and Balls | 15,000 | |

| Stationery | 2,000 | |

| Subscriptions Due | 5,000 | |

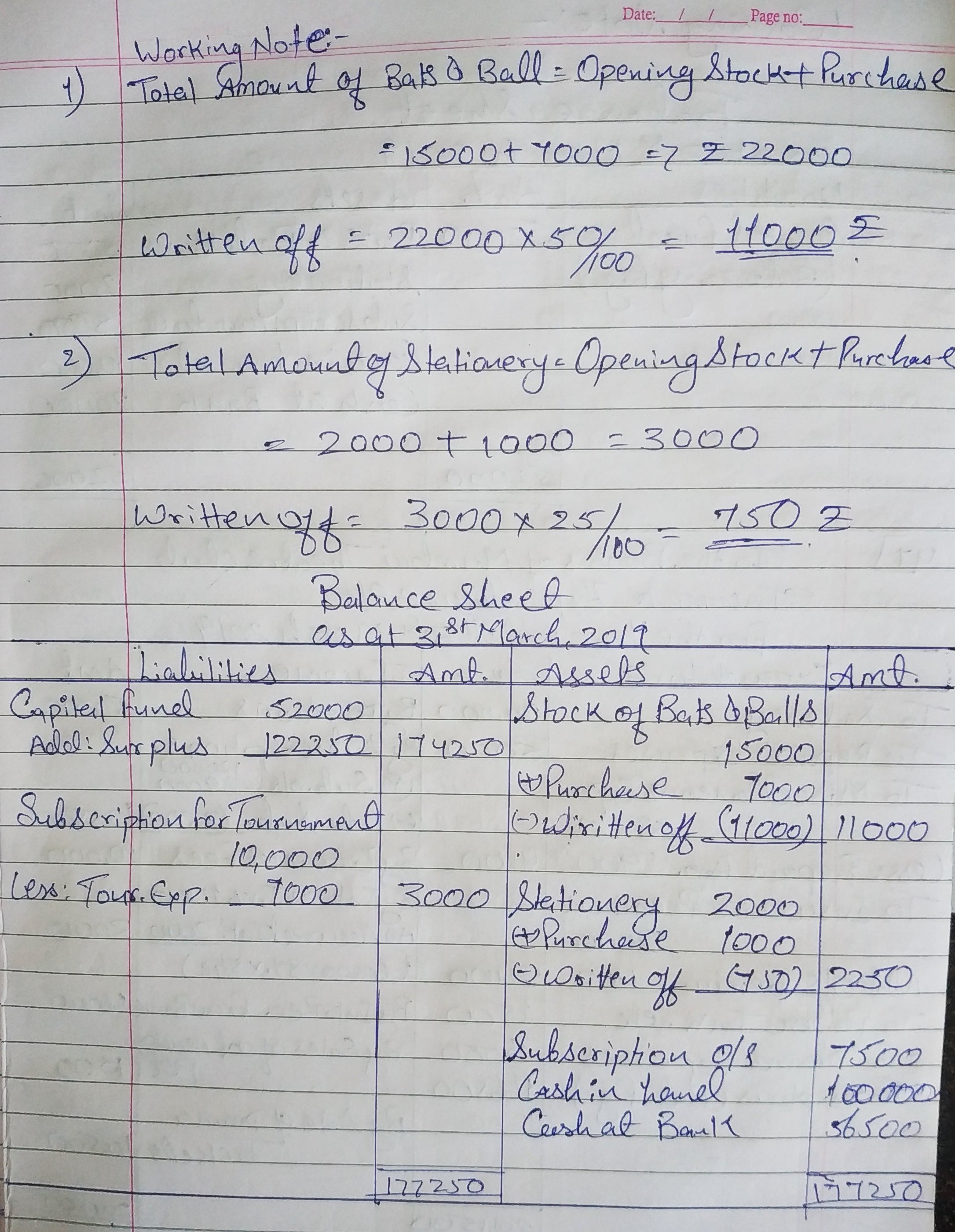

Subscriptions due on 31st March, 2019 amounted to ₹ 7,500. Write off 50% of Bats, Balls (not considering sale) and 25% of Stationery.

ANSWER:

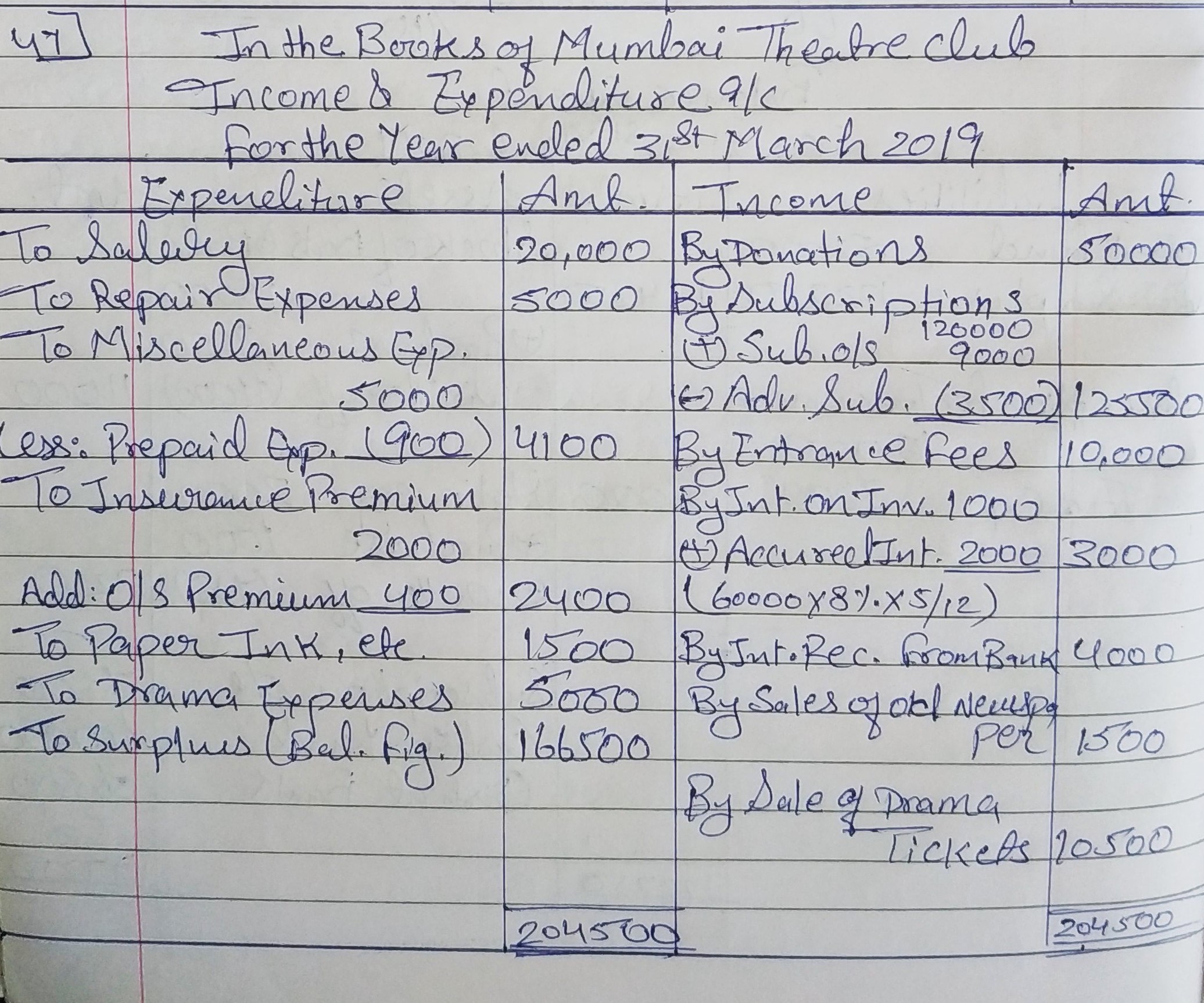

Question 47:

From the following Receipts and Payments Account of Mumbai Theatre Club, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date:

RECEIPTS AND PAYMENTS ACCOUNT | |||||

| Dr. |

|

| Cr. | ||

| Receipts | (₹) | Payments | (₹) | ||

| To Balance b/d: | By Salary | 20,000 | |||

Cash and Bank | 1,40,000 | By Repair Expenses | 5,000 | ||

| To Donations | 50,000 | By Furniture | 60,000 | ||

| To Subscriptions | 1,20,000 | By Miscellaneous Expenses | 5,000 | ||

| To Entrance Fees | 10,000 | By Investments | 60,000 | ||

| To Interest on Investments | 1,000 | By Insurance Premium | 2,000 | ||

| To Interest Received from Bank | 4,000 | By Billiard Table | 80,000 | ||

| To Sale of Old Newspapers | 1,500 | By Paper, lnk, etc. | 1,500 | ||

| To Sale of Drama Tickets | 10,500 | By Drama Expenses | 5,000 | ||

| By Balance c/d: | |||||

| Cash and Bank | 98,500 | ||||

| 3,37,000 | 3,37,000 | ||||

Additional Information:

(i) Subscriptions in arrear for the year ended 31st March, 2019 ₹ 9,000 and subscriptions in advance for the year ending 31st March, 2020 ₹ 3,500.

(ii) Insurance Premium outstanding ₹ 400.

(iii) Miscellaneous expenses prepaid ₹ 900.

(iv) 8% interest has accrued on investment for five months.

(v) Billiard Table costing ₹ 3,00,000 was purchased during last year and ₹ 2,20,000 were paid for it.

ANSWER:

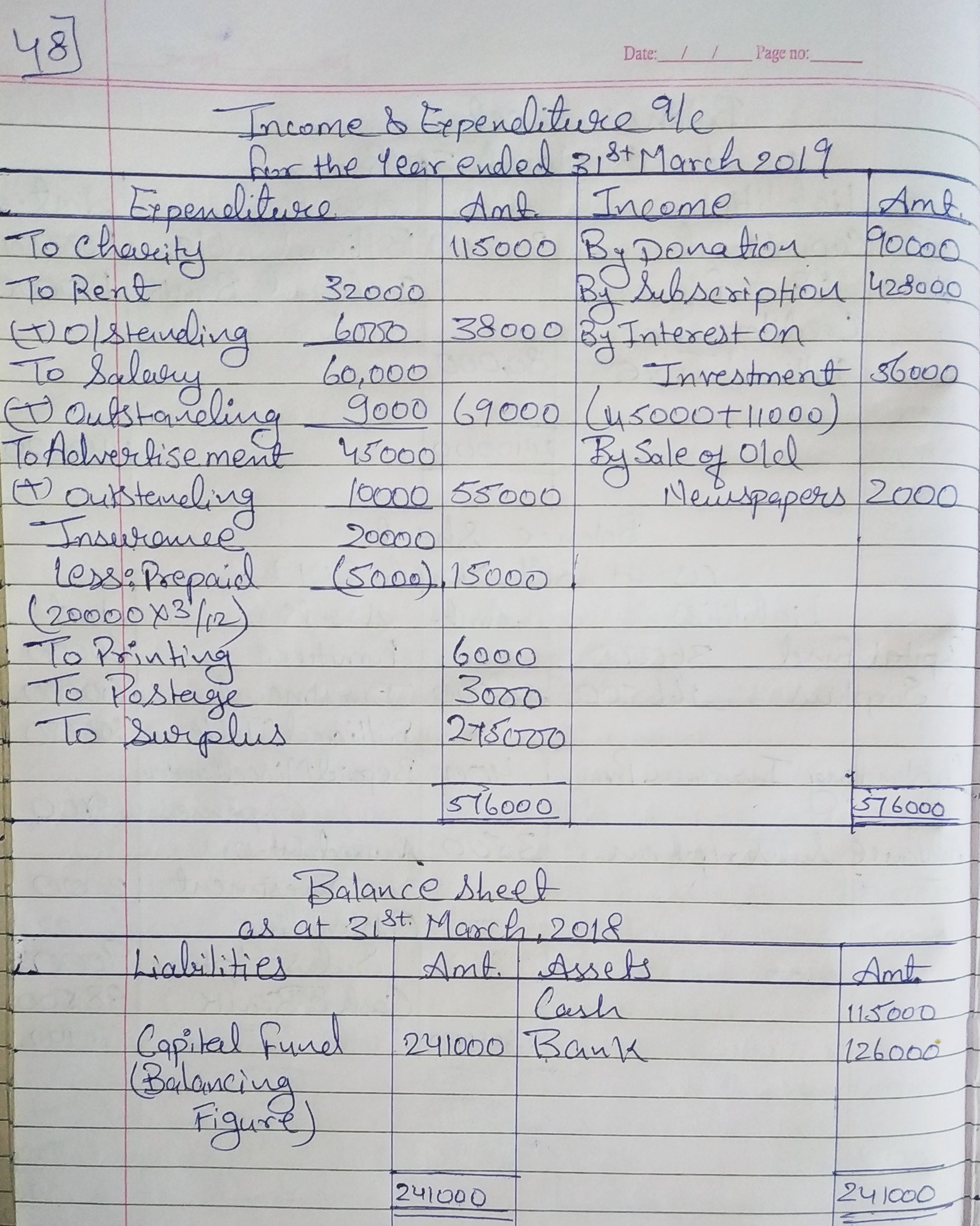

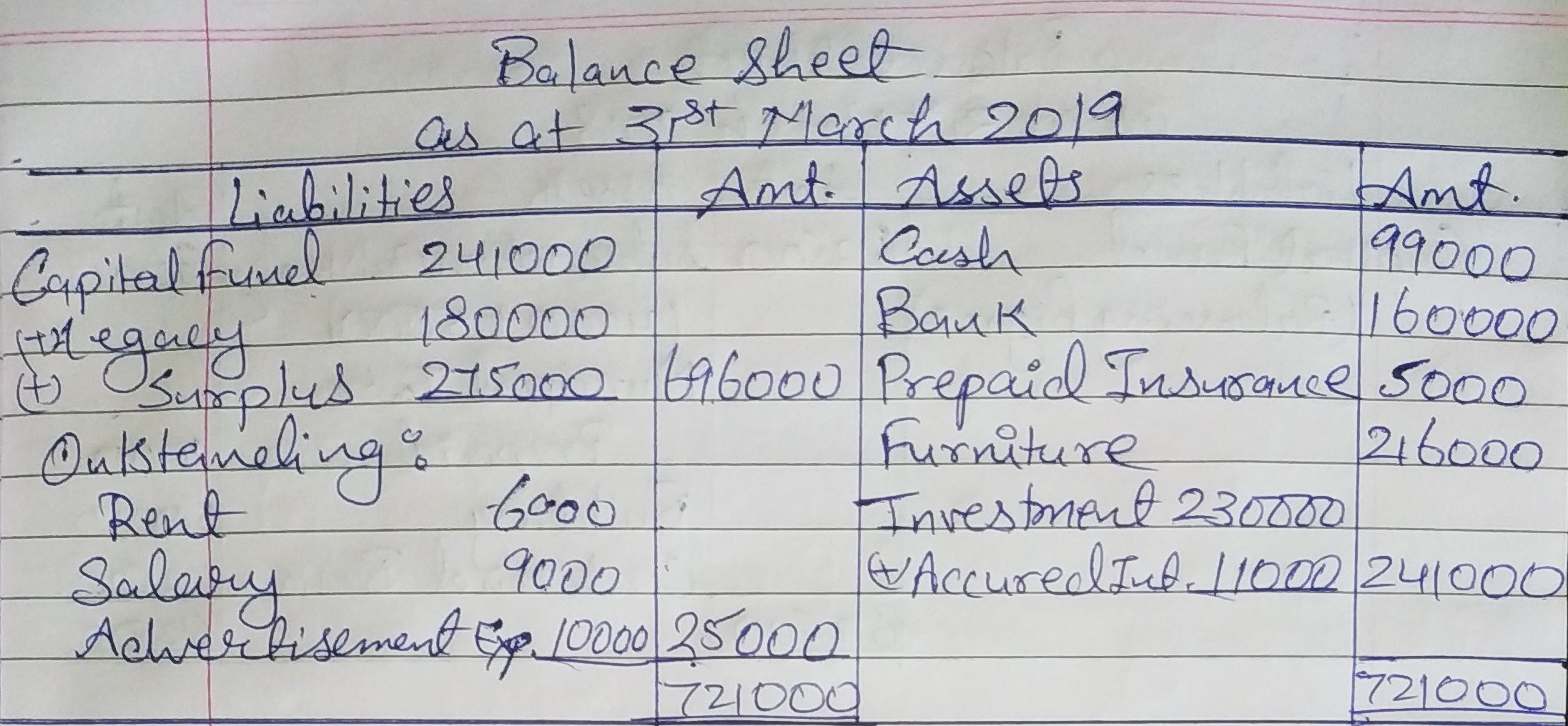

Question 48:

Following Receipts and Payments Account was prepared from the Cash Book of Delhi Charitable Trust for the year ending 31st March, 2019:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ending 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Balance b/d: | By Charity | 1,15,000 | |||

| Cash in Hand | 1,15,000 | By Rent and Taxes | 32,000 | ||

| Cash at Bank | 1,26,000 | By Salary | 60,000 | ||

| To Donations | 90,000 | By Printing | 6,000 | ||

| To Subscriptions | 4,28,000 | By Postage | 3,000 | ||

| To Legacies Donations | 1,80,000 | By Advertisements | 45,000 | ||

| To Interest on Investment | 45,000 | By Insurance | 20,000 | ||

| To Sale of old Newspaper | 2,000 | By Furniture | 2,16,000 | ||

| By Investment | 2,30,000 | ||||

| By Balance c/d: | |||||

| Cash in Hand | 99,000 | ||||

| Cash at Bank | 1,60,000 | ||||

9,86,000 | 9,86,000 | ||||

Prepare Income and Expenditure Account for the year ended 31st March, 2019, and Balance Sheet as on that date after the following adjustments:

(i) Insurance premium was paid for insurance taken w.e.f. 1st July, 2018.

(ii) Interest on investment ₹ 11,000 accrued was not received.

(iii) Rent ₹ 6,000; Salary ₹ 9,000 and advertisement expenses ₹ 10,000 outstanding as on 31st March, 2019.

(iv) Legacy Donation is towards construction of Library Block.

ANSWER:

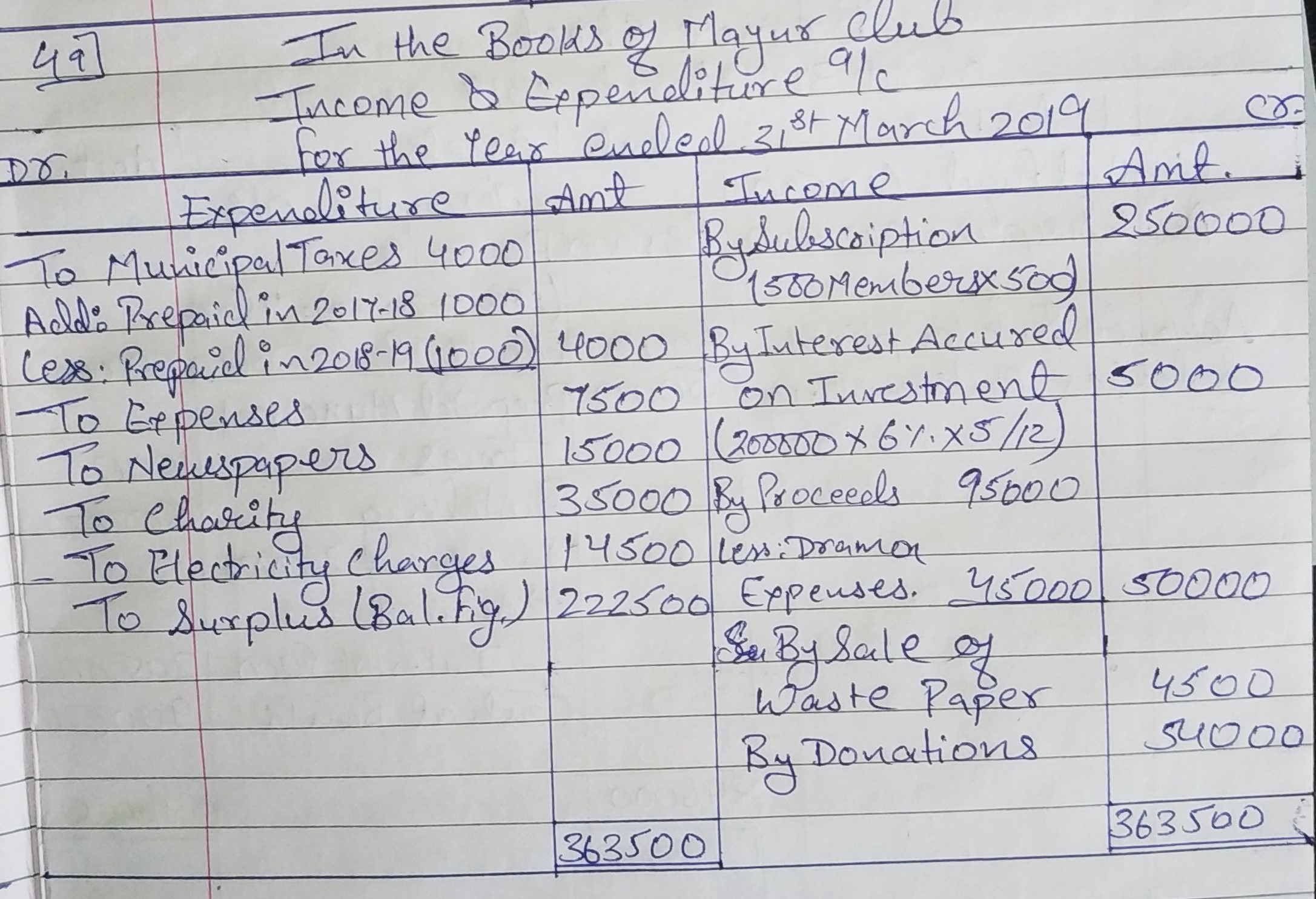

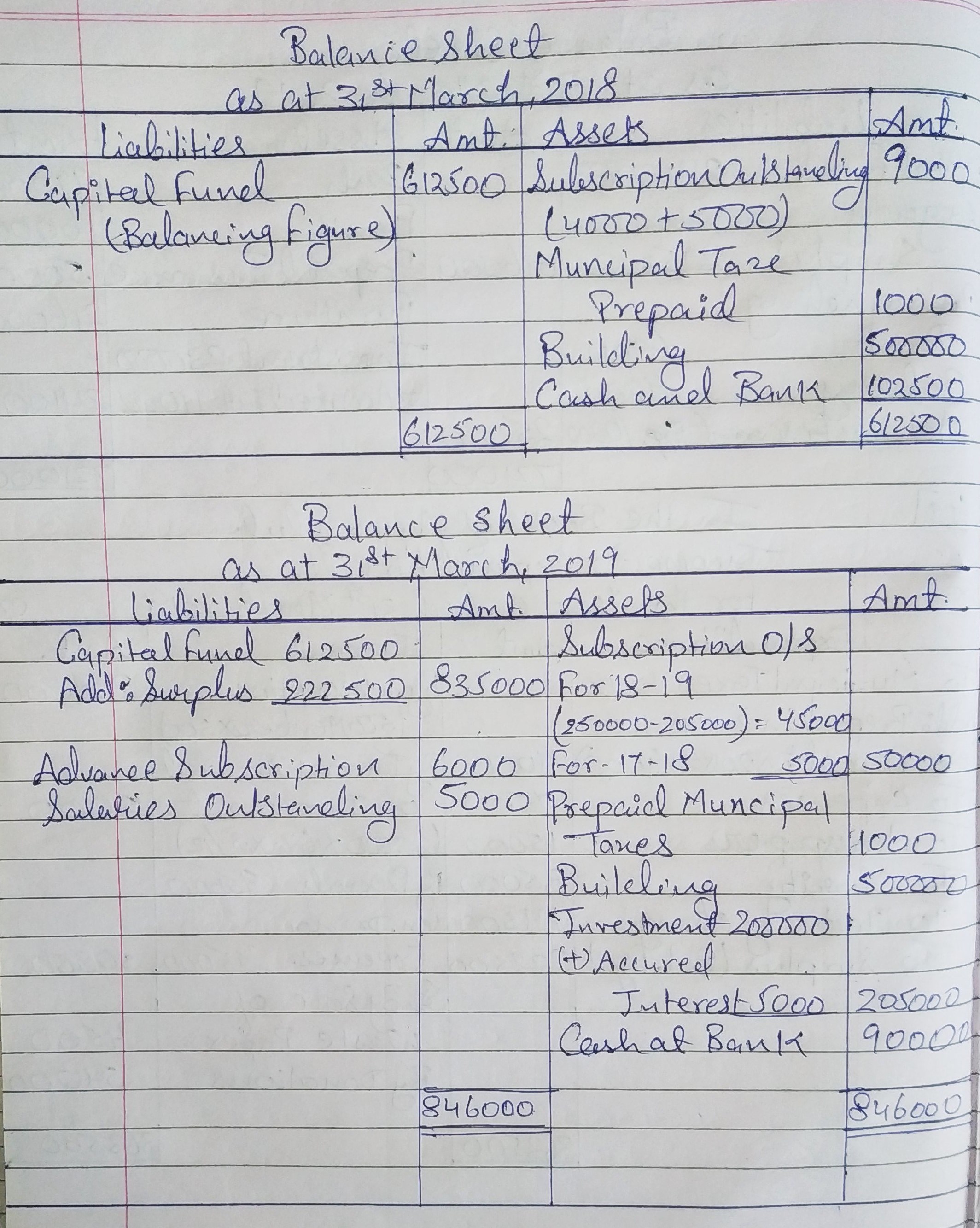

Question 49:

Given Below is the Receipts and Payments Account of a Mayur Club for the year ended 31st March, 2019:

RECEIPTS AND PAYMENTS ACCOUNT | |||||

| Dr. |

|

| Cr. | ||

| Receipts | (₹) | Payments | (₹) | ||

| To Balance b/d | 1,02,500 | By Salaries | 60,000 | ||

| To Subscriptions: |

| By Expenses | 7,500 | ||

2017-18 | 4,000 | By Drama Expenses | 45,000 | ||

2018-19 | 2,05,000 | By Newspapers | 15,000 | ||

2019-20 | 6,000 | 2,15,000 | By Municipal Taxes | 4,000 | |

| To Donations | 54,000 | By Charity | 35,000 | ||

| To Proceeds of Drama Tickets | 95,000 | By Investments | 2,00,000 | ||

| To Sale of Waste Paper | 4,500 | By Electricity Charges | 14,500 | ||

| By Balance c/d | 90,000 | ||||

4,71,000 | 4,71,000 | ||||

Prepare club’s Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date after taking the following information into account:

(i) There are 500 members, each paying an annual subscription of ₹ 500, ₹ 5,000 are still in arrears for the year ended 31st March, 2018.

(ii) Municipal Taxes amounted to ₹ 4,000 per year is paid up to 30th June and ₹ 5,000 are outstanding of salaries.

(iii) Building stands in the books at ₹ 5,00,000.

(iv) 6% interest has accrued on investments for five months.

ANSWER:

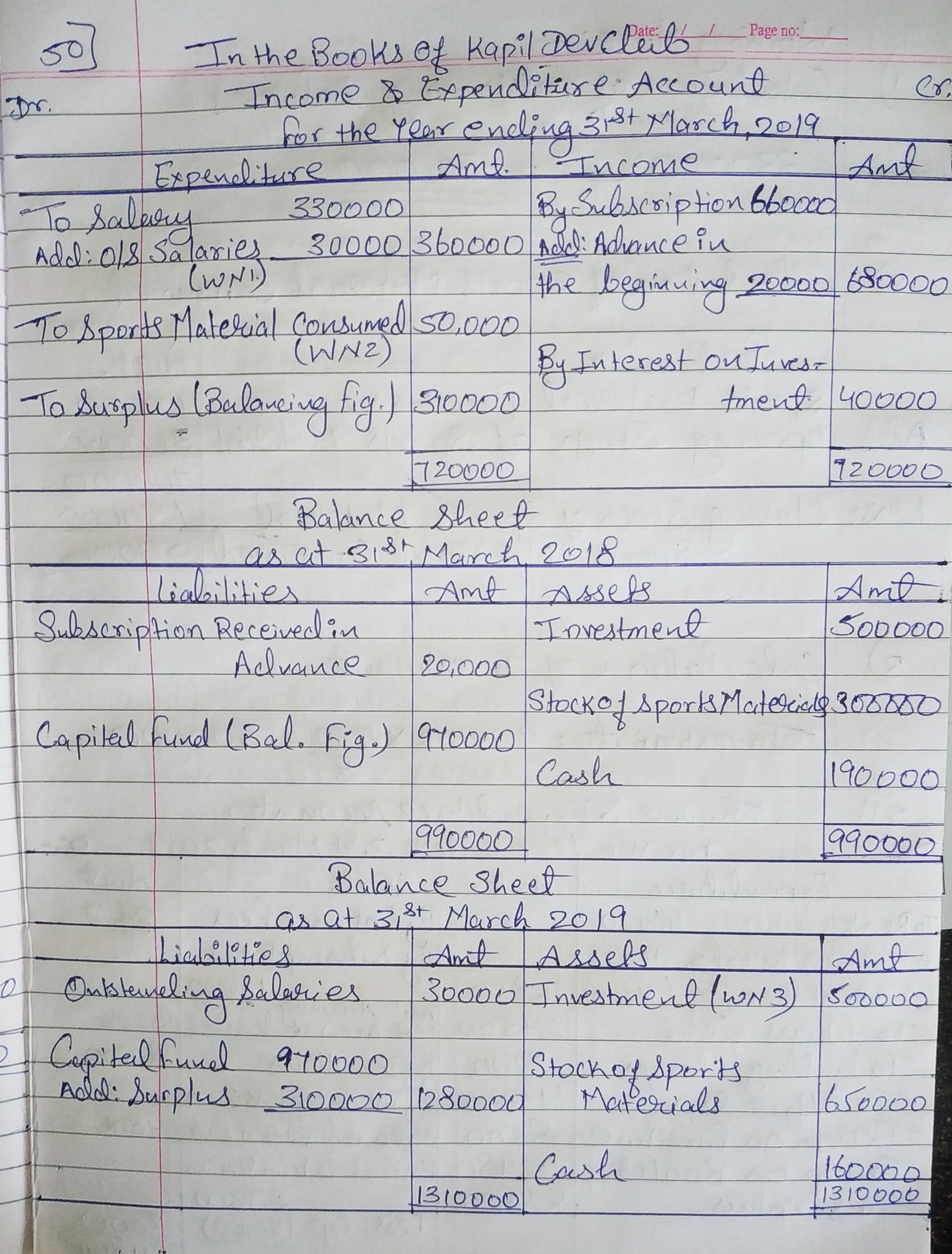

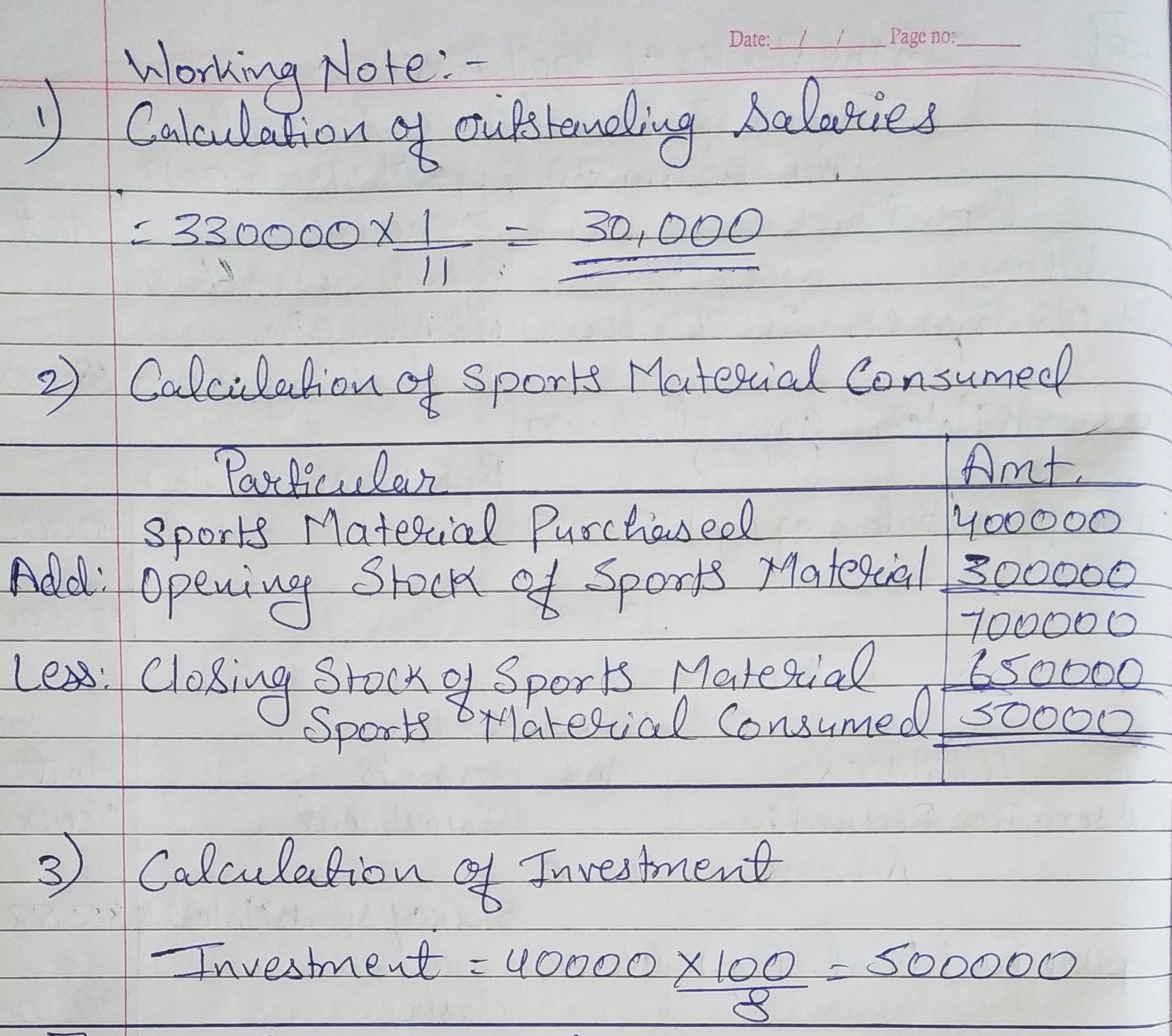

Question 50:

From the following Receipts and Payments Account of Kapil Dev Club and from the given additional information, prepare Income and Expenditure Account for the year ending 31st December, 2019 and the Balance Sheet as at that date:

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Balance b/d | 1,90,000 | By Salaries | 3,30,000 | ||

| To Subscriptions | 6,60,000 | By Sports Material | 4,00,000 | ||

| To Interest on Investment | 40,000 | By Balance c/d | 1,60,000 | ||

| @ 8% p.a. for full year | |||||

8,90,000 | 8,90,000 | ||||

Additional Information:

(i) The club had received ₹ 20,000 for subscription in 2017-18 for 2018-19.

(ii) Salaries had been paid only for 11 months.

(iii) Stock of sports materials on 31st March, 2018 was ₹ 3,00,000 and on 31st March, 2019 ₹ 6,50,000.

ANSWER:

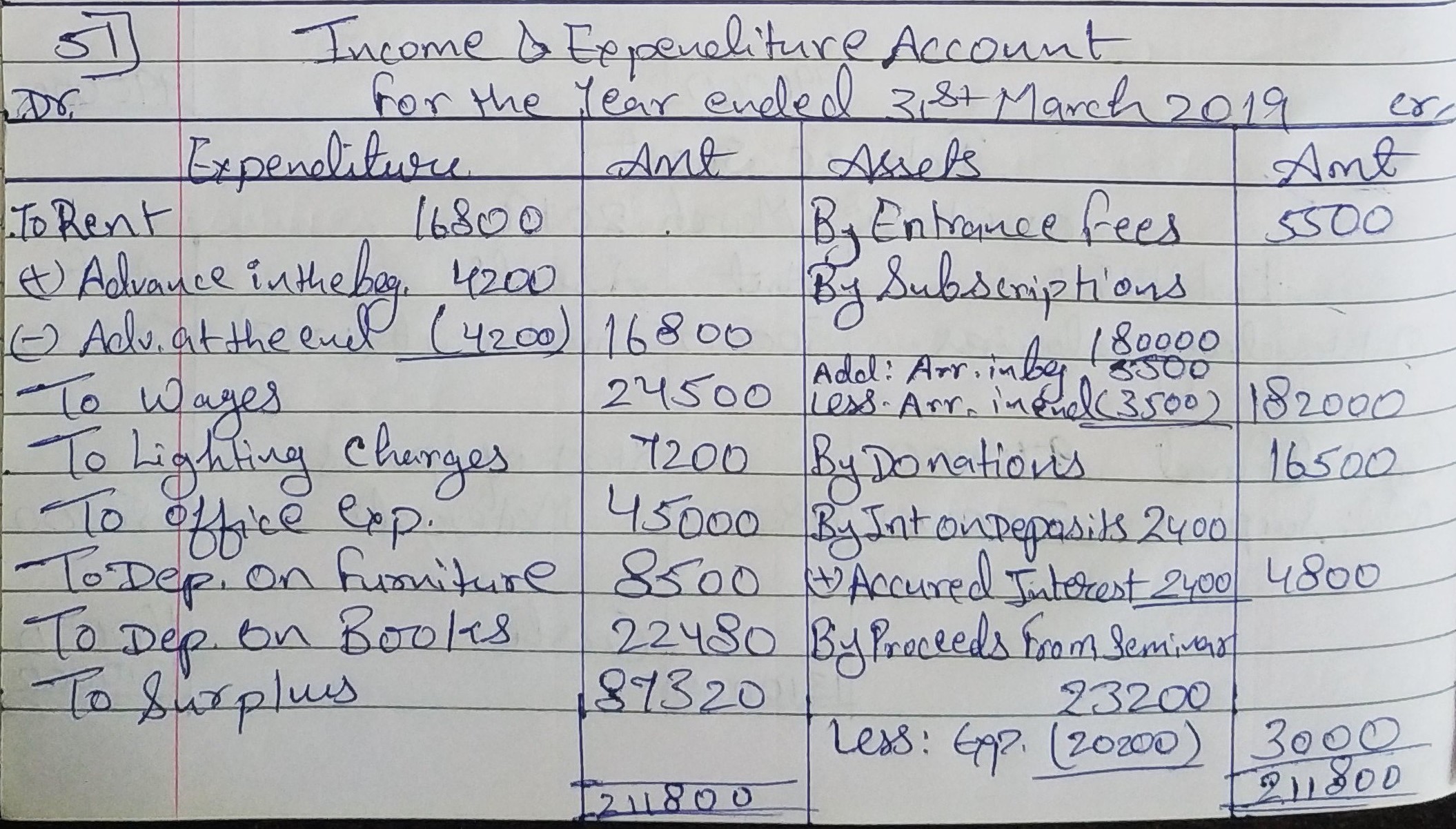

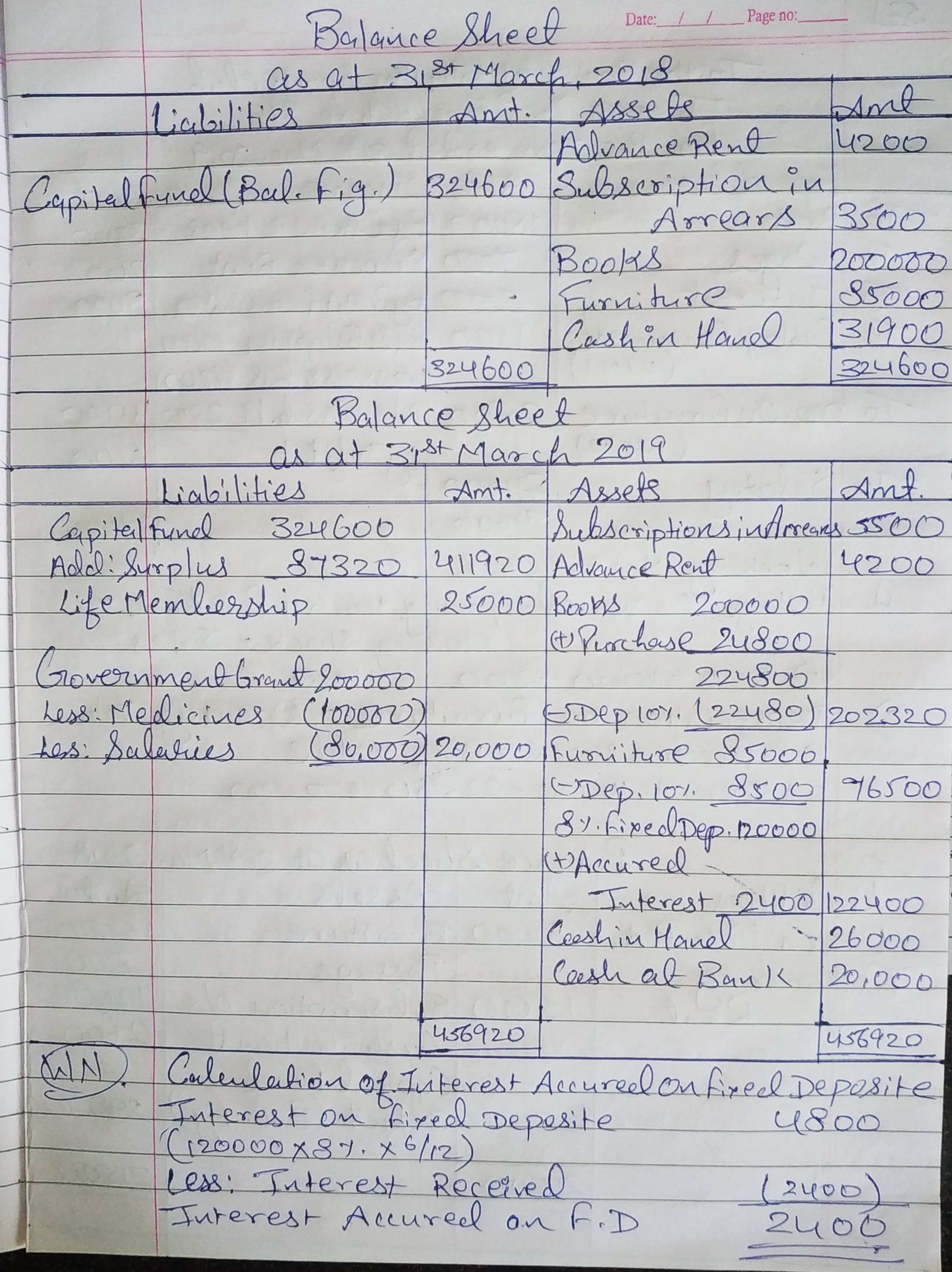

Question 51:

From the following information and Receipts and Payments Account of Delhi Medical Society, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date.

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

Dr. | Cr. | ||||

Receipts | (₹) | Payments | (₹) | ||

To Balance b/d | 31,900 | By Rent | 16,800 | ||

| To Entrance Fees | 5,500 | By Wages | 24,500 | ||

| To Subscriptions | 1,80,000 | By Lighting Charges | 7,200 | ||

| To Donations | 16,500 | By Books | 24,800 | ||

| To Life Membership Fees | 25,000 | By Medicines (Polio Eradication Project) | 1,00,000 | ||

| To Government Grant (Polio Eradication Project) | 2,00,000 | By Salaries to Doctors (Polio Eradication Project) | 80,000 | ||

| To Proceeds of Seminar | 23,200 | By Office Expenses | 45,000 | ||

| To Interest on Deposits | 2,400 | By 8% Fixed Deposits | 1,20,000 | ||

| (On 1st October, 2018) | |||||

| By Seminar Expenses | 20,200 | ||||

| By Cash in Hand | 26,000 | ||||

| By Bank A/c (Polio Eradication Project) | 20,000 | ||||

4,84,500 | 4,84,500 | ||||

Other information:

On 31st March, 2018, the Club possessed books of ₹ 2,00,000 and Furniture of ₹ 85,000. Provide depreciation on these assets @ 10% including the purchases during the year.

Subscriptions in arrears in the beginning of the year amounted to ₹ 3,500 and at the end of the year ₹ 5,500 were outstanding.

The Club paid three months’ rent in advance both in the beginning and at the end of the year.

ANSWER:

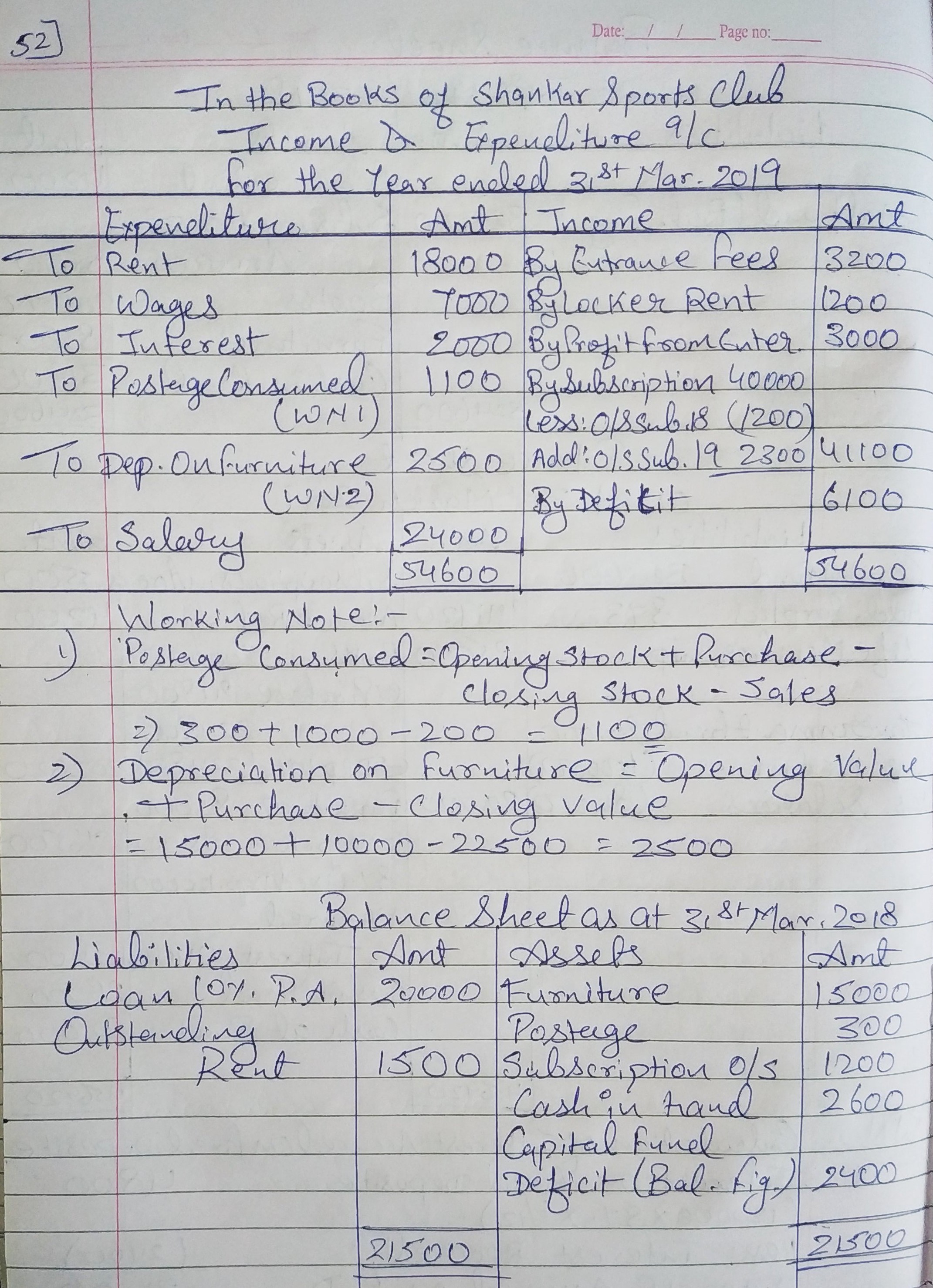

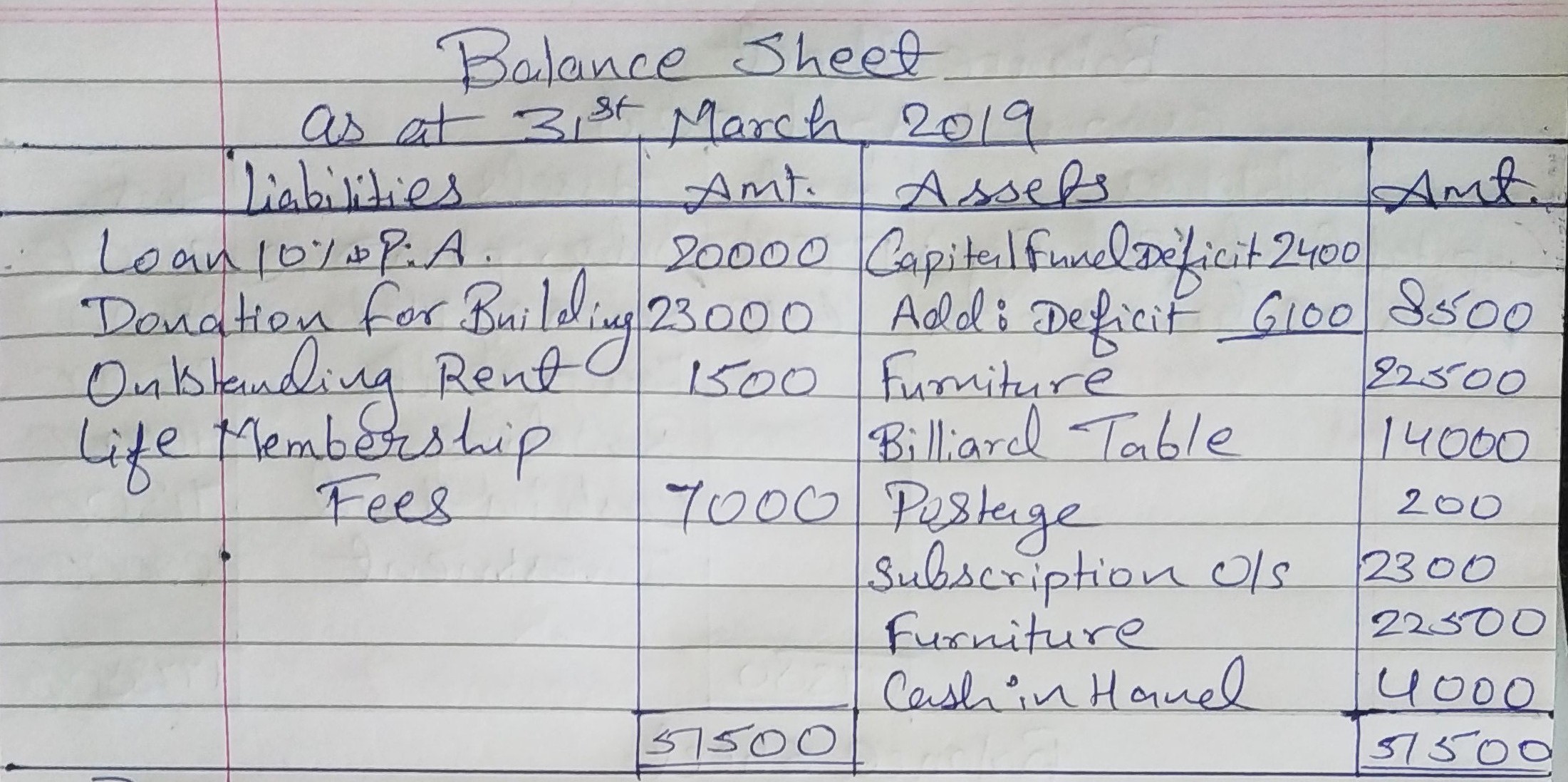

Question 52:

Receipts and Payments Account of Shankar Sports Club is given below for the year ended 31st March, 2019:

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

Dr. | Cr. | ||||

Receipts | (₹) | Payments | (₹) | ||

| To Cash in Hand (Opening) | 2,600 | By Rent | 18,000 | ||

| To Entrance Fee | 3,200 | By Wages | 7,000 | ||

| To Donation for Building | 23,000 | By Billiard Table | 14,000 | ||

| To Locker Rent | 1,200 | By Furniture | 10,000 | ||

| To Life Membership Fee | 7,000 | By Interest | 2,000 | ||

| To Profit from Entertainment | 3,000 | By Postage | 1,000 | ||

| To Subscription | 40,000 | By Salary | 24,000 | ||

| By Cash In Hand (Closing) | 4,000 | ||||

| 80,000 | 80,000 | ||||

Prepare Income and Expenditure Account and Balance Sheet with the help of following information:

Subscription outstanding on 31st March, 2018 is ₹ 1,200 and ₹ 2,300 on 31st March, 2019; opening stock of postage stamps is ₹ 300 and closing stock is ₹ 200; Rent ₹ 1,500 related to the year ended 31st March, 2018 and ₹ 1,500 is still unpaid. On 1st April, 2018 the club owned furniture ₹ 15,000, Furniture valued at ₹ 22,500 on 31st March, 2019. The club has a loan of ₹ 20,000 (@ 10% p.a.) which was taken, in year ended 31st March, 2018.

ANSWER:

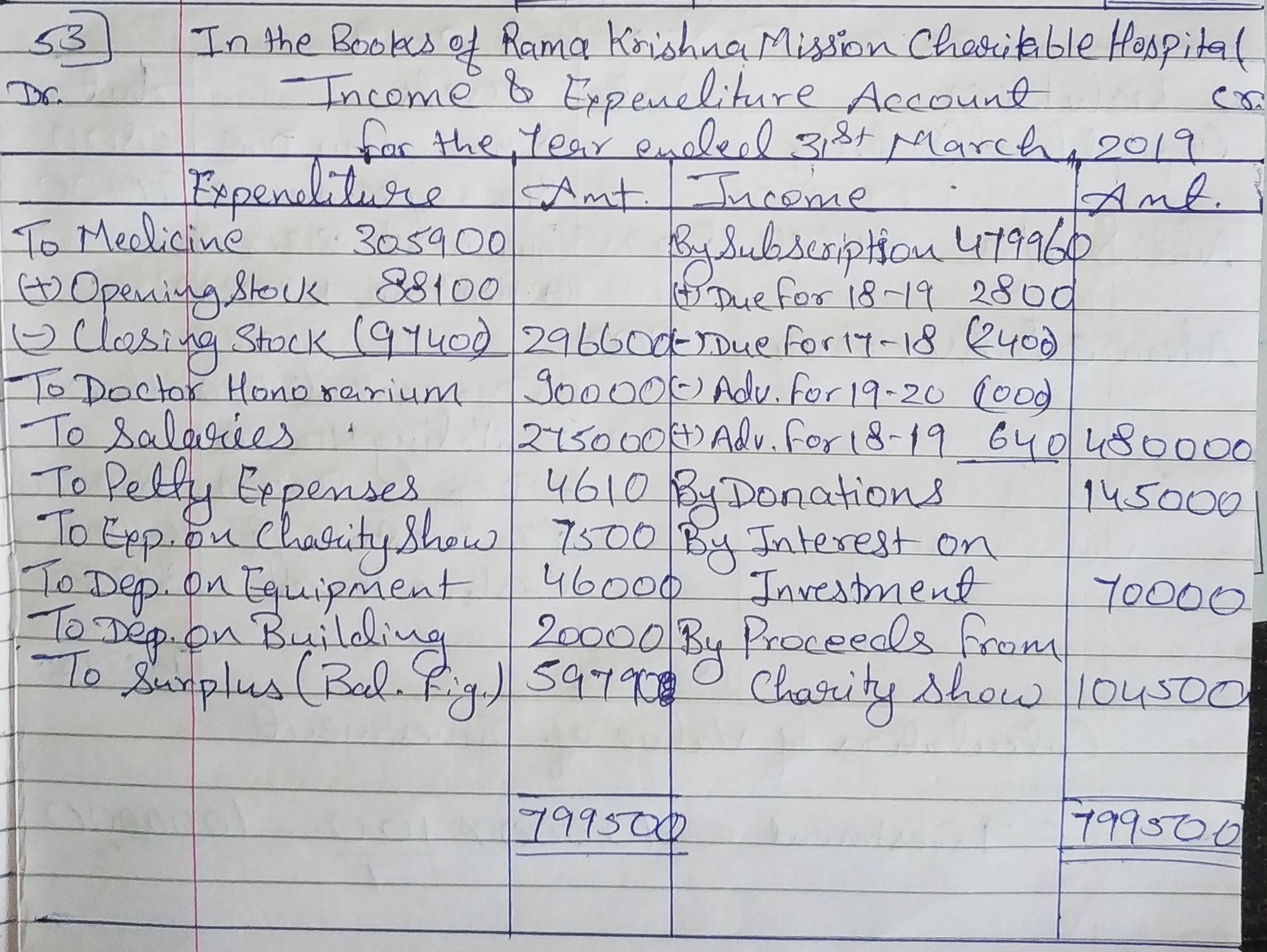

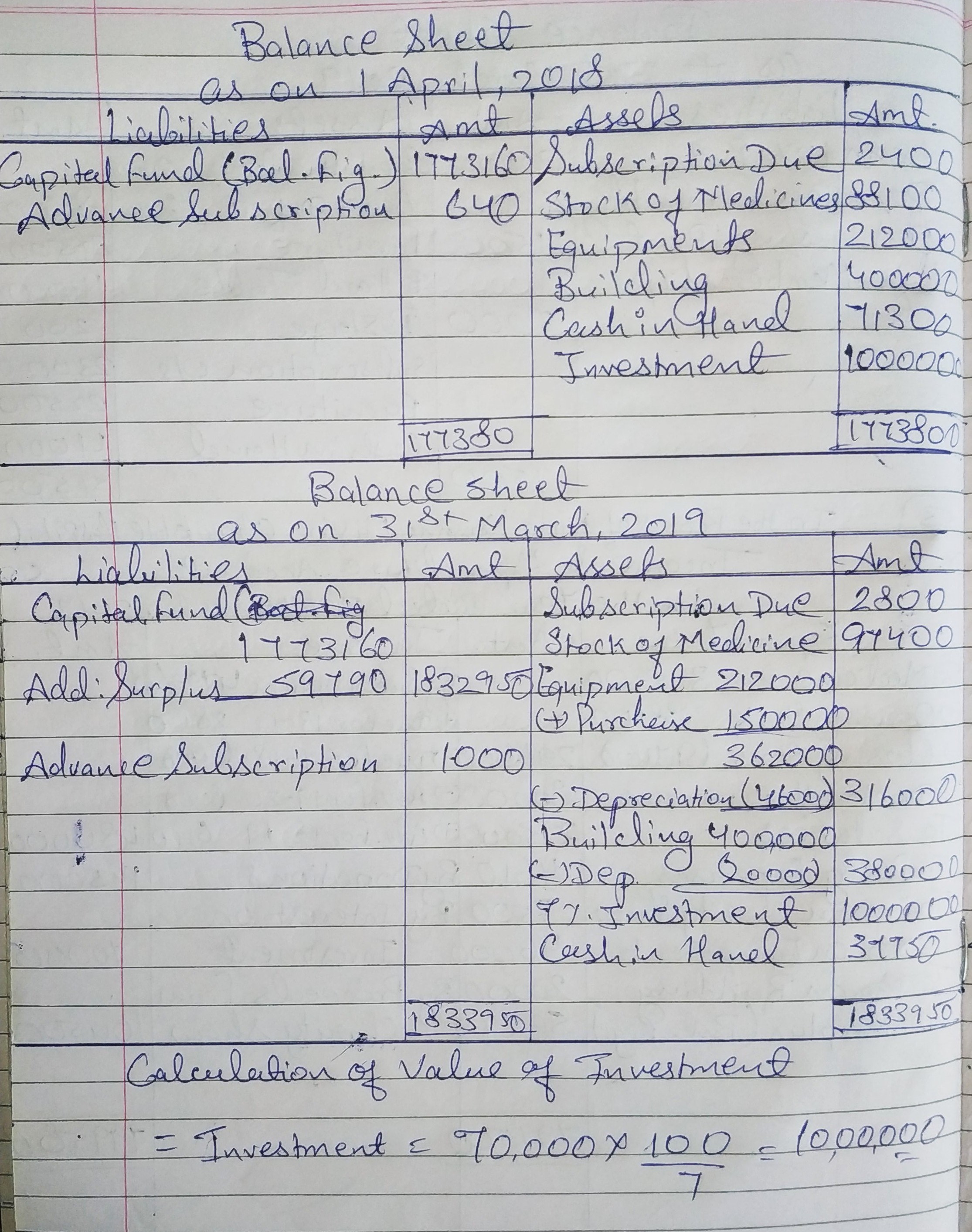

Question 53:

From the following particulars relating to the Ramakrishna Mission Charitable Hospital, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date.

| RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March, 2019 | |||||

| Dr. | Cr. | ||||

| Receipts | ₹ | Payments | ₹ | ||

| To Cash in Hand on 1st April, 2018 | 71,300 | By Medicines | 3,05,900 | ||

| To Subscriptions | 4,79,960 | By Doctor’s Honorarium | 90,000 | ||

| To Donations | 1,45,000 | By Salaries | 2,75,000 | ||

| To Interest on Investment @ @ 7% for full year | 70,000 | By Petty Expenses | 4,610 | ||

| To Proceeds from Charity Show | 1,04,500 | By Equipments | 1,50,000 | ||

| By Expenses on Charity Show | 7,500 | ||||

| By Cash in Hand on 31st March, 2018 | 37,750 | ||||

| 8,70,760 | 8,70,760 | ||||

| Additional Information: | As at 1st April, 2018 (₹) | As at 31st March, 2019 (₹) |

| Subscriptions Due | 2,400 | 2,800 |

| Subscriptions Received in Advance | 640 | 1,000 |

| Stock of Medicines | 88,100 | 97,400 |

| Estimated value of Equipments | 2,12,000 | 3,16,000 |

| Building (cost less depreciation) | 4,00,000 | 3,80,000 |

ANSWER:

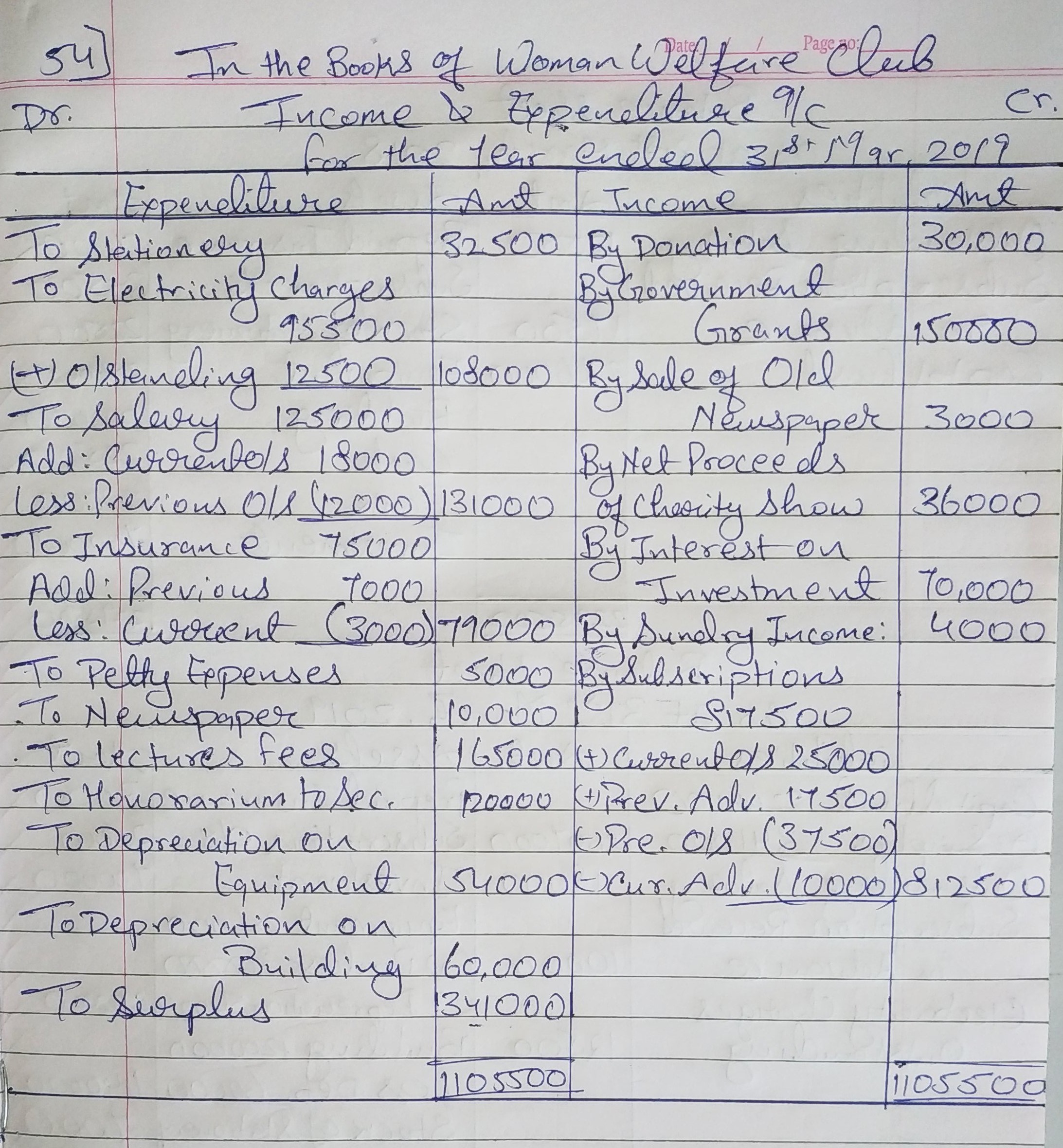

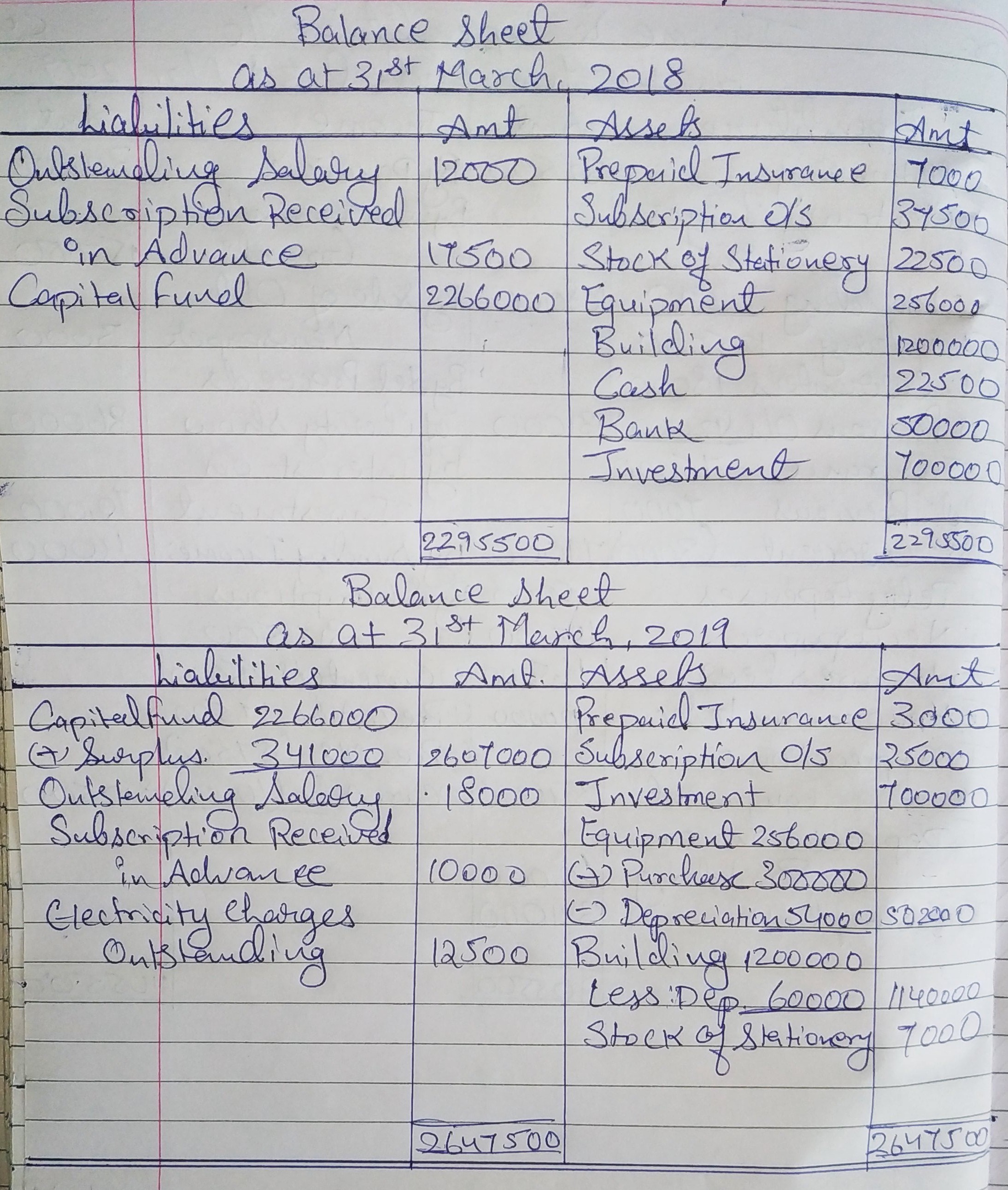

Question 54:

Following is the Receipt and Payment Account of Women’s Welfare Club for the year ended 31st March, 2019:

RECEIPTS AND PAYMENTS ACCOUNT | |||||

Dr. |

| Cr. | |||

| Receipts | ₹ | Payments | ₹ | ||

| To Cash in Hand | 22,500 | Salary | 1,25,000 | ||

| To Cash at Bank | 50,000 | By Stationery | 17,000 | ||

| To Subscriptions | 8,17,500 | By Electric Charges | 95,500 | ||

| To Donations | 30,000 | By Insurance | 75,000 | ||

| To Government Grant | 1,50,000 | By Equipments | 3,00,000 | ||

| To Sale of Newspapers | 3,000 | By Petty Expenses | 5,000 | ||

| To Proceeds of Charity Show | 1,65,000 | By Expenses on Charity Show | 1,29,000 | ||

| To Interest on Investments @ 10% for full year | 70,000 | By Newspapers | 10,000 | ||

| To Sundries Income | 4,000 | By Lectures Fee | 1,65,000 | ||

| By Honorarium to secretary | 1,20,000 | ||||

| By Cash in Hand | 20,500 | ||||

| By Cash at Bank | 2,50,000 | ||||

|

|

| |||

| 13,12,000 |

| 13,12,000 | ||

|

|

|

| ||

Particulars | 1st April, 2018 (₹) | 31st March, 2019 (₹) |

| Outstanding Salaries | 12,000 | 18,000 |

| Insurance Prepaid | 7,000 | 3,000 |

| Subscription Outstanding | 37,500 | 25,000 |

| Subscription received in advance | 17,500 | 10,000 |

| Electricity Charges outstanding | … | 12,500 |

| Stock of Stationery | 22,500 | 7,000 |

| Equipments | 2,56,000 | 5,02,000 |

| Building | 12,00,000 | 11,40,000 |

Prepare Income and Expenditure Account for the year ended 31st March, 2019,and Balance Sheet as on that date.

ANSWER: