MEANING AND CONCEPT OF NOT-FOR-PROFIT ORGANISATION

Enterprises (Business organisations) are profit-earning entities since their main objective is to earn profit. In contrast to these entities, there are also Not-for-Profit Organisations whose main objective is to serve the society and its members and not to earn profit.

Not-for-Profit Organisations, also known as Non-profit Organisations are set up with the objective to further cultural, educational, health, religious, public services to public and/or members, etc. not with the purpose of earning profit.

Examples of such organisations are: schools, colleges, public hospitals, literary societies, societies for promotion of sports, arts and culture, social welfare organisations, clubs, etc.

Funds required for the activities of a Not-for-Profit Organisation are normally sourced (contributed) by its members, trustees, etc., as donations, membership fees and subscriptions. Funds received by a Not-for-Profit Organisation may be:

(a) Donation,

(b) Membership Fee or Entrance Fee,

(c) Subscription,

(d) Loans, and

(e) Grants (From Government and/or Institutions).

CHARACTERISTICS OR FEATURES OF NOT-FOR-PROFIT ORGANISATION

- Entity: Not-for-Profit Organisation is a legal entity separate from its promoters.

- Purpose: Their purpose is to further cultural, educational, religious, professional objectives and rendering service to people at large.

- Ownership: It is set-up by individuals or companies as charitable society or trust but it is not owned by them. It belongs to the society.

- Profit is not the Objective: Not-for-Profit Organisation does not function with the objective of earning profit. But, it does not mean that it cannot earn profit, termed as Surplus. Surplus is necessary to maintain its assets and also operations. Surplus is used for the objectives for which it is set-up and is not distributed among its members.

- Management: Not-for-Profit Organisation is managed by a group of individuals often called Trustees or Managing Committee.

- Funds: Funds for it’ operations are given by its members and donors in the form of Entrance Fee, Membership Fee, Subscription and Donations. It is supplemented by surplus from operations.

- Financial Statements: It prepares its financial statements every year and includes Receipts and Payments Account, Income and Expenditure Account and the Balance Sheet.

Difference between Not-for-Profit Organisation and Profit Earning Organisation

| Basis | Not-for-Profit Organisation | Profit Earning Organisation (Business Firm) |

|---|---|---|

| Purpose for which set-up | It is set-up with a purpose to further cultural, educational, religious, professional or public service. | Purpose is to earn profit. |

| Sources of Funds | They are raised by way of Membership Fee, Subscription, Donations and Surplus from Operations. In the Balance Sheet, it is shown as General Fund or Capital Fund or Corpus Fund. | They are raised as capital by the proprietor, partners (in the case of Partnership Firms) and Share Capital or borrowed funds (in the case of Companies). Profits not distributed to partners and shareholders are shown as Reserves. |

| Financial Statements | Financial Statements prepared are Receipts and Payments Account, Income and Expenditure Account and Balance Sheet. | Financial Statements prepared are Trading Account, Profit and Loss Account and Balance Sheet. |

| Surplus/Profit | Balance of the Income and Expenditure Account is either Surplus or Deficit. | Financial Statements prepared are Trading Account, Profit and Loss Account and Balance Sheet. |

| Distribution of Surplus/Profit | Its profit is not distributed among its members. | Its profit is distributed among its members. |

Financial Statements of Not-for-Profit Organisation

Not-for-Profit Organisation prepares annual or final accounts showing the financial transactions of the organisation for its members and to comply with statutory requirements.

Financial Statements or Final accounts of a Not-for-Profit Organisation include:

Receipts and Payments Account,

Income and Expenditure Account, and

Balance Sheet.

1. RECEIPTS AND PAYMENTS ACCOUNT

Receipts and Payments Account is a summary of cash (including bank) receipts and payments during an accounting period, receipts and payments being shown under appropriate heads of accounts.

It begins with Opening Cash and Bank Balances and ends with Closing Cash and Bank Balances of the accounting period.

Receipts are shown in the debit side whereas payments are shown in the credit side of the account.

Receipts and Payments of every nature are shown in this account, i.e., whether it is capital or revenue in nature or whether it relates to the current year, previous year or next year.

Format of Receipts and Payments Account

Features or Characteristics of Receipts and Payments Account

- Nature: It is an Asset Account (Real Account as per Traditional Approach), it being a summary of cash receipts and cash payments including bank balance.

- Basis of Preparing: It is prepared on Cash Basis of Accounting, i.e., transactions which have been received or paid in cash are shown in the account. In the debit side amounts received are shown and in the credit side amounts paid are shown.

- Capital and Revenue Receipts and Payments: It shows all receipts and payments whether they are of revenue nature or capital nature.

- Period: It shows all cash and bank transactions whether it relates to current, previous or succeeding (next) accounting periods.

- Opening and Closing Balances: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

- Adjustments: Adjustment for outstanding expenses, prepaid expenses, accrued income or income received in advance, and depreciation are not made in this account as it is maintained on cash basis of accounting.

- Purpose: The purpose is to show amount received and paid under different heads during the accounting year.

Limitations of Receipts and Payments Account

(i) It does not differentiate between capital and revenue incomes and expenses as both are shown in Receipts and Payments Account.

(ii) It does not show the incomes and expenses that have been earned during the year but are not received.

(iii) It does not show surplus or deficit for the accounting period.

(iv) It does not show whether the Not-for-Profit Organisation is able to meet its day-to-day expenses out of its income or not.

Difference between Receipts and Payments Account and Cash Book

| Basis | Receipts and Payments Account | Cash Book |

|---|---|---|

| Basis | It is a summary of Cash Book and is prepared from the Cash Book. | It records each transaction of receipt and payment separately. |

| Period | Receipts and Payments Account is a summary prepared at the end of accounting year. | Cash Book is maintained on daily basis, i.e., transactions are recorded date wise in the Cash Book. |

| Institutions | It is prepared by the Not-for-Profit Organisation. | It is prepared by all organisations be it Not-for-Profit Organisation or an enterprise. |

| Sides | Under it, there are receipts and payments sides instead of debit and credit sides. | Cash Book is divided into debit and credit sides. |

| Ledger Folio | There is no column for Ledger Folio. | Cash Book has a separate column for Ledger Folio. |

2. INCOME AND EXPENDITURE ACCOUNT

Not-for-Profit Organisations do not prepare Profit and Loss Account as they are not set up with a purpose to earn profit. Instead, they prepare Income and Expenditure Account at the end of the accounting period to determine surplus or deficit.

Incomes and gains are transferred to the credit of this account while expenses and losses are transferred to the debit. Difference between the two sides is either surplus (If total of credit side is more than the total of debit side) or deficit (If total of debit side is more than the total of credit side). Surplus is added to the Capital Fund, whereas, Deficit is deducted from Capital Fund in the Balance Sheet.

Income and Expenditure Account is prepared at the end of the accounting period matching Revenue Receipts (income) with Revenue Expenses to determine surplus or deficit.

Revenue Expenses to determine surplus or deficit.

It is prepared following the accrual basis of accounting, therefore:

- Revenue Expenses for the accounting period are taken, whether paid or not.

- Revenue Incomes for the accounting period are taken, whether received or not.

- Non-Cash Expenses such as Depreciation are accounted.

- Capital Expenditure, e.g., purchase of Land, are not considered because they are shown in the Balance Sheet.

- Capital Incomes or Receipts, e.g., donation for specific purpose are not considered.

IMPORTANT NOTE

Income and Expenditure Account does not have an opening balance. Closing balance is either surplus or deficit, which is transferred to Capital Fund in the Balance Sheet.

Revenue items of the current accounting period only are considered and incomes and expenditures relating to the preceding or succeeding (next) accounting periods are excluded while preparing the Income and Expenditure Account.

- Capital Expenditure: Capital expenditure is an expenditure the benefit of which is of enduring nature, i.e., its benefit extends beyond one accounting period. For example, purchase of asset (say, land and building) for the furtherance of organisation’s activities is a capital expenditure.

- Revenue Expenditure: Revenue expenditure is that expenditure the benefit of which expires within the accounting period. In the context of Not-for-Profit Organisations, revenue expenditure means expenditure incurred for social or charitable activities for which it is set up but excluding the capital expenditure. Examples: Salaries to staff, rent, educational grants, honorariums paid, sports material used, insurance, etc.

- Capital Receipts: Capital Receipts are the receipts which are not revenue receipts or are receipts for the purpose specified by the donor. Examples: Life Membership Fee, Corpus Donations, Donation towards Building Fund, Receipts from sale of Fixed Assets, etc.

- Revenue Receipts: Revenue receipts are the receipts which are received as an income by the organisation. Examples: Entrance Fee, Subscription for the year from members, General Donations, Rent Received, Sale of Old Newspapers, etc.

Features of Income and Expenditure Account

- Nature: It is a Nominal Account. Hence, expenses and losses for the year are transferred to the debit while incomes and gains for the year are transferred to the credit of Income and Expenditure Account.

- Basis of Accounting: Incomes, expenses and losses of revenue nature are shown in the account on accrual basis of accounting.

According to Accrual Basis of Accounting, revenue and expenses are recorded in the period in which they become due, rather than when they are received or paid.

- Accounting Period: Those incomes, expenses and losses which relate to the current accounting period, whether paid or not are shown in the account.

- Opening and Closing Balances: It does not have an opening balance. Its balance at the end is either surplus or deficit which is transferred to Capital Fund in the Balance Sheet.

- Adjustments: This account is prepared on accrual basis of accounting and thus all adjustments relating to prepaid or outstanding expenses and incomes, provision for depreciation or doubtful debts are made.

Format of Income and Expenditure Account

*Either of the two will appear.

Difference between Income and Expenditure Account and Profit and Loss Account

| Basis | Income and Expenditure Account | Profit and Loss Account |

|---|---|---|

| Object | Object of income and Expenditure Account is to determine surplus, i.e., excess of income over expenditure or deficit, i.e., excess of expenditure over income. | Object of Profit and Loss Account is to determine net profit earned or net loss incurred. |

| Prepared by | It is prepared by Not-for-Profit Organisations. | It is prepared by business enterprises. |

| Method | It is prepared from the Trial Balance, where complete set of books of account are maintained or from the Receipts and Payments Account and other information, where complete set of books of account are not maintained. | It is prepared from the Trial Balance and other information. |

| Balance | The balance in the account is termed as surplus or deficit. | The balance in the account is termed as net profit or net loss. |

3. BALANCE SHEET

Balance Sheet shows the financial position of an organisation as at a particular date.

The method and basis of preparing the Balance Sheet of a Not-for-Profit Organisation is same as that is of an enterprise (business firm).

It is prepared after having prepared the Income and Expenditure Account.

Surplus or deficit of the Income and Expenditure Account is transferred to the Capital Fund.

The Balance Sheet shows assets, liabilities and capital fund.

Capital Fund is also known as General Fund, Corpus Fund and Accumulated Fund.

Where Opening Balance of Capital Fund is not given, it is determined by preparing Opening Balance Sheet.

Opening Capital Fund is excess of assets over liabilities in the beginning of the period.

Capital Fund = Total Assets — Total Liabilities.While preparing the Balance Sheet, following points should be kept in mind:

- Determination of Value of Fixed Assets: Fixed Assets as existing in the previous year’s Balance Sheet should be adjusted for sale during the year, purchase during the year and depreciation. The adjusted amount is shown in the Balance Sheet. It should be noted that if during the year a part of the asset has been sold then the book value of the asset sold is deducted from that Asset Account and the difference between the sale proceeds and the book value is shown as gain (profit) or loss in the Income and Expenditure Account. For example, opening balance in Furniture Account is 1,00,000. Furniture having book value of 20,000 is sold for 25,000. 20,000 will be deducted from 1,00,000 and 5,000 (gain, i.e., profit on sale) will be shown as income in the credit side of Income and Expenditure Account. If the furniture is sold for 15,000; 5,000 (Loss on Sale) will be shown as loss in the debit side of Income and Expenditure Account. If a new asset is purchased, the payment would have been shown in the Payments Side of the Receipts and Payments Account. This account, therefore, should be scrutinised, i.e., observed and payments for assets therein will be shown in the assets side of the Balance Sheet.

- Loan: Loan taken, if any, is shown in the Receipts Side of the Receipts and Payments Account and the amount, less any, repayments (which will be in the Payments Side), is shown in the liabilities side of the Balance Sheet.

- Advance: Advance given, if any, is shown in the Payments Side and recovery of advance on the Receipts Side. Net amount is shown in the assets side of the Balance Sheet.

- Investment: Investment made is shown in the Payments Side of Receipts and Payments Account and Investments realised in the Receipts Side. They are shown in the assets side of the Balance Sheet. Any addition is added and sale of Investment is deducted.

- Adjustment Related to Expenses and Income: Adjustments made in expenses and incomes before they are shown in the Income and Expenditure Account are also shown in the Balance Sheet.

(a) Outstanding Expenses are shown as a liability;

(b) Prepaid Expenses are shown as an asset;

(c) Unearned Income or Income Received in Advance are shown as a Liability; and

(d) Accrued Incomes are shown as an asset.

- Liabilities: Liabilities as existing in the previous year’s Balance Sheet should be adjusted for payment made against them. This information will be available in the Payments. Side of the Receipts and Payments Account. Net amount is shown in the Balance Sheet.

Receipts for specific purpose say donations for building or Annual Dinner, etc., are not shown in Income and Expenditure Account but are shown in the liabilities side of the Balance Sheet.

- Cash and Bank Balance: Cash and Bank Balance at the end of the year in the Receipts and Payments Account is shown in the Assets Side of the Balance Sheet. Bank Overdraft is shown in the liabilities side of the Balance Sheet.

- Surplus or Deficit: Surplus or deficit as determined from the Income and Expenditure Account is transferred to the Capital Fund.

Format of Balance Sheet of a Not-for-Profit Organisation

*Building Fund and Sports Fund are examples of Specific Funds.

FUND BASED ACCOUNTING

Fund means amount received or set aside by a Not-for-Profit Organisation to be used for the specific purpose.

Fund amount along with the income earned on the fund cannot be used for purposes other than those for which it is received or set aside.

Donations received or funds set aside for specific purposes are credited to a separate Fund Account and are shown in the liabilities side of the Balance Sheet.

Incomes from these funds are credited to the respective Fund Account and expenses or payments out of these funds are debited.

Accounting when done on this basis is known as Fund Based Accounting.

Not-for-Profit Organisation normally maintains a separate Bank Account for each fund, donations received towards that fund are deposited in the respective Bank Account of the Fund along with the income (e.g., interest). Expenses are paid out of the Bank Account of the Fund.

In the Balance Sheet, each Fund (Say Building Fund, Library Fund, Sports Fund, etc.) are shown separately.

Further receipts and/or surplus set aside towards the fund and income from investment of fund amount is added to the opening balance of the fund.

Payments or expenses are deducted (if the fund does not bring an asset into existence, or;

transferred to Capital Fund (if the fund brings an asset into existence).

A fund normally has a credit balance, which is shown in the liabilities side of the Balance Sheet.

It is the balance that is yet to be used for the purpose for which the fund is established.

Accounting Treatment of Debit Balance in Fund Account when an Asset does not come into Existence.

Fund that does not bring an asset into existence and has a debit balance (i.e., expense is more than the fund balance), it is transferred to the debit of Income and Expenditure Account.

Accounting Treatment of Fund when an Asset is Created

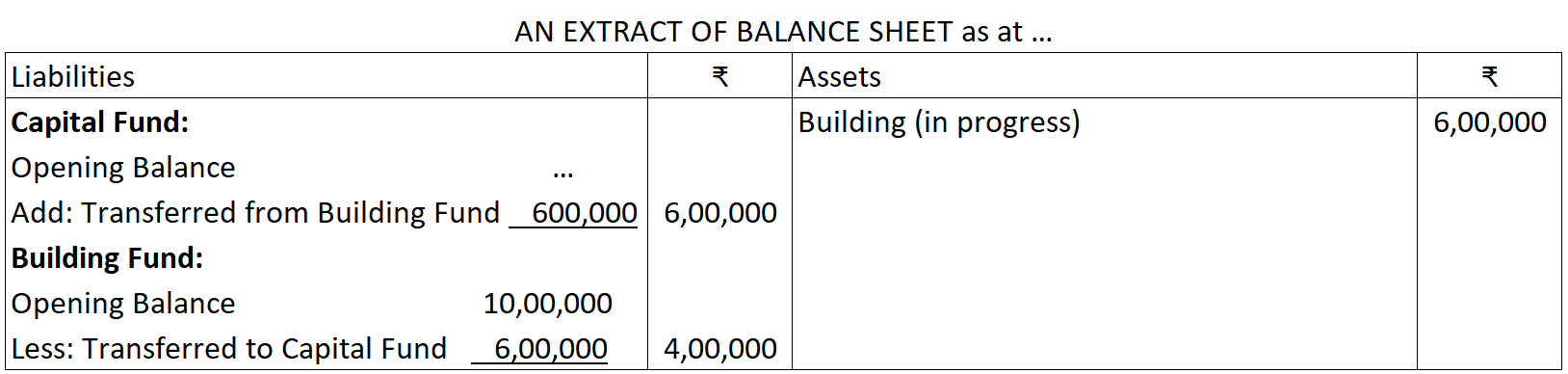

If an asset is created out of Specific Fund (say Building Fund), amount incurred on the asset (say Building) is transferred to Capital Fund.

As a result, asset created out of Specific Fund is shown in the Assets side of the Balance Sheet and the amount is included in Capital Fund.

For example, a Not-for-Profit Organisation has a balance in Building Fund of ₹ 10,00,000. It is constructing a Building and has spent ₹ 6,00,000 during the year. In the Balance Sheet, it will be shown as follows:

ALWAYS REMEMBER

In case the amount of fund (other than funds for assets) is less than the expenses, the balance of expenses not covered by the fund is debited to the Income and Expenditure Account.

Categories of Funds: In the case of Not-for-Profit Organisations, funds may be classified under following two heads:

Unrestricted Fund

Restricted Fund

(i) Unrestricted Fund: Unrestricted Fund means the fund use of which is not restricted. Stating differently, management can use the amount in the fund as is considered appropriate, but for the purpose for which the organisation exists. This fund is known as the General Fund or Capital Fund to which the surplus for the year is added and in case of deficit, deducted.

CAPITAL FUND OR GENERAL FUND OR CORPUS FUND OR ACCUMULATED FUND

It is the sum total of contributions by different parties as corpus donations for commencement and expansion of the Not-for-Profit Organisation. It may increase with further corpus donations or by transfer of Surplus from Income and Expenditure Account. Deficit in Income and Expenditure Account will decrease it.

(ii) Restricted Fund: Restricted Fund is the fund, the use of which is restricted either by the management or by the donor for a specific purpose. Examples of such funds are: Government Grant for a specific purpose, Endowment Fund, Annuity Fund, Loan Fund, Prize Fund, Sports Fund, etc.

(a) Government Grant for a specific purpose: Grant received from Government for specific purpose is restricted to be used for the purpose it is granted. It is accounted in the books following Fund Based Accounting. For example, Grant received from Government for Polio Eradication Programme’ is credited to ‘Polio Eradication Fund’ and income (interest) earned relating to the fund is credited to the fund while related expenses are debited.

(b) Endowment Fund: “It is a fund usually of a non-profit institution, arising from bequest or gift, the income of which is devoted to a specified purpose.—Kohler

Endowment Fund, thus, is a donation with a condition by the donor to use only the income earned from the investment of such funds for the specified purpose so that the original donated amount remains intact.

(c) Annuity Fund: An annuity fund is established when a Not-for-Profit Organisation receives assets from a donor with a condition to pay specified amount periodically to designated beneficiary or beneficiaries. Annuity is a fixed annual (normally) payment and usually, continue only during the lifetime of the named beneficiary or for the period specified by the donor. Annuity Fund Donation, thereafter, becomes the property of the organisation.

(d) Loan Fund: Loan Fund is set-up to grant loans for specific purposes say loan to pursue higher studies.

(e) Fixed Assets Fund: Fixed Assets Fund is a fund earmarked for investment in fixed assets or already invested in fixed assets. Example of Fixed Assets Fund is ‘Building Fund’. Amount invested in fixed assets during the year is transferred to Capital Fund.

(f) Prize Fund: Prize Fund is a fund set-up to use for distribution as prizes say for achievements or contribution to the welfare of the society.

Accounting Treatment of Important Items of Income and Expenditure Account

1. Entrance Fee/Admission Fee

Entrance Fee or Admission Fee is the amount paid by a person at the time of becoming a member of the Not-for-Profit Organisation. Entrance Fee or Admission Fee is a revenue receipt and therefore, is accounted as an income and credited to Income and Expenditure Account.

2. Life Membership Fee

Life Membership Fee is accounted as a Capital Receipt and added to Capital Fund in the liabilities side of the Balance Sheet. It is not accounted as income because a life member pays membership fee once and avails services all through his life.

3. Special Receipts

Special Receipts means receipts of amount for special occasions. For example, contributions received for annual dinner. Such contributions are credited to separate account (Annual Dinner Account in this case) and expenses against these receipts are debited to it. The balance after the event is held is transferred to the Income and Expenditure Account.

4. Donations

A charitable institution often receives donations. Donation received may be a general donation or a specific donation.

(i) General Donation: General Donation is the donation in which the donor does not specify the purpose for which it is to be used.

The amount of general donation is accounted as an income and credited to Income and Expenditure Account.

(ii) Specific Donation: In case the donor specifies the purpose for which the donation can be used, it is a Specific Donation. For example, a donor donates for a library. It means the donation received can be used only for library, i.e., it is a specific donation.

Specific donation is capitalised and is shown in the liabilities side of the Balance Sheet.

IMPORTANT NOTE

Entrance/admission fees and general donations are revenue receipts. Hence, they are shown in the credit side of the Income and Expenditure Account.

5. Legacy

Legacy is the amount received as donation by a Not-for-Profit Organisation under WILL of a deceased person.

The donor may or may not specify conditions for its use.

In case, no condition is specified, it is accounted as ‘General Donation’.

And if a condition is specified, it is accounted as ‘Specific Donation’.

It is accounted for in the books of account as follows:

(i) General Donation: It is accounted as revenue receipt and thus, is credited to Income and Expenditure Account.

(ii) Specific Donation: It is accounted as capital receipt and is credited to a specific ‘Fund Account’ maintained for the purpose (e.g. Prize Fund). It is shown in the liabilities side of the Balance Sheet. It being a fund, principles of Fund Based Accounting are applied, i.e., income relating to such fund is credited to the fund while expenses are debited.

6. Grant

Grant (including Government Grant) received for a specific purpose is a capital receipt and is shown in the Balance Sheet. If the grant is not for a specific purpose, it is a revenue receipt and is credited to Income and Expenditure Account.

7. Sale of Used Sports Materials

Stock of Sports Material is shown in the assets side of the Balance Sheet. Sports material consumed during the year is debited to Income and Expenditure Account and balance amount is carried forward in the Balance Sheet.

In case, old sports material that was debited to Income and Expenditure Account is sold, the sale proceeds are credited to Income and Expenditure Account, i.e., is shown as income.

In case, old sports material appears in the Balance Sheet and is sold, gain (profit) if any on sale of old sports material (Sale Proceeds — Book Value) is credited to Income and Expenditure Account, i.e., is shown as income.

If the sale of old sports material results in a loss (Book Value — Sale Proceeds), it is debited to Income and Expenditure Account.

8. Sale of Old Assets

Sale of an asset may result in gain (profit), if sale value is more than the book value; or

loss, if sale value is less than the book value; or

neither profit nor loss, if sale value is equal to the book value.

Book Value of an asset as on the date of sale is determined after charging depreciation up to the date of sale.

Sale Value is credited to the Asset Account while gain (profit), if any, is credited or loss, if any, is debited to the Income and Expenditure Account.

9. Sale of Old Newspapers

Amount paid for newspapers, magazines, periodicals, etc., is debited to Income and Expenditure Account, it being a revenue expense. Thus, amount realised from sale of old newspapers, magazines, periodicals, etc., is credited to Income and Expenditure Account.

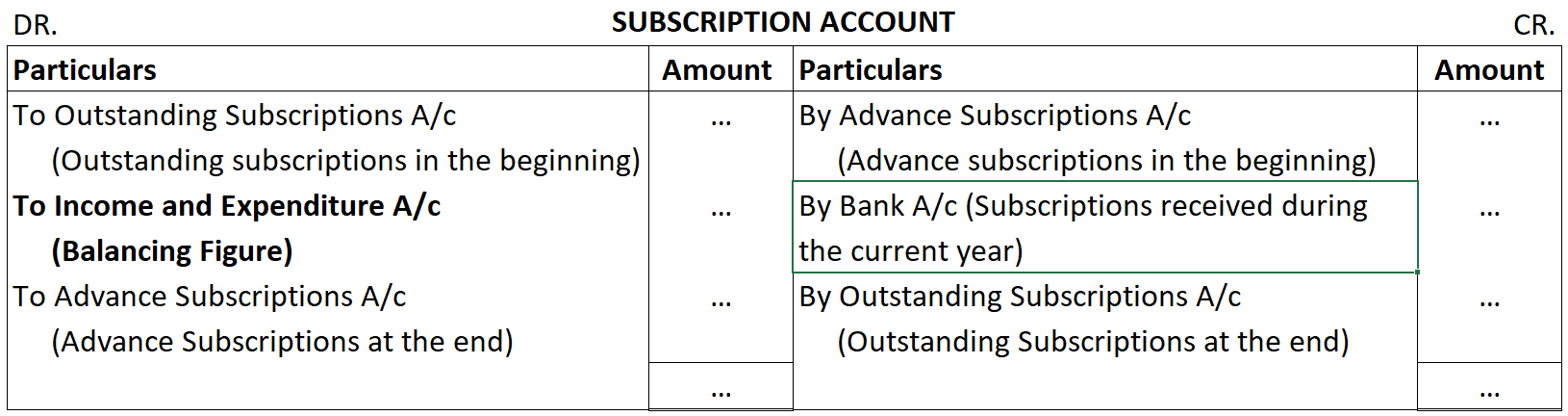

10. Subscriptions

It is the amount paid by the members periodically (quarterly or half-yearly or yearly) so that their membership remains alive. It is a source of income of Not-for-Profit Organisation.

Subscription received whether it is for current, previous or next period, is shown in the debit side of the Receipts and Payments Account.

Subscriptions relating to the current year whether received or not, are shown in the credit side of the Income and Expenditure Account.

Subscriptions not received, i.e., outstanding are shown in the assets side of the Balance Sheet. Subscriptions received in advance for the following years are shown in the liabilities side of the Balance Sheet. Amount of subscriptions to be shown in the Income and Expenditure Account is calculated as follows:

In Account Form:

Subscription Written off:

Part of the subscription earlier accounted as receivable or outstanding may not be receivable is written-off by passing the following Journal entries:

i) For writing off Subscription not receivable:

Subscription written-off A/c Dr…

To Subscription Receivable or Outstanding Subscription A/c

ii) For transfer of subscription written-off to Income and Expenditure Account:

Income and Expenditure A/c …Dr.

To Subscription Written-off A/c

11. Honorarium

Honorarium is a token payment made to a person who has voluntarily undertaken a service which is normally rendered for a fee.

It is an expression of gratitude rather than a payment for the service.

For example, payment made to a Guest Teacher for a lecture is an honorarium.

Honorarium is a revenue expense hence, debited to Income and Expenditure Account.

12. Revenue Expenses

Revenue expenses are expenses incurred by the Not-for-Profit Organisation to carry out the operations or activities for which it is set-up.

Examples are: wages, salaries, rent, printing and stationery, insurance, advertisement, etc.

Revenue expenses also include expenses incurred on the maintenance of fixed assets, e.g., repairs, depreciation, etc.

All such expenses are debited to the Income and Expenditure Account.

Expenses of capital nature or expenses incurred out of specific funds are not revenue expenses.

13. Revenue Receipts

Revenue receipts are the amounts received as income. Such as Entrance Fee, General Donations, rent, subscription and interest on investments other than interest on specific fund investments.

They are shown in the credit side of Income and Expenditure Account.

14. Capital Expenditure

Expenditure that gives benefit of enduring nature, i.e., the benefit of which is not exhausted or consumed within the accounting period is Capital Expenditure.

Examples: purchase of books, furniture, investments, building, etc., are treated as capital expenditures and shown in the assets side of the Balance Sheet

15. Capital Receipts

Capital Receipts are the receipts by Not-for-Profit Organisation that are received for a specific purpose say, specific donation, specific legacy donation and Life Membership Fee, etc.

16. Cost of Goods Consumed

Not-for-Profit Organisations consume consumable items, e.g., stationery is consumed in the office, medicines in the hospitals, sports materials by a sports club and so on.

In such a case, separate Stock Account for each of the consumable items is prepared to determine the consumption during the year.

Income and Expenditure Account will show correct ‘Surplus’ or ‘Deficit’, only if the goods consumed are debited to Income and Expenditure Account and Closing Stock is shown in the Balance Sheet. The amount of items consumed during the year is calculated as follows:

Opening Stock of Consumable items …

Add: Net Purchases during the year …

Less: Closing Stock (…)

Balance (to be shown in the Income and Expenditure Account) …

Opening Stock of such items will appear in the opening Balance Sheet and closing balance will be shown in the closing Balance Sheet.

Sometimes, the amount of credit purchases in not given in the question. In such a case, the Creditors for Consumable Goods Account should be prepared to determine credit purchases.

It is to be noted that receipts from sale of the consumable items, if any, are accounted as revenue receipt.

Preparation of Income and Expenditure Account and Balance Sheet from Receipts and Payments Account with Additional Information

Income and Expenditure Account from the Receipts and Payments Account and other information is prepared by following the steps as follows:

Step 1. Calculate Opening Capital Fund:

If opening balance of the Capital Fund is not given, Balance Sheet in the beginning of the year is prepared. It is prepared by taking Opening Cash and Bank balances as given in the Receipts and Payments Account, other assets and liabilities as given in the additional information. Difference between the assets and liabilities is Capital Fund.

Step 2. Determine Items of Income from Receipts and Payments Account:

In Receipts and Payments Account, all receipts, whether they relate to current, previous or future periods and whether they are of revenue or capital nature are shown in the debit side. But, in the Income and Expenditure Account only revenue receipts of current accounting period (whether received or not) are taken. Thus,

(a) Revenue receipts in which no adjustment is required, are shown in the credit side of the Income and Expenditure Account.

(b) Revenue receipts in which adjustment is required, determine income for the current accounting period and show in the credit side of the Income and Expenditure Account. Incomes requiring adjustments can be for subscriptions rent and interest, etc. It is determined as follows:

(c) Show capital receipts in the appropriate assets and liabilities accounts and then incorporate them in the Balance Sheet.

Step 3. Determine Items of Expenses from Receipts and Payments Account:

Identify from the payments side (Credit Side) of Receipts and Payments Account, revenue payments and capital payments.

(a) Revenue payments which do not require adjustment, are shown in the debit side of the Income and Expenditure Account.

(b) Revenue payments which require adjustment, determine the expense for the current accounting period and show them in the debit side of the Income and Expenditure Account. It is determined as follows:

(c) Show capital payments in the appropriate assets and liabilities accounts and show them in the Balance Sheet.

Step 4. Items not existing in Receipts and Payments Account:

Following items do not exist in Receipts and Payments Account but are shown in Income and Expenditure Account:

(a) Depreciation on fixed assets as an expense, i.e., in the debit side.

(b) Outstanding Expenses as expenses, i.e., in the debit side.

(c) Accrued or outstanding incomes as an income, i.e., in the credit side.

(d) Loss on sale of fixed assets, if any, as expense (loss), i.e., in the debit side.

(e) Gain (Profit) on sale of fixed assets, if any, as income, i.e., in the credit side.

Deduct the amount of depreciation from fixed assets in the Balance Sheet after adjusting purchase and sale of fixed assets.

Step 5. Determine Surplus or Deficit in Income and Expenditure Account:

By comparing total of debit side and total of credit side of Income and Expenditure Account.

If total of credit side is more than the total of debit side, it is surplus (i.e., excess of income over expenditure). And

If, total of debit side is more than the total of credit side, it is deficit (i.e., excess of expenditure over income).

Surplus or deficit is transferred to the Capital Fund and shown in the Balance Sheet.

Step 6. Closing Balance Sheet.

Prepare Balance Sheet as at the end of the year after taking into account opening balances of assets, liabilities and opening Capital Fund, surplus or deficit, purchase and sale of assets during the year and charging depreciation on the fixed assets.