TS Grewal Double Entry Book Keeping Class 12 Solutions Volume1: Accounting for Partnership Firms

TS Grewal Accountancy Class 12 Solutions Chapter 7th Dissolution of a Partnership Firm are part of TS Grewal Accountancy Class 12 Solutions.

Here we have given TS Grewal Accountancy Class 12 Solutions Chapter 7th Dissolution of a Partnership Firm

| Board | CBSE |

| Textbook | NCERT |

| Book | Accounting for Partnership Firms |

| Volume | I |

| Class | 12th |

| Subject | Accountancy |

| Chapter | 7 |

| Chapter Name | Dissolution of a Partnership Firm |

| Number of Questions (Solved) | 54 |

| Category | TS Grewal’s Solutions |

T.S. Grewal’s Accountancy Class 12 Solutions – Chapter 7th Dissolution of a Partnership Firms

Question 1:

Land and Building (book value) ₹ 1,60,000 sold for ₹ 3,00,000 through a broker who charged 2% commission on the deal. Journalise the transaction, at the time of dissolution of the firm.

ANSWER:

Question 2:

Pass Journal entries in the following cases?

(a) Expenses of realisation ₹ 1,500.

(b) Expenses of realisation ₹ 600 but paid by Mohan, a partner.

(c) Mohan, one of the partners of the firm, was asked to look into the dissolution of the firm for which he was allowed a commission of ₹ 2,000.

(d) Motor car of book value ₹ 50,000 taken over by creditors of the book value of ₹ 40,000 in full settlement.

ANSWER:

Question 3:

Pass Journal entries for the following:

(a) Realisation expenses of ₹ 15,000 were to be met by Rahul, a partner, but were paid by the firm.

(b) Ramesh, a partner, was paid remuneration of ₹ 25,000 and he was to meet all expenses.

(c) Anuj, a partner, was paid remuneration of ₹ 20,000 and he was to meet all expenses. Firm paid an expense of ₹ 5,000.

ANSWER:

Question 4:

Pass Journal entries for the following:

(a) Realisation expenses amounted to ₹ 10,000 were paid by the firm on behalf of Alok, a partner, with whom it was agreed at ₹ 7,500.

(b) Realisation expenses amounted to ₹ 5,000. It was agreed that the firm will pay ₹ 2,000 and balance by Ravinder, a partner.

(c) Dissolution expenses amounted to ₹ 10,000 were paid by Amit, a partner, on behalf of the firm.

ANSWER:

Question 5:

Record necessary Journal entries in the following cases:

(a) Creditors worth ₹ 85,000 accepted ₹ 40,000 as cash and Investment worth ₹ 43,000, in full settlement of their claim.

(b) Creditors were ₹ 16,000. They accepted Machinery valued at ₹ 18,000 in settlement of their claim.

(c) Creditors were ₹ 90,000. They accepted Building valued at ₹ 1,20,000 and paid cash to the firm ₹ 30,000.

ANSWER:

Question 6:

Pass Journal entries for the following at the time of dissolution of a firm:

(a) Sale of Assets − ₹ 50,000.

(b) Payment of Liabilities − ₹ 10,000.

(c) A commission of 5% allowed to Mr. X, a partner, on sale of assets.

(d) Realisation expenses amounted to ₹ 15,000. The firm had agreed with Amrit, a partner, to reimburse him up to ₹ 10,000.

(e) Z, an old customer, whose account for ₹ 6,000 was written off as bad in the previous year, paid 60% of the amount written off.

(f) Investment (Book Value ₹ 10,000) realised at 150%.

ANSWER:

Question 7:

Pass Journal entries for the following transactions at the time of dissolution of the firm:

(a) Loan of ₹ 10,000 advanced by a partner to the firm was refunded.

(b) X, a partner, takes over an unrecorded asset (Typewriter) at ₹ 300.

(c) Undistributed balance (Debit) of Profit and Loss Account ₹ 30,000. The firm has three partners X,Y and Z.

(d) Assets of the firm realised ₹ 1,25,000.

(e) Y who undertakes to carry out the dissolution proceedings is paid ₹ 2,000 for the same.

(f) Creditors are paid ₹ 28,000 in full settlement of their account of ₹ 30,000.

ANSWER:

Question 8:

Pass necessary Journal entries for the following transactions on the dissolution of the firm P and Q after the various assets (other than cash) and outside liabilities have been transferred to Realisation Account:

(a) Bank Loan ₹ 12,000 was paid.

(b) Stock worth ₹ 16,000 was taken over by partner Q.

(c) Partner P paid a creditor ₹ 4,000.

(d) An asset not appearing in the books of accounts realised ₹ 1,200.

(e) Expenses of realisation ₹ 2,000 were paid by partner Q.

(f) Profit on realisation ₹ 36,000 was distributed between P and Q in 5 : 4 ratio.

ANSWER:

Question 9:

X, Y and Z are partners in a firm sharing profits in the ratio of 3 : 2 : 1 respectively. The firm was dissolved on 1st March, 2013. After transferring assets (other than cash) and third party liabilities to the ‘Realisation Account’ you are provided with the following information:

(a) There was a balance of ₹ 18,000 in the firm’s Profit and Loss Account.

(b) There was an unrecorded bike of ₹ 50,000 which was taken over by X.

(c) Creditors of ₹ 5,000 were paid ₹ 4,000 in full settlement of accounts.

Pass necessary Journal entries for the above at the time of dissolution of firm.

ANSWER:

Question 10:

Pass necessary Journal entries to record the following unrecorded assets and liabilities in the books of Paras and Priya:

(a) There was an old furniture in the firm which had been written off completely in the books. This was sold for ₹ 3,000.

(b) Ashish, an old customer whose account for ₹ 1,000 was written off as bad in the previous year, paid 60%, of the amount.

(c) Paras agreed to takeover the firm’s goodwill (not recorded in the books of the firm), at a valuation of ₹ 30,000.

(d) There was an old typewriter which had been written off completely from the books. It was estimated to realise ₹ 400. It was taken by Priya at an estimated price less 25%.

(e) There were 100 shares of ₹ 10 each in Star Limited acquired at a cost of ₹ 2,000 which had been written-off completely from the books. These shares are valued @ ₹ 6 each and divided among the partners in their profit-sharing ratio.

ANSWER:

Question 11:

Aman and Harsh were partners in a firm. They decided to dissolve their firm. Pass necessary Journal entries for the following after various assets (other than Cash and Bank) and third party liabilities have been transferred to Realisation Account:

(a) There was furniture worth ₹ 50,000. Aman took over 50% of the furniture at 10% discount and the remaining furniture was sold at 30% profit on book value.

(b) Profit and Loss Account was showing a credit balance of ₹ 15,000 on the date of dissolution.

(c) Harsh’s loan of ₹ 6,000 was discharged at ₹ 6,200.

(d) The firm paid realisation expenses amounting to ₹ 5,000 on behalf of Harsh who had to bear these expenses.

(e) There was a bill for 1,200 under discount. The bill was received from Soham who proved insolvent and a first and final dividend of 25% was received from his estate.

(f) Creditors, to whom the firm owed ₹ 6,000, accepted stock of ₹ 5,000 at a discount of 5% and the balance in cash.

ANSWER:

Question 12:

Rohit, Kunal and Sarthak are partners in a firm. They decided to dissolve their firm. Pass necessary Journal entries for the following after various assets (other than Cash and Bank) and the third party liability have been transferred to Realisation Account:

(a) Kunal agreed to pay off his wife’s loan of ₹ 6,000.

(b) Total Creditors of the firm were ₹ 40,000. Creditors worth ₹ 10,000 were given a piece of furniture costing ₹ 8,000 in full and final settlement. Remaining Creditors allowed a discount of 10%.

(c) Rohit had given a loan of ₹ 70,000 to the firm which was duly paid.

(d) A machine which was not recorded in the books was taken over by Kunal at ₹ 3,000, whereas its expected value was ₹ 5,000.

(e) The firm had a debit balance of ₹ 15,000 in the Profit and Loss Account on the date of dissolution.

(f) Sarthak paid the realisation expenses of ₹ 16,000 out of his private funds, who was to get a remuneration of ₹ 15,000 for completing dissolution process and was responsible to bear all the realisation expenses.

ANSWER:

Question 13:

Book Value of assets (other than cash and bank) transferred to Realisation Account is ₹ 1,00,000. 50% of the assets are taken over by a partner Atul, at a discount of 20%; 40% of the remaining assets are sold at a profit of 30% on cost; 5% of the balance being obsolete, realised nothing and remaining assets are handed over to a Creditor, in full settlement of his claim.

You are required to record the Journal entries for realisation of assets.

ANSWER:

Question 14:

Lal and Pal were partners in a firm sharing profits in the ratio of 3 : 7. On 1st April, 2015 their firm was dissolved. After transferring assets (other than cash) and outsider’s liabilities to Realisation Account, you are given the following information:

(a) A creditor of ₹ 3,60,000 accepted machinery valued at ₹ 5,00,000 and paid to the firm ₹ 1,40,000.

(b) A second creditor for ₹ 50,000 accepted stock at ₹ 45,000 in full settlement of his claim.

(c) A third creditor amounting to ₹ 90,000 accepted ₹ 45,000 in cash and investments worth ₹ 43,000 in full settlement of his claim.

(d) Loss on dissolution was ₹ 15,000.

Pass necessary Journal entries for the above transactions in the books of firm assuming that all payments were made by cheque.

ANSWER:

Question 15:

Pass the Journal entries for the following transactions on the dissolution of the firm of P and Q after various assets (other than cash) and outside liabilities have been transferred to Realisation Account:

(a) Stock ₹ 2,00,000. ‘P‘ took over 50% of stock at a discount of 10%. Remaining stock was sold at a profit of 25% on cost.

(b) Debtors ₹ 2,25,000. Provision for Doubtful Debts ₹ 25,000. ₹ 20,000 of the book debts proved bad.

(c) Land and Building (Book value ₹ 12,50,000) sold for ₹ 15,00,000 through a broker who charged 2% commission.

(d) Machinery (Book value ₹ 6,00,000) was handed over to a creditor at a discount of 10%.

(e) Investment (Book value ₹ 60,000) realised at 125%.

(f) Goodwill of ₹ 75,000 and prepaid fire insurance of ₹ 10,000.

(g) There was an old furniture in the firm which had been written off completely in the books. This was sold for ₹ 10,000.

(h) ‘Z‘ an old customer whose account for ₹ 20,000 was written off as bad in the previous year, paid 60%.

(i) ‘P‘ undertook to pay Mrs. P‘s loan of ₹ 50,000.

(j) Trade creditors ₹ 1,60,000. Half of the trade creditors accepted Plant and Machinery at an agreed valuation of ₹ 54,000 and cash in full settlement of their claims after allowing a discount of ₹ 16,000. Remaining trade creditors were paid 90% in final settlement.

ANSWER:

Question 16:

What Journal entries would be passed for discharge of following unrecorded liabilities on the dissolution of a firm of partners A and B:

(a) There was a contingent liability in respect of bills discounted but not matured of ₹ 18,500. An acceptor of one bill of ₹ 2,500 became insolvent and fifty paise in a rupee was recovered. The liability of the firm on account of this bill discounted and dishonoured has not so far been recorded.

(b) There was a contingent liability in respect of a claim for damages for ₹ 75,000, such liability was settled for ₹ 50,000 and paid by the partner A.

(c) Firm will have to pay ₹ 10,000 as compensation to an injured employee, which was a contingent liability not accepted by the firm.

(d) ₹ 5,000 for damages claimed by a customer has been disputed by the firm. It was settled at 70% by a compromise between the customer and the firm.

ANSWER:

Question 17:

Pass necessary Journal entries on the dissolution of a firm in the following cases:

(a) Dharam, a partner, was appointed to look after the process of dissolution at a remuneration of ₹ 12,000 and he had to bear the dissolution expenses. Dissolution expenses ₹ 11,000 were paid by Dharam.

(b) Jay, a partner, was appointed to look after the process of dissolution and was allowed a remuneration of ₹ 15,000. Jay agreed to bear dissolution expenses. Actual dissolution expenses ₹ 16,000 were paid by Vijay, another partner on behalf of Jay.

(c) Deepa, a partner, was to look after the process of dissolution and for this work she was allowed a remuneration of ₹ 7,000. Deepa agreed to bear dissolution expenses. Actual dissolution expenses ₹ 6,000 were paid from the firm’s bank account.

(d) Dev, a partner, agreed to do the work of dissolution for ₹ 7,500. He took away stock of the same amount as his commission. The stock had already been transferred to Realisation Account.

(e) Jeev, a partner, agreed to do the work of dissolution for which he was allowed a commission of ₹ 10,000. He agreed to bear the dissolution expenses. Actual dissolution expenses paid by Jeev were ₹ 12,000. These expenses were paid by Jeev by drawing cash from the firm.

(f) A debtor of ₹ 8,000 already transferred to Realisation Account agreed to pay the realisation expenses of ₹ 7,800 in full settlement of his account.

ANSWER:

Realisation Account

Question 18:

Ramesh and Umesh were partners in a firm sharing profits in the ratio of their capitals. On 31st March, 2013, their Balance Sheet was as follows:

| Liabilities |

Amount

(₹) | Assets |

Amount

(₹) | |||||

| Creditors | 1,70,000 | Bank | 1,10,000 | |||||

| Workmen Compensation Reserve | 2,10,000 | Debtors | 2,40,000 | |||||

| General Reserve | 2,00,000 | Stock | 1,30,000 | |||||

| Ramesh’s Current Account | 80,000 | Furniture | 2,00,000 | |||||

| Capital A/cs: | Machinery | 9,30,000 | ||||||

| Ramesh | 7,00,000 | Umesh’s Current Account | 50,000 | |||||

| Umesh | 3,00,000 | 10,00,000 | ||||||

| 16,60,000 | 16,60,000 | |||||||

On the above date the firm was dissolved.

(a) Ramesh took over 50% of stock at ₹ 10,000 less than book value. The remaining stock was sold at a loss of ₹ 15,000. Debtors were realised at a discount of 5%.

(b) Furniture was taken over by Umesh for ₹ 50,000 and machinery was sold for ₹ 4,50,000.

(c) Creditors were paid in full.

(d) There was an unrecorded bill for repairs for ₹ 1,60,000 which was settled at ₹ 1,40,000.

Prepare Realisation Account.

ANSWER:

Question 19:

Pradeep and Rajesh were partners in a firm sharing profits and losses in the ratio of 3 : 2. They decided to dissolve their partnership firm on 31st March, 2018. Pradeep was deputed to realise the assets and to pay off the liabilities. He was paid ₹ 1,000 as commission for his services. The financial position of the firm on 31st March, 2018 was as follows:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

| Creditors | 80,000 | Building | 1,20,000 | ||

| Mrs. Pradeep’s Loan | 40,000 | Investment | 30,600 | ||

| Rajesh’s Loan | 24,000 | Debtors | 34,000 | ||

| Investment Fluctuation Fund | 8,000 | Less : Provision for Doubtful Debts | 4,000 | 30,000 | |

| Capital A/cs: | Bills Receivable | 37,400 | |||

| Pradeep | 42,000 | Bank | 6,000 | ||

| Rajesh | 42,000 | 84,000 | Profit and Loss A/c | 8,000 | |

| Goodwill | 4,000 | ||||

2,36,000 | 2,36,000 | ||||

Following terms and conditions were agreed upon:

(a) Pradeep agreed to pay off his wife’s loan.

(b) Half of the debtors realised ₹ 12,000 and remaining debtors were used to pay off 25% of the creditors.

(c) Investment sold to Rajesh for ₹ 27,000.

(d) Building realised ₹ 1,52,000.

(e) Remaining creditors were to be paid after two months, they were paid immediately at 10% p.a. discount.

(f) Bill receivables were settled at a loss of ₹ 1,400.

(g) Realisation expenses amounted to ₹ 2,500.

Prepare Realisation Account.

ANSWER:

Soon Update…

Realisation Account, Partners’ Capital Accounts and Bank/Cash Account

Question 20:

Balance Sheet of a firm as at 31st March, 2019, when it was decided to dissolve the same, was:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Sundry Creditors | 14,000 | Cash at Bank | 640 | |||||

| General Reserve | 500 | Stock | 4,740 | |||||

| Capital A/cs: | Debtors | 5,540 | ||||||

| X | 4,000 | Machinery | 10,580 | |||||

| Y | 3,000 | 7,000 | ||||||

| 21,500 | 21,500 | |||||||

₹19,500 were realised from all assets except Cash at Bank. The cost of winding up came to ₹ 440. X and Y shared profits in the ratio of 2 : 1 respectively.

Prepare Realisation Account and Capital Accounts of Partners.

ANSWER:

Question 21:

Achal and Vichal were partners in a firm sharing profits in the ratio of 3 : 5. On 31st March, 2019, their Balance Sheet was as follows:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Capital A/cs: | Land and Building | 4,00,000 | ||||||

| Achal | 3,00,000 | Machinery | 3,00,000 | |||||

| Vichal | 5,00,000 | 8,00,000 | Debtors | 2,22,000 | ||||

| Creditors | 1,79,000 | Cash at Bank | 78,000 | |||||

| Employees’ Provident Fund | 21,000 | |||||||

| 10,00,000 | 10,00,000 | |||||||

The firm was dissolved on 1st April, 2019 and the Assets and Liabilities were settled as follows:

(a) Land and Building realised ₹ 4,30,000.

(b) Debtors realised ₹ 2,25,000 (with interest) and ₹ 1,000 were recovered for Bad Debts written off last year.

(c) There was an Unrecorded Investment which was sold for ₹ 25,000.

(d) Vichal took over Machinery at ₹ 2,80,000 for cash.

(e) 50% of the Creditors were paid ₹ 4,000 less in full settlement and the remaining Creditors were paid full amount.

Pass necessary Journal entries for dissolution of the firm.

ANSWER:

Question 22:

Bale and Yale are equal partners of a firm. They decide to dissolve their partnership on 31st March, 2019 at which date their Balance Sheet stood as:

| Liabilities | ₹ | Assets | ₹ | |

| Capital A/cs: | Building | 45,000 | ||

| Bale | 50,000 | Machinery | 15,000 | |

| Yale | 40,000 | 90,000 | Furniture | 12,000 |

| General Reserve | 8,000 | Debtors | 8,000 | |

| Bale’s Loan A/c | 3,000 | Stock | 24,000 | |

| Creditors | 14,000 | Bank | 11,000 | |

| 1,15,000 | 1,15,000 | |||

(a) The assets realised were:

Stock ₹ 22,000; Debtors ₹ 7,500; Machinery ₹ 16,000; Building ₹ 35,000.

(b) Yale took over the Furniture at ₹ 9,000.

(c) Bale agreed to accept ₹ 2,500 in full settlement of his Loan Account.

(d) Dissolution Expenses amounted to ₹ 2,500.

Prepare the:

(i) Realisation Account; (ii) Capital Accounts of Partners;

(iii) Bale’s Loan Account; (iv) Bank Account.

ANSWER:

Question 23:

Shilpa, Meena and Nanda decided to dissolve their partnership on 31st March, 2019. Their profit-sharing ratio was 3 : 2 : 1 and their Balance Sheet was as under:

| Liabilities | ₹ | Assets | ₹ | |

| Capital A/cs: | Land | 81,000 | ||

| Shilpa | 80,000 | Stock | 56,760 | |

| Meena | 40,000 | 1,20,000 | Debtors | 18,600 |

| Bank Loan | 20,000 | Nanda’s Capital | 23,000 | |

| Creditors | 37,000 | Cash | 10,840 | |

| Provision For Doubtful Debts | 1,200 | |||

| General Reserve | 12,000 | |||

| 1,90,200 | 1,90,200 | |||

It is agreed as follows:

The stock of value of ₹ 41,660 are taken over by Shilpa for ₹ 35,000 and she agreed to discharge bank loan. The remaining stock was sold at ₹ 14,000 and debtors amounting to ₹ 10,000 realised ₹ 8,000. Land is sold for ₹ 1,10,000. The remaining debtors realised 50% at their book value. Cost of realisation amounted to ₹ 1,200. There was a typewriter not recorded in the books worth of ₹ 6,000 which were taken over by one of the Creditors at this value. Prepare Realisation Account, Partners’ Capital Accounts, and Cash Account to Close the books of the firm.

ANSWER:

Question 24:

A and B are partners in a firm sharing profits and losses in the ratio of 3 : 2. On 31st March, 2019, their Balance Sheet was as follows:

| BALANCE SHEET as at 31st March, 2019 | ||||

| Liabilities | Amount (₹) | Assets | Amount (₹) | |

| Creditors | 38,000 | Cash at Bank | 11,500 | |

| Mrs. A‘s Loan | 10,000 | Stock | 6,000 | |

| B‘s Loan | 15,000 | Debtors | 19,000 | |

| Reserve | 5,000 | Furniture | 4,000 | |

| A‘s Capital | 10,000 | Plant | 28,000 | |

| B‘s Capital | 8,000 | 18,000 | Investments | 10,000 |

| Profit and LossA/C | 7,500 | |||

| 86,000 | 86,000 | |||

The firm was dissolved on 31st March, 2019 and both the partners agreed to the following:

(a) A took Investments at an agreed value of ₹ 8,000. He also agreed to settle Mrs. A’s Loan.

(b) Other assets realised as: Stock − ₹ 5,000; Debtors − ₹ 18,500; Furniture − ₹ 4,500; Plant − ₹ 25,000.

(c) Expenses of realisation came to ₹ 1,600.

(d) Creditors agreed to accept ₹ 37,000 in full settlement of their claims.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

ANSWER:

Question 25:

Balance Sheet of P, Q and R as at 31st March, 2019, who were sharing profits in the ratio of 5 : 3 : 1, was:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

| Bills Payable | 40,000 | Cash at Bank | 40,000 | ||

| Loan from Bank | 30,000 | Stock | 19,000 | ||

| General Reserve | 9,000 | Sundry Debtors | 42,000 |

| |

| Capital A/cs: |

| Less: Provision for Doubtful Debts | 2,000 | 40,000 | |

| P | 44,000 | ||||

| Q | 36,000 |

| Building | 40,000 | |

| R | 20,000 | 1,00,000 | Plant and Machinery | 40,000 | |

|

|

| |||

1,79,000 | 1,79,000 | ||||

|

| ||||

The partners dissolved the business. Assets realised − Stock ₹ 23,400; Debtors 50%; Fixed Assets 10% less than their book value. Bills Payable were settled for ₹ 32,000. There was an Outstanding Bill of Electricity ₹ 800 which was paid off. Realisation expenses ₹ 1,250 were also paid.

Prepare Realisation Account, Partner’s Capital Accounts and Bank Account.

ANSWER:

Question 26:

Vinod, Vijay and Venkat are partners sharing profits and losses in the ratio of 3 : 2 : 1. They decided to dissolve their firm on 31st March, 2019, the date on which their Balance Sheet stood as:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

| Creditors | 17,000 | Bank | 3,500 | ||

| Bills Payable | 12,000 | Stock | 19,800 | ||

| Vinod’s Loan | 5,300 | Debtors | 15,000 |

| |

| General Reserve | 6,000 | Less: Provision for Doubtful Debts | 1,000 | 14,000 | |

| Capital A/cs: | Investments | 4,000 | |||

| Vinod | 25,000 | Furniture | 10,000 | ||

| Vijay | 11,000 |

| Machinery | 33,000 | |

| Venkat | 8,000 | 44,000 | |||

|

|

| |||

84,300 | 84,300 | ||||

|

| ||||

The following additional information is given:

(a) The Investments are taken by Vinod for ₹ 5,000 in settlement of his loan

(b)

| Assets realised as follows: | ₹ |

| Stock | 17,500 |

| Debtors | 14,500 |

| Furniture | 6,800 |

| Machinery | 30,300 |

(c) Expenses on realisation amounted to ₹ 2,000.

Close the books of the firm giving relevant Ledger Accounts.

ANSWER:

Question 27:

P, Q and R were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. They agreed to dissolve their partnership firm on 31st March, 2019. P was deputed to realise the assets and pay the liabilities. He was paid ₹ 1,000 as commission for his services. The financial position of the firm was:

Balance Sheet as at 31st March, 2019 | ||||||||

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Creditors | 10,000 | Stock | 5,500 | |||||

| Bills Payable | 3,700 | Investments | 15,000 | |||||

| Investments Fluctuation Reserve | 4,500 | Debtors | 7,100 | |||||

| Capital A/cs: | Less: Provision for Doubtful Debtors | 450 | 6,650 | |||||

| P | 37,550 | Cash | 5,600 | |||||

| Q | 15,000 | 52,550 | R’s Capital A/c | 8,000 | ||||

| Plant and Machinery | 30,000 | |||||||

| 70,750 | 70,750 | |||||||

P took over Investments for ₹ 12,500. Stock and Debtors realised ₹ 11,500. Plant and Machinery were sold to Q for ₹ 22,500 for cash. Unrecorded assets realised ₹ 1,500. Realisation expenses paid amounted to ₹ 900.

Prepare necessary Ledger Accounts to close the books of the firm.

ANSWER:

Question 28:

Ashu and Harish are partners sharing profit and losses as 3 : 2 . They decided to dissolve the firm on 31st March, 2019. Their Balance Sheet on the above date was:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Capital A/cs: | Building | 80,000 | ||||||

| Ashu | 1,08,000 | Machinery | 70,000 | |||||

| Harish | 54,000 | 1,62,000 | Furniture | 14,000 | ||||

| Creditors | 88,000 | Stock | 20,000 | |||||

| Bank Overdraft | 50,000 | Investments | 60,000 | |||||

| Debtors | 48,000 | |||||||

| Cash in Hand | 8,000 | |||||||

| 3,00,000 | 3,00,000 | |||||||

Ashu is to take over the building at ₹ 95,000 and Machinery and Furniture is taken over by Harish at value of ₹ 80,000. Ashu agreed to pay Creditor and Harish agreed to meet Bank overdraft. Stock and Investments are taken by both partner in profit-sharing ratio. Debtors realised for ₹ 46,000, expenses of realisation amounted to ₹ 3,000. Prepare necessary Ledger Accounts.

ANSWER:

Question 29:

A, B and C were equal partners. On 31st March, 2019, their Balance Sheet stood as:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |

| Creditors | 50,400 | Cash | 3,700 | |

| Reserve | 12,000 | Stock | 20,100 | |

| Capital A/cs: | Debtors | 62,600 | ||

| A | 40,000 | Loan to A | 10,000 | |

| B | 25,000 | Investments | 16,000 | |

| C | 15,000 | 80,000 | Furniture | 6,500 |

| Building | 23,500 | |||

| 1,42,400 | 1,42,400 | |||

The firm was dissolved on the above date on the following terms:

(a) For the purpose of dissolution, Investments were valued at ₹ 18,000 and A took over the Investments at this value.

(b) Fixed Assets realised ₹ 29,700 whereas Stock and Debtors realised ₹ 80,000.

(c) Expenses of realisation amounted to ₹ 1,300.

(d) Creditors allowed a discount of ₹ 800.

(e) One Bill receivable for ₹ 1,500 under discount was dishonoured as the acceptor had become insolvent and was unable to pay anything and hence the bill had to be met by the firm.

Prepare Realisation Account, Partner’s Capital Accounts and Cash Account showing how the accounts would finally be settled among the partners.

ANSWER:

Question 30:

Yogesh and Naresh were partners sharing profits equally. They dissolved the firm on 1st April, 2019. Naresh was assigned the responsibility to realise the assets and pay the liabilities at a remuneration of ₹10,000 including expenses. Balance Sheet of the firm as on that date was as follows:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

| Creditors | 40,000 | Cash/Bank | 6,000 | ||

| Bills Payable | 40,000 | Investments | 30,000 | ||

| Naresh’s Loan | 44,000 | Debtors | 40,000 |

| |

| Mrs. Yogesh’s Loan | 42,000 | Less: Provision for Doubtful Debts | 4,000 | 36,000 | |

| Investment Fluctuation Reserve | 8,000 | Bills Receivable | 33,400 | ||

| Capital A/cs: | Profit and Loss A/c | 1,10,600 | |||

| Yogesh | 21,000 |

| |||

| Naresh | 21,000 | 42,000 | |||

|

|

| |||

2,16,000 | 2,16,000 | ||||

|

| ||||

The firm was dissolved on following terms:

(a) Yogesh was to pay his wife’s loan.

(b) Debtors realised ₹ 30,000.

(c) Naresh was to take investments at an agreed value of ₹ 26,000.

(d) Creditors and Bills Payable were payable after two months but were paid immediately at a discount of 15% p.a.

(e) Bills Receivable were received allowing 5% rebate.

(f) A Debtor previously written off as Bad Debt paid ₹ 15,000.

(g) An unrecorded asset realised ₹10,000.

Prepare Realisation Account, Partners’ Capital Accounts, Partners’ Loan Account and Cash/Bank Account.

ANSWER:

Question 31:

A, B and C are in partnership sharing profits and losses in the proportions of 1/2, 1/3 and 1/6 respectively. On 31st March, 2019, they decided to dissolve the partnership and the position of the firm on this date is represented by the following Balance Sheet:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |

| Creditors | 40,000 | Cash at Bank | 3,000 | |

| Loan A/c: | Stock | 50,000 | ||

| A | 10,000 | Sundry Debtors | 50,000 | |

| Workmen Compensation Reserve | 21,000 | Land and Building | 57,000 | |

| Capital A/cs: | Profit and Loss A/c | 15,000 | ||

| A | 60,000 | Advertisement Suspense A/c | 6,000 | |

| B | 40,000 | |||

C | 10,000 | 1,10,000 | ||

| 1,81,000 | 1,81,000 | |||

During the course of realisation, a liability under a suit for damages is settled at ₹ 20,000 as against ₹ 5,000 only provided for in the books of the firm.

Land and Building were sold for ₹ 40,000 and the Stock and Sundry Debtors realised ₹ 30,000 and ₹ 42,000 respectively. The expenses of realisation amounted to ₹ 1,200.

There was a car in the firm, which was completely written off from the books. It was taken by A for ₹ 20,000. He also agreed to pay Outstanding Salary of ₹ 20,000 not provided in books.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account in the books of the firm.

ANSWER:

Question 32:

A and B are partners in a firm sharing profits and losses in the ratio of 2 : 1. On 31st March, 2019, their Balance Sheet was:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Bank Overdraft | 30,000 | Cash in Hand | 6,000 | |||||

| General Reserve | 56,000 | Bank Balance | 10,000 | |||||

| Investments Fluctuation Reserve | 20,000 | Sundry Debtors | 26,000 | |||||

| A‘s Loan | 34,000 | Less: Provision for Doubtful Debtors | 2,000 | 24,000 | ||||

| Capital A/c: | ||||||||

| A | 50,000 | Investments | 40,000 | |||||

| Stock | 10,000 | |||||||

| Furniture | 10,000 | |||||||

| Building | 60,000 | |||||||

| B’s Capital | 30,000 | |||||||

| 1,90,000 | 1,90,000 | |||||||

On that date, the partners decide to dissolve the firm. A took over Investments at an agreed valuation of ₹ 35,000. Other assets were realised as follows:

Sundry Debtors: Full amount. The firm could realise Stock at 15% less and Furniture at 20% less than the book value. Building was sold at ₹ 1,00,000.

Compensation to employees paid by the firm amounted to ₹ 10,000. This liability was not provided for in the above Balance Sheet.

You are required to close the books of the firm by preparing Realisation Account, Partners’ Capital Accounts and Bank Account.

ANSWER:

Question 33:

Ashok, Babu and Chetan are in partnership sharing profit in the proportion of 1/2, 1/3, 1/6 respectively. They dissolve the partnership of the 31st March, 2019 when the Balance Sheet of the firm as under:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Sundry Creditors | 20,000 | Bank | 7,500 | |||||

| Bills Payable | 25,500 | Sundry Debtors | 58,000 | |||||

| Babu’s Loan | 30,000 | Stock | 39,500 | |||||

| Capital A/cs: | Machinery | 48,000 | ||||||

| Ashok | 70,000 | Investments | 42,000 | |||||

| Babu | 55,000 | Freehold Property | 50,500 | |||||

| Chetan | 27,000 | 1,52,000 | ||||||

| Current A/cs: | ||||||||

| Ashok | 10,000 | |||||||

| Babu | 5,000 | |||||||

| Chetan | 3,000 | 18,000 | ||||||

| 2,45,500 | 2,45,500 | |||||||

The Machinery was taken over by Babu for ₹ 45,000, Ashok took over the Investments for ₹ 40,000 and Freehold property took over by Chetan at ₹ 55,000. The remaining Assets realised as follows:

Sundry Debtors ₹ 56,500 and Stock ₹ 36,500. Sundry Creditors were settled at discount of 7%. A Office computer, not shown in the books of accounts realised ₹ 9,000. Realisation expenses amounted to ₹ 3,000.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

ANSWER:

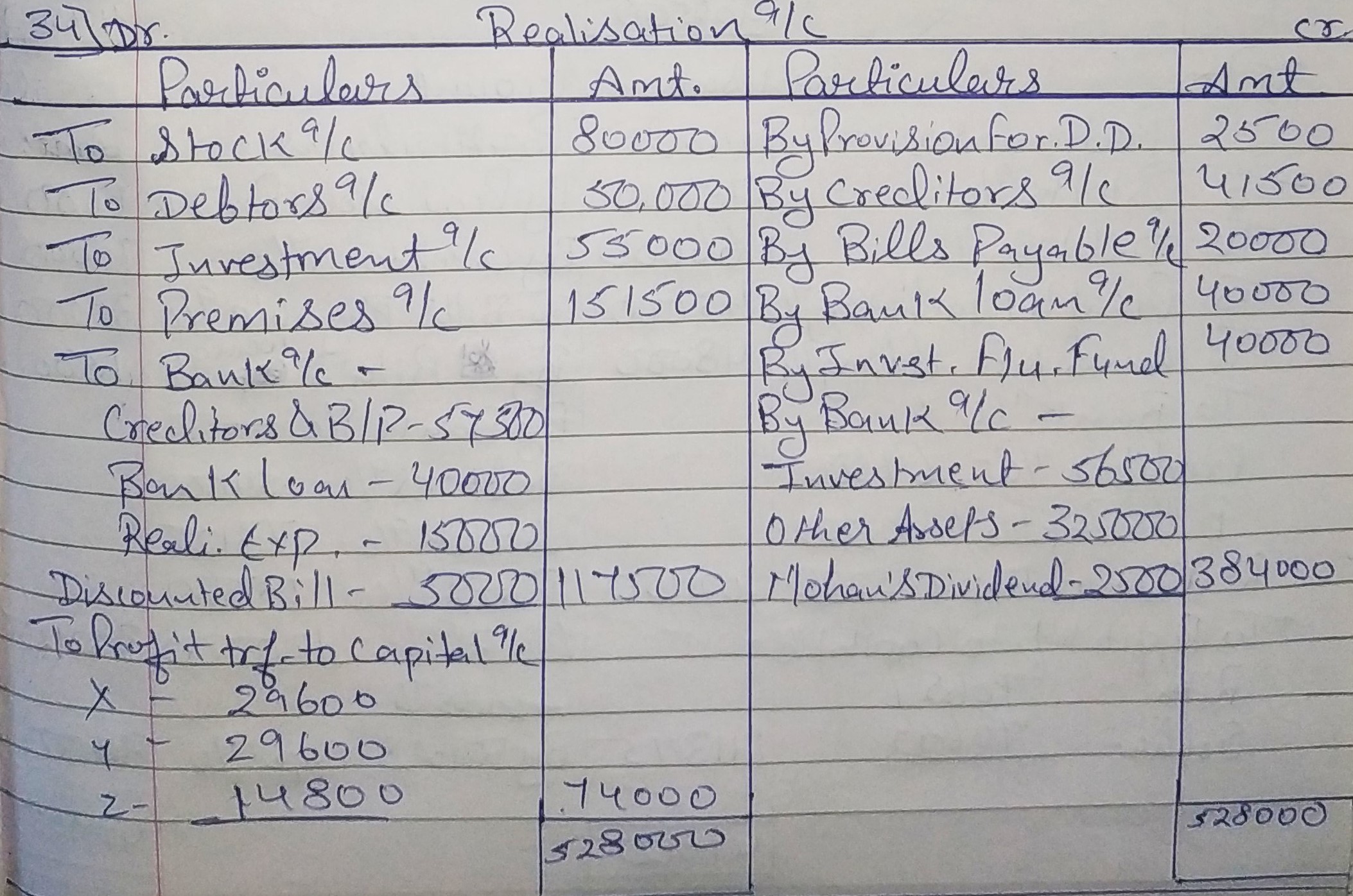

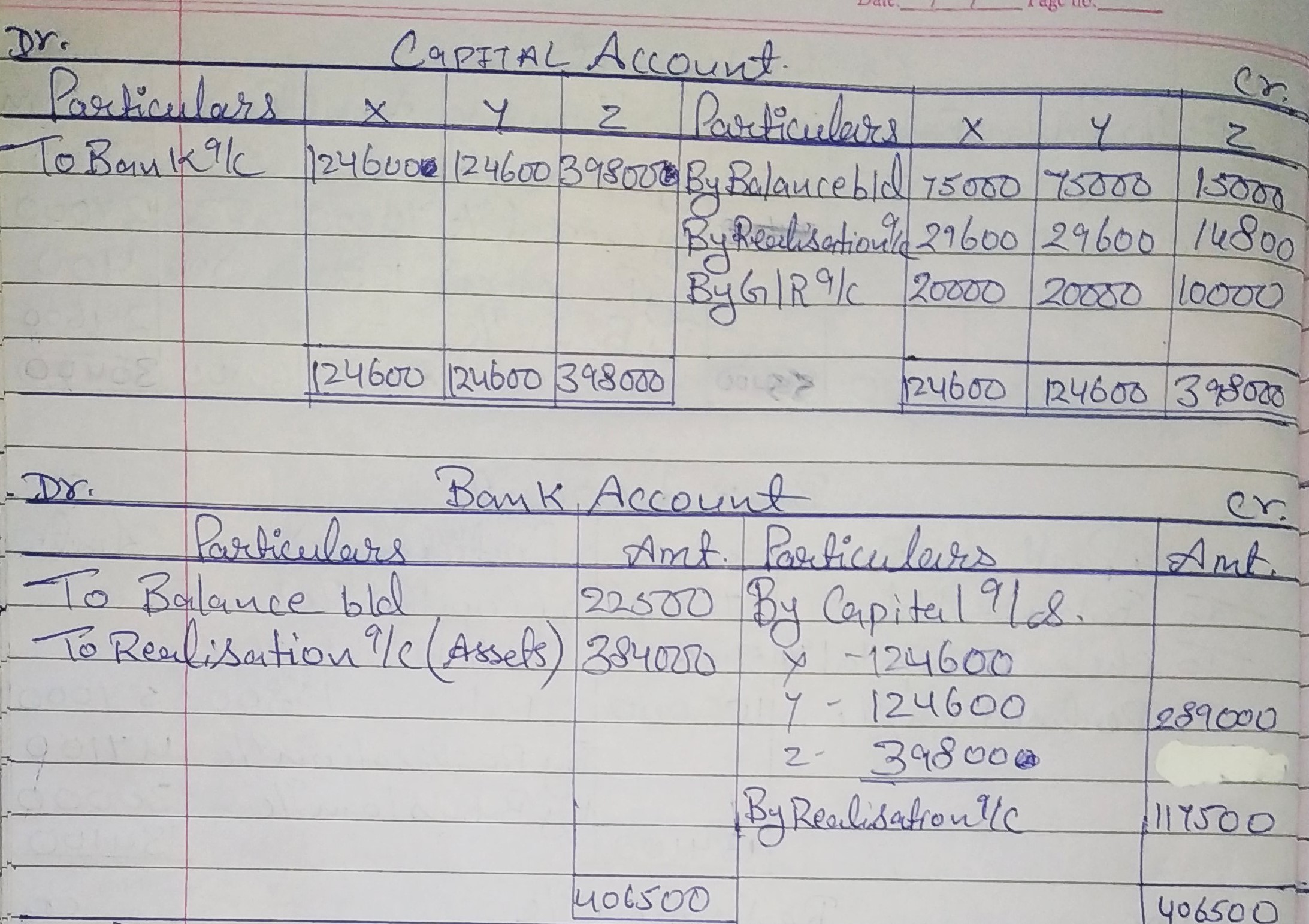

Question 34:

X, Y and Z carrying on business as merchants and sharing profits and losses in the ratio of 2 : 2 : 1, dissolved their firm as at 31st March, 2019 on which date their Balance Sheet was as follows:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Sundry Creditors | 41,500 | Cash at Bank | 22,500 | |||||

| Bills Payable | 20,000 | Stock | 80,000 | |||||

| Bank Loan | 40,000 | Debtors | 50,000 | |||||

| General Reserve | 50,000 | Less: Provision for Doubtful Debts | 2,500 | 47,500 | ||||

| Investments Fluctuation Reserve | 40,000 | Investments | 55,000 | |||||

| Capital A/cs: | Premises | 1,51,500 | ||||||

| X | 75,000 | |||||||

| Y | 75,000 | |||||||

| Z | 15,000 | 1,65,000 | ||||||

| 3,56,500 | 3,56,500 | |||||||

A bill for ₹ 5,000 received from Mohan discounted from bank is not met on maturity.

The assets except Cash at Bank and Investments were sold to a company which paid ₹ 3,25,000 in cash.The Investments were sold and ₹ 56,500 were received. Mohan proved insolvent and a dividend of 50% was received from his estate. Sundry Creditors (including Bills Payable) were paid ₹ 57,500 in full settlement. Realisation Expenses amounted to ₹ 15,000.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

ANSWER:

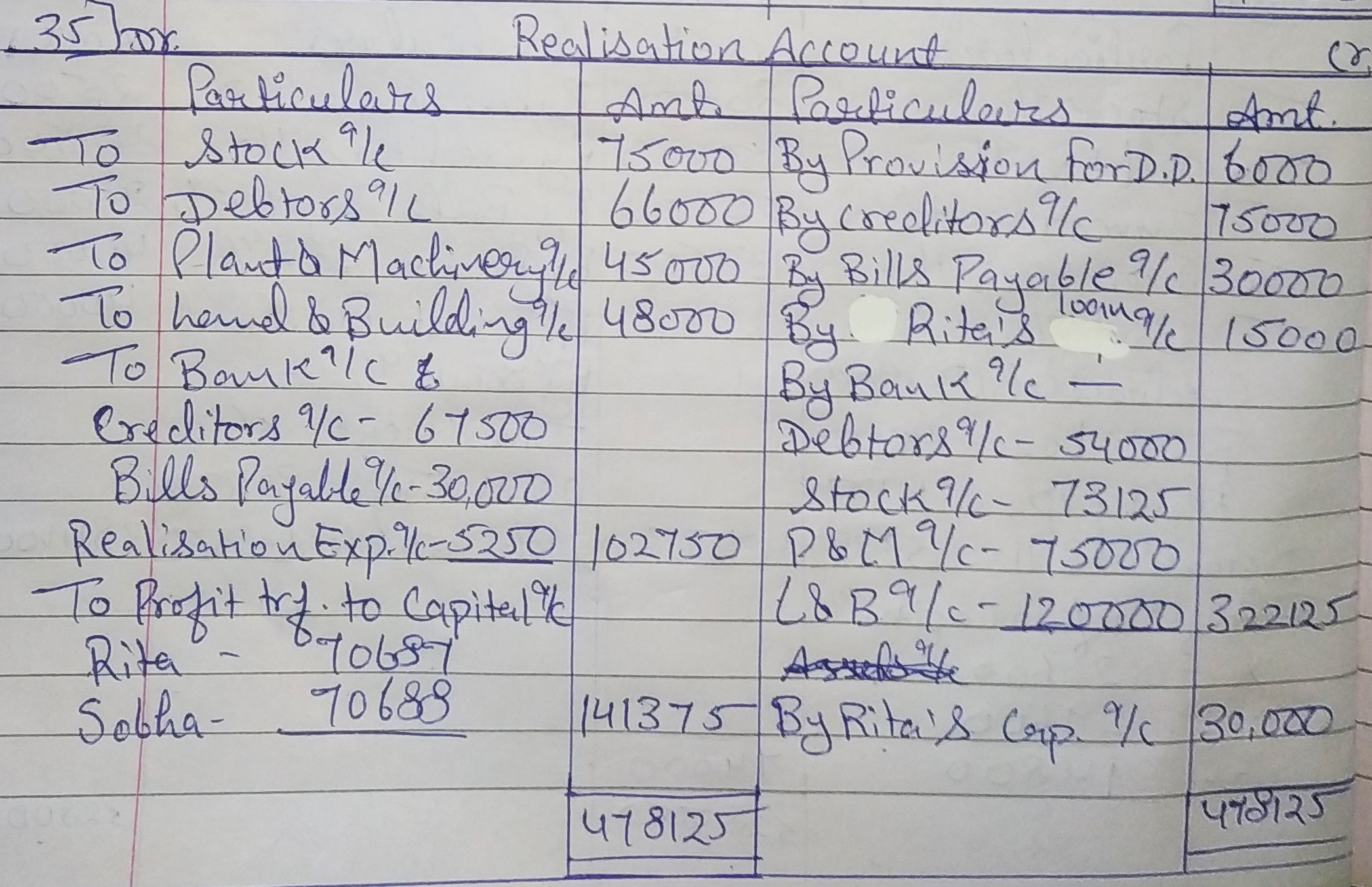

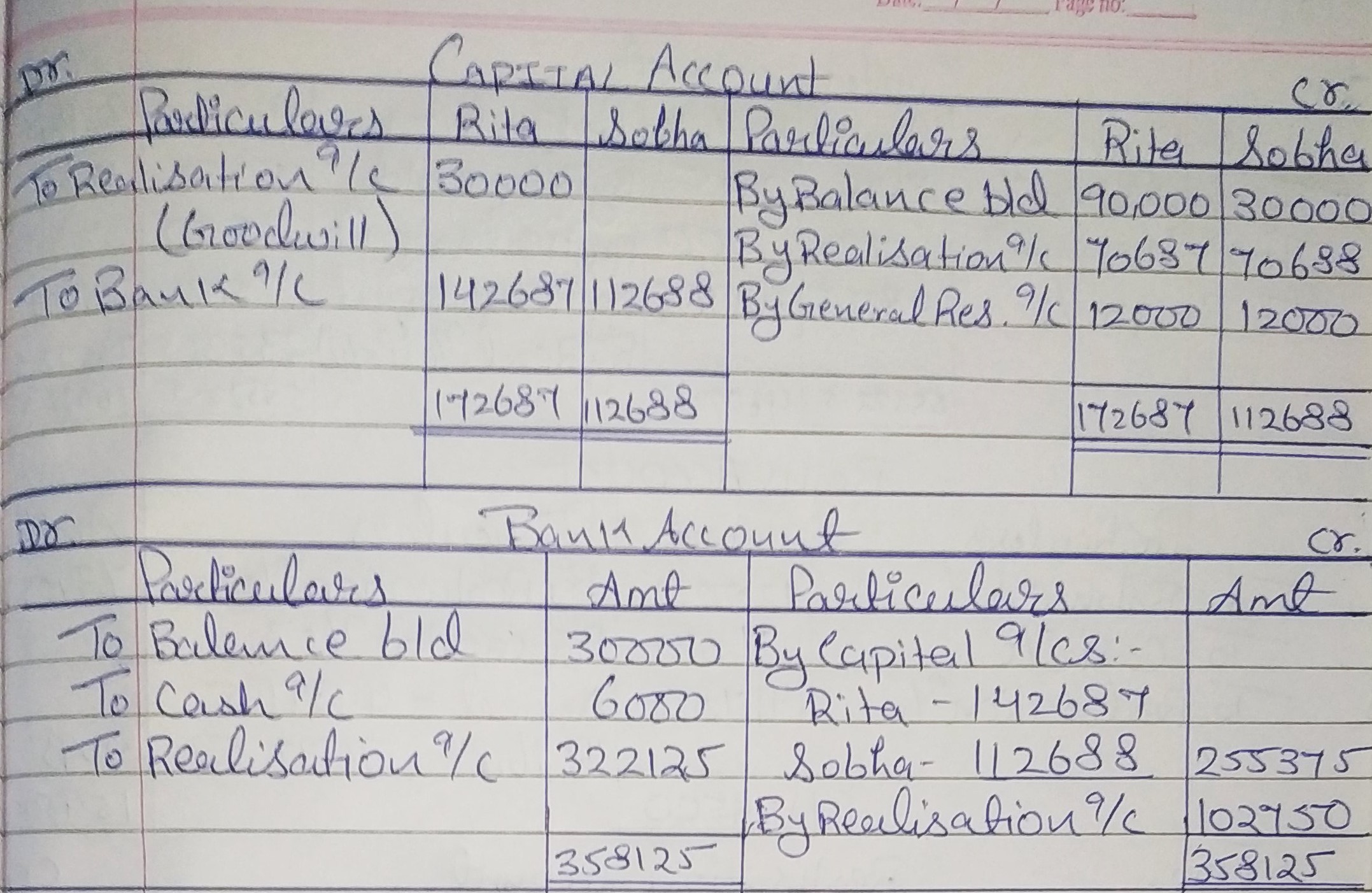

Question 35:

Rita and Sobha are partners in a firm, Fancy Garments Exports, sharing profits and losses equally. On 1st April, 2019, the Balance Sheet of the firm was:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |||||

| Sundry Creditors | 75,000 | Cash | 6,000 | |||||

| Bills Payable | 30,000 | Bank | 30,000 | |||||

| Rita’s Loan | 15,000 | Stock | 75,000 | |||||

| Reserve | 24,000 | Book Debts | 66,000 | |||||

| Capital A/cs: | Less: Provision for Doubtful Debts | 6,000 | 60,000 | |||||

| Rita | 90,000 | |||||||

| Sobha | 30,000 | 1,20,000 | Plant and Machinery | 45,000 | ||||

| Land and Building | 48,000 | |||||||

| 2,64,000 | 2,64,000 | |||||||

The firm was dissolved on the date given above. The following transactions took place:

(a) Rita took 25% of the Stock at a discount of 20% in settlement of her loan.

(b) Book Debts realised ₹ 54,000; balance of the Stock was sold at a profit of 30% on cost.

(c) Sundry Creditors were paid out at a discount of 10%. Bills Payable were paid in full .

(d) Plant and Machinery realised ₹ 75,000. Land and Building ₹ 1,20,000.

(e) Rita took the goodwill of the firm at a value of ₹ 30,000.

(f) An unrecorded asset of ₹ 6,900 was handed over to an unrecorded liability of ₹ 6,000 in full settlement.

(g) Realisation expenses were ₹ 5,250.

Show Realisation Account, Partners’ Capital Accounts and Bank Account in the books of the firm.

ANSWER:

Question 36:

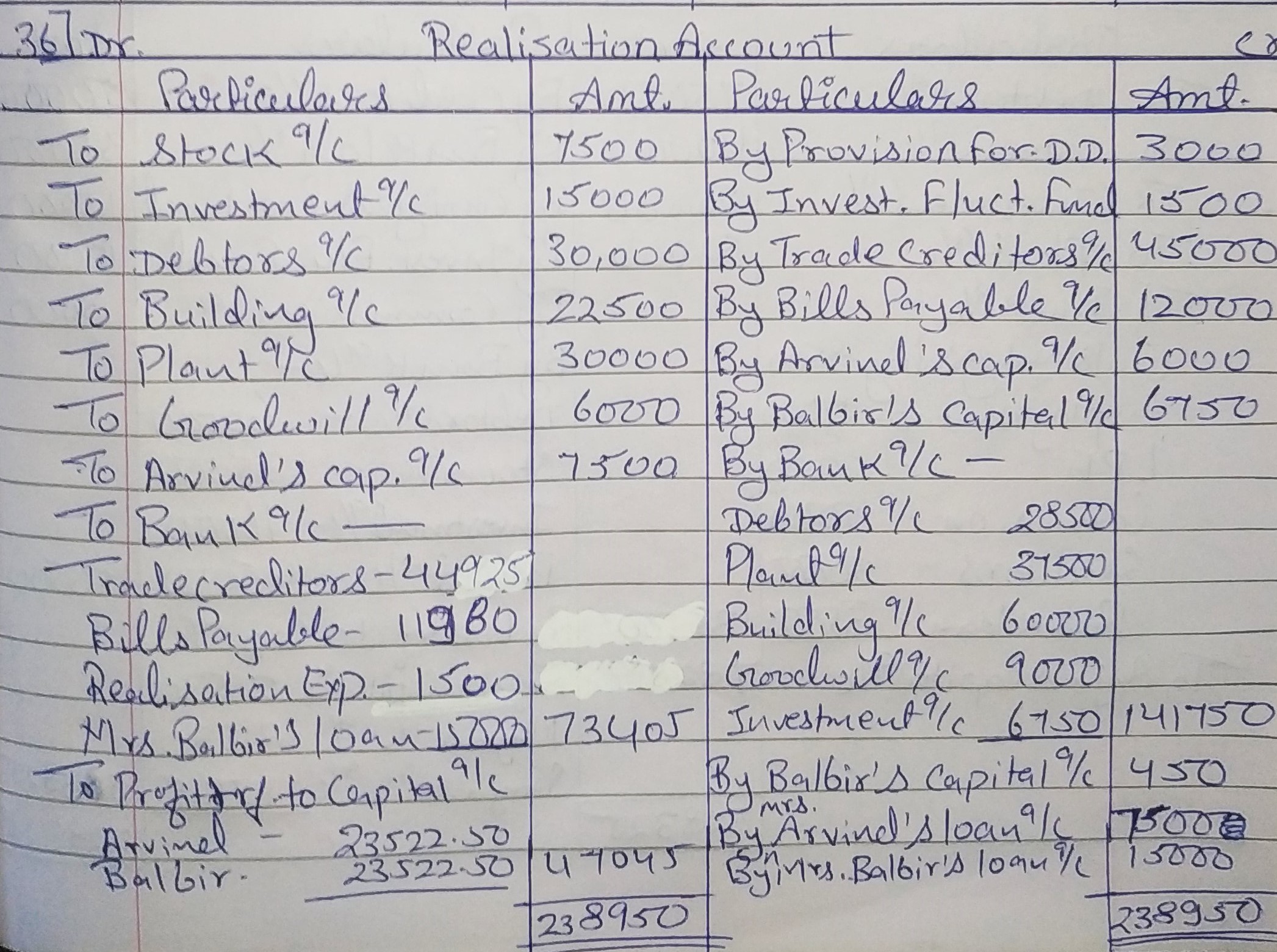

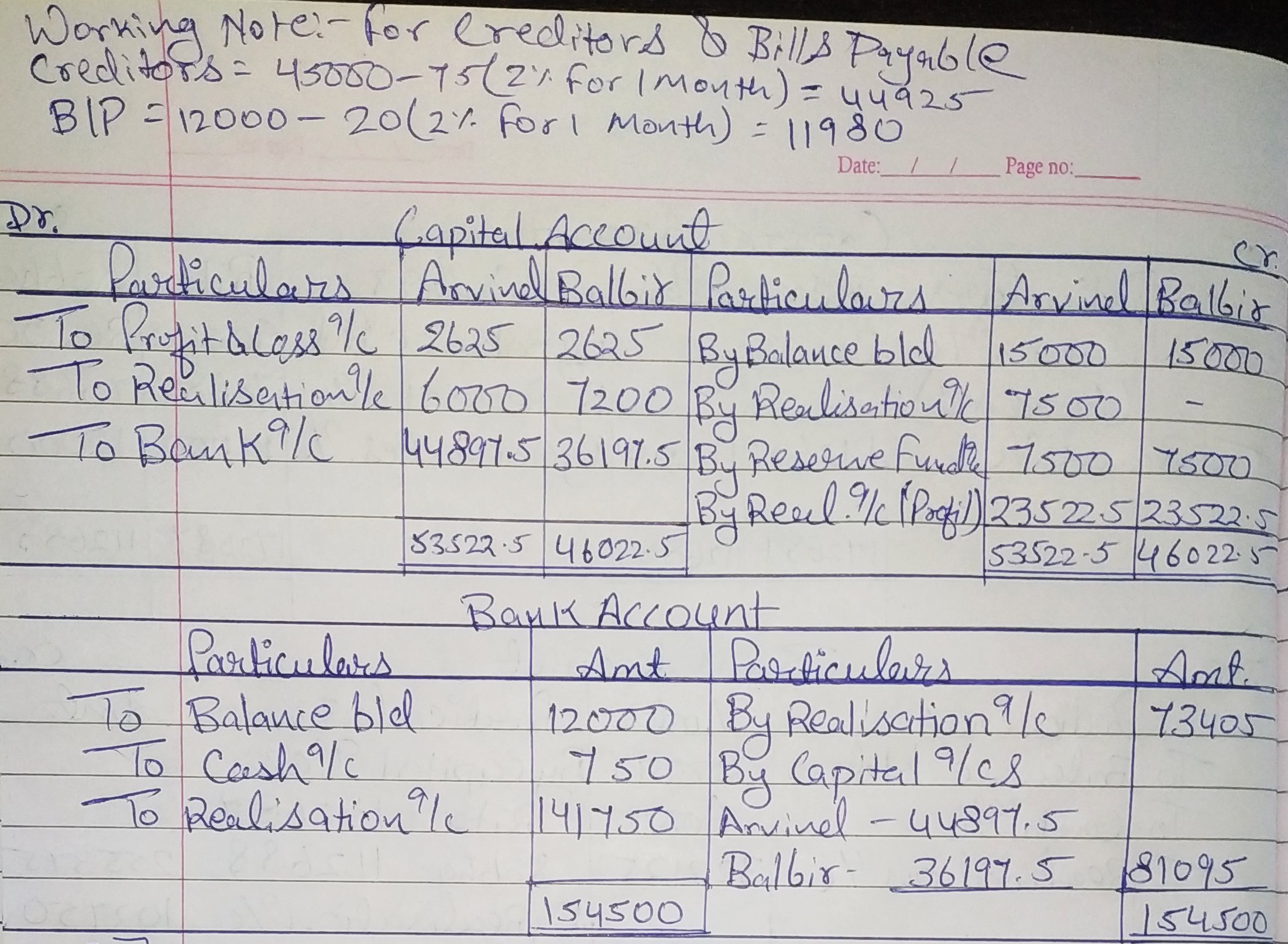

Following is the Balance Sheet of Arvind and Balbir as at 31st March, 2019:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

| Trade Creditors | 45,000 | Cash | 750 | ||

| Bills Payable | 12,000 | Bank | 12,000 | ||

| Mrs. Arvind’s Loan | 7,500 | Stock | 7,500 | ||

| Mrs. Balbir’s Loan | 15,000 | Investments | 15,000 | ||

| Reserve Fund | 15,000 | Book Debts | 30,000 |

| |

| Investments Fluctuation Reserve | 1,500 | Less: Provision for Doubtful Debts | 3,000 | 27,000 | |

| Capital A/cs: | Building | 22,500 | |||

| Arvind | 15,000 |

| Plant | 30,000 | |

| Balbir | 15,000 | 30,000 | Goodwill | 6,000 | |

|

| Profit and Loss A/c | 5,250 | ||

1,26,000 | 1,26,000 | ||||

|

| ||||

The firm was dissolved on the above date under the following arrangement:

(a) Arvind promised to pay off Mrs. Arvind’s Loan and took Stock at ₹ 6,000.

(b) Balbir took half the Investments @ 10% discount.

(c) Book Debts realised ₹ 28,500.

(d) Trade Creditors and Bills Payable were due on average basis of one month after 31st March, but were paid immediately on 31st March @ 2% discount per annum.

(e) Plant realised ₹ 37,500; Building ₹ 60,000; Goodwill ₹ 9,000 and remaining Investments ₹ 6,750.

(f) An old typewriter, written off completely from the firm’s books, now estimated to realise ₹ 450. It was taken by Balbir at this estimated price.

(g) Realisation expenses were ₹ 1,500.

Show Realisation Account, Capital Accounts of Partners and Bank Account.

ANSWER:

Question 37:

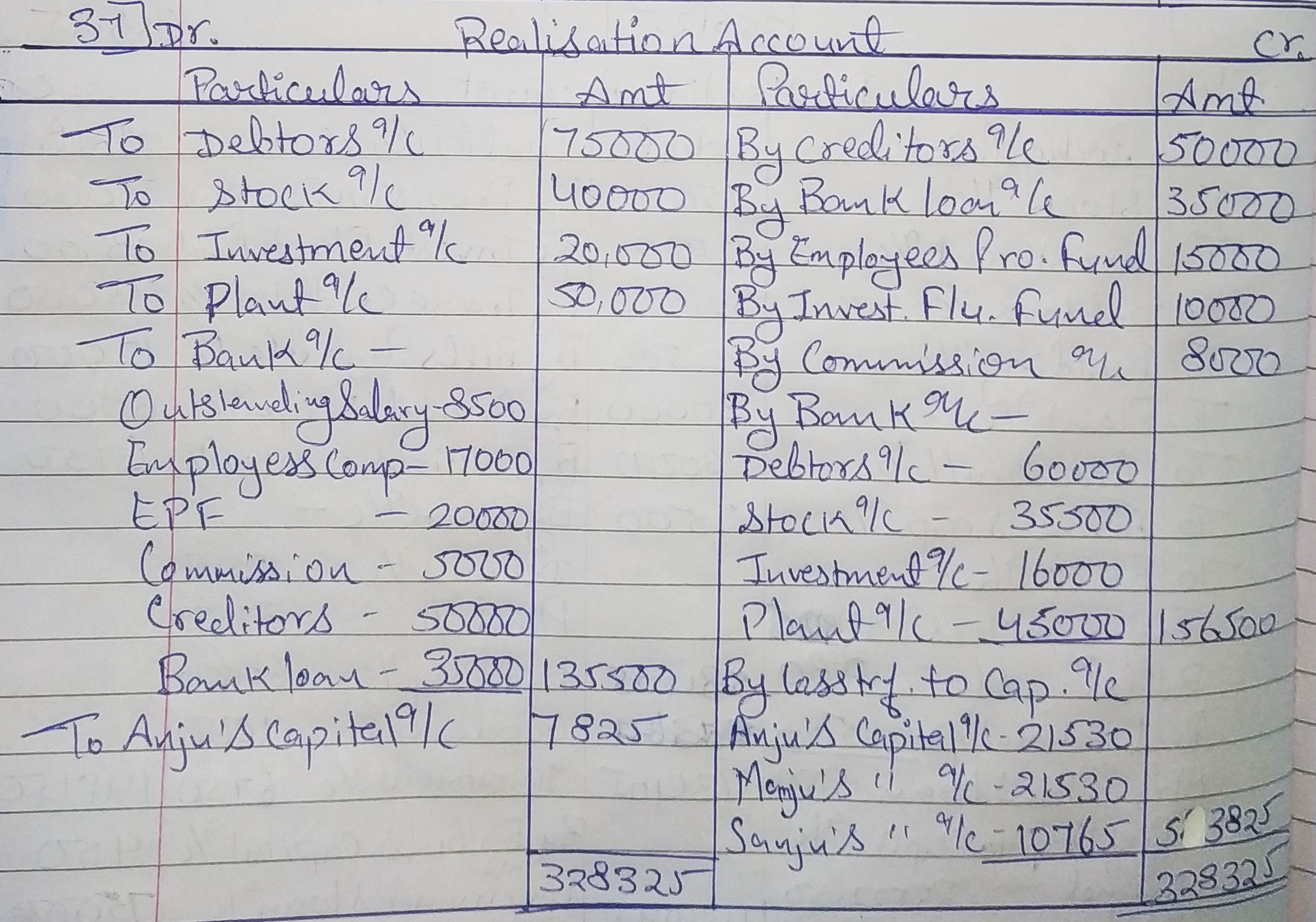

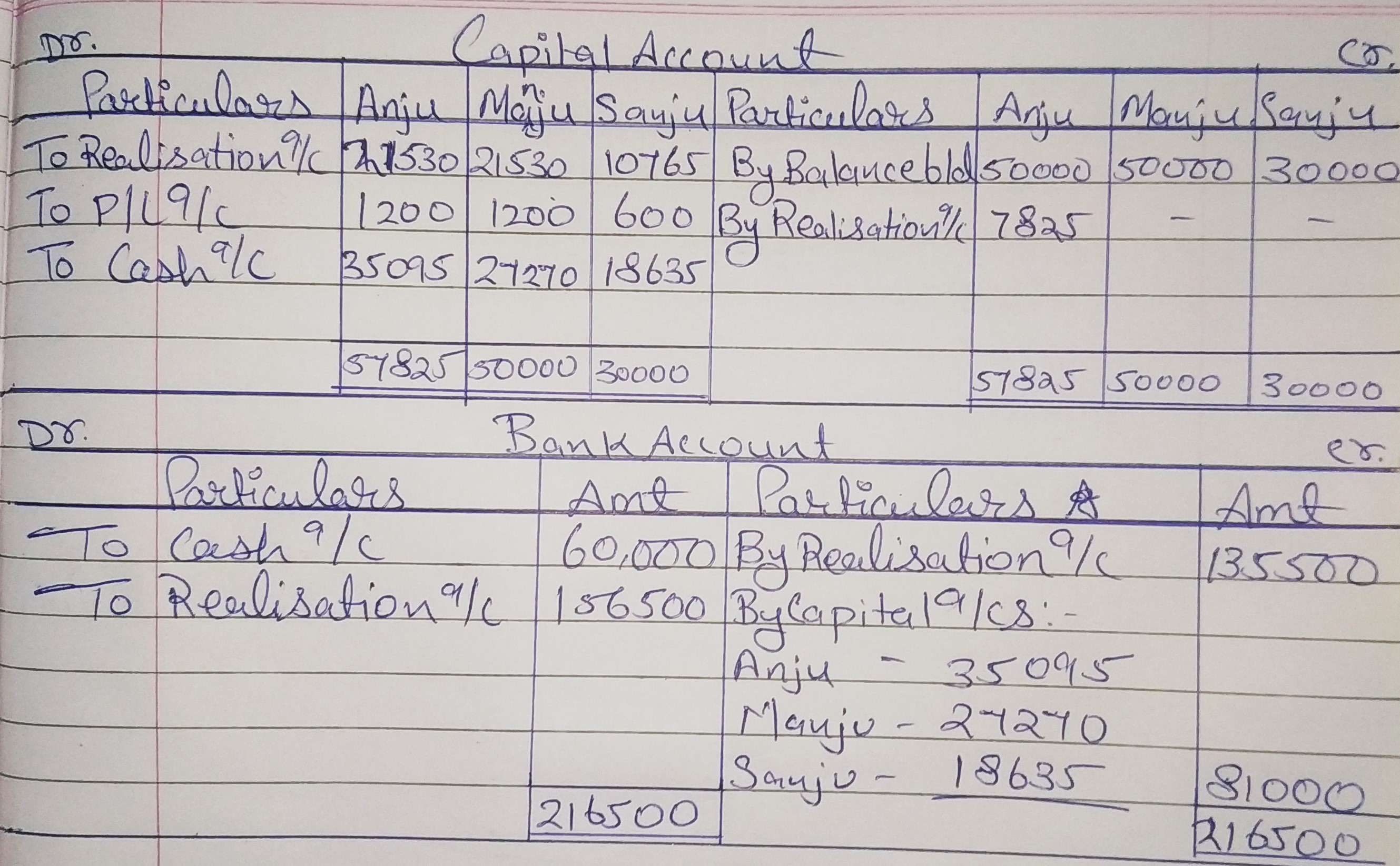

Anju, Manju and Sanju were partners in a firm sharing profits in the ratio of 2 : 2 : 1. On 31st March, 2019, their Balance Sheet was:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |

| Creditors | 50,000 | Cash | 60,000 | |

| Bank Loan | 35,000 | Debtors | 75,000 | |

| Employees’ Provident Fund | 15,000 | Stock | 40,000 | |

| Investments Fluctuation Reserve | 10,000 | Investments | 20,000 | |

| Commission Received in Advance | 8,000 | Plant | 50,000 | |

| Capital A/cs: | Profit and Loss A/c | 3,000 | ||

| Anju | 50,000 | |||

| Manju | 50,000 | |||

Sanju | 30,000 | 1,30,000 | ||

| 2,48,000 | 2,48,000 | |||

On this date, the firm was dissolved. Anju was appointed to realise the assets. Anju was to receive 5% commission on the sale of assets (except cash) and was to bear all expenses of realisation.

Anju realised the assets as follows: Debtors ₹ 60,000; Stock ₹ 35,500; Investments ₹ 16,000; Plant 90% of the book value. Expenses of Realisation amounted to ₹ 7,500. Commission received in advance was returned to customers after deducting ₹ 3,000.

Firm had to pay ₹ 8,500 for Outstanding Salary, not provided for earlier, Compensation paid to employees amounted to ₹ 17,000. This liability was not provided for in the above Balance Sheet. ₹ 20,000 had to be paid for Employees’ Provident Fund.

Prepare Realisation Account, Capital Accounts of Partners and Cash Account.

ANSWER:

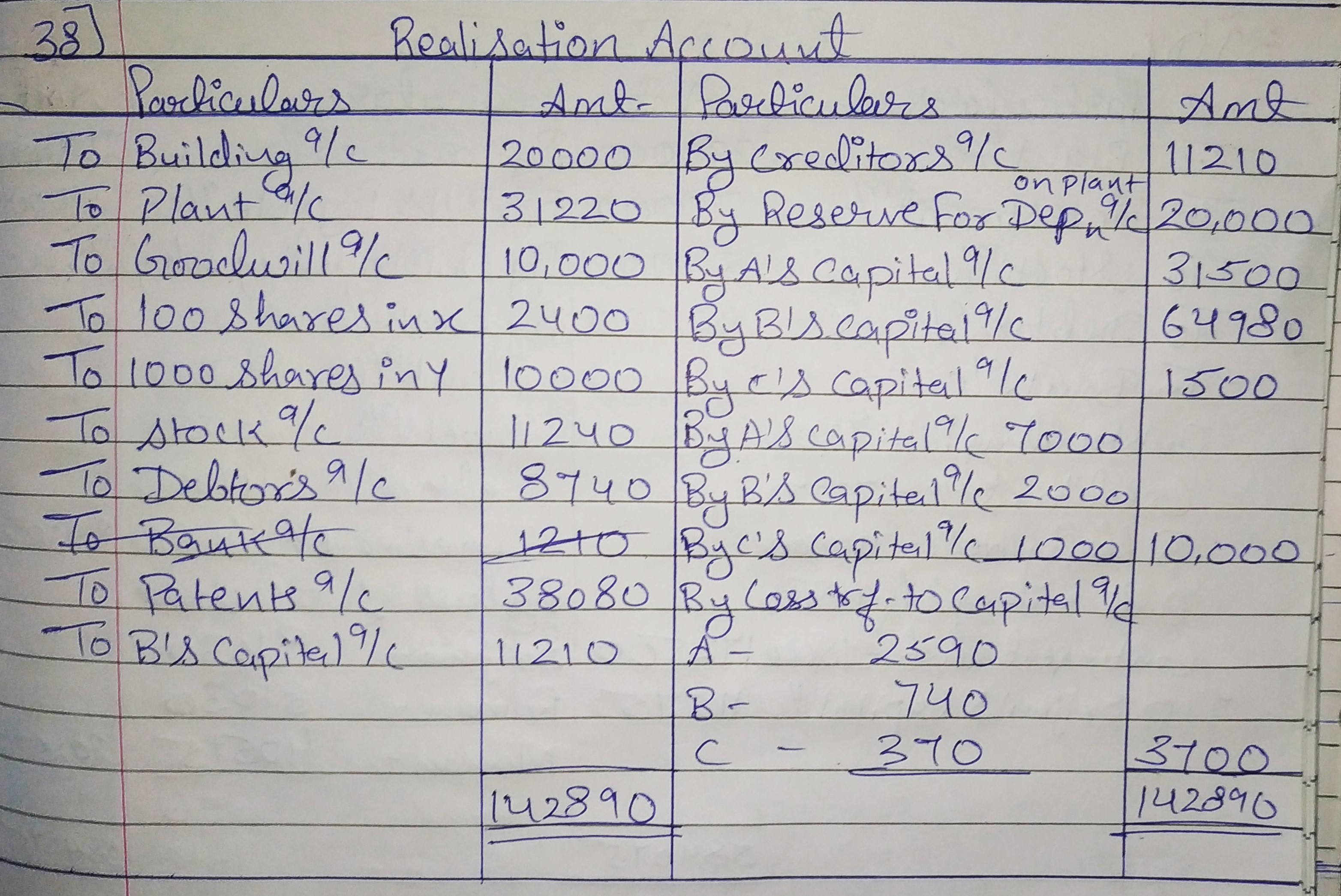

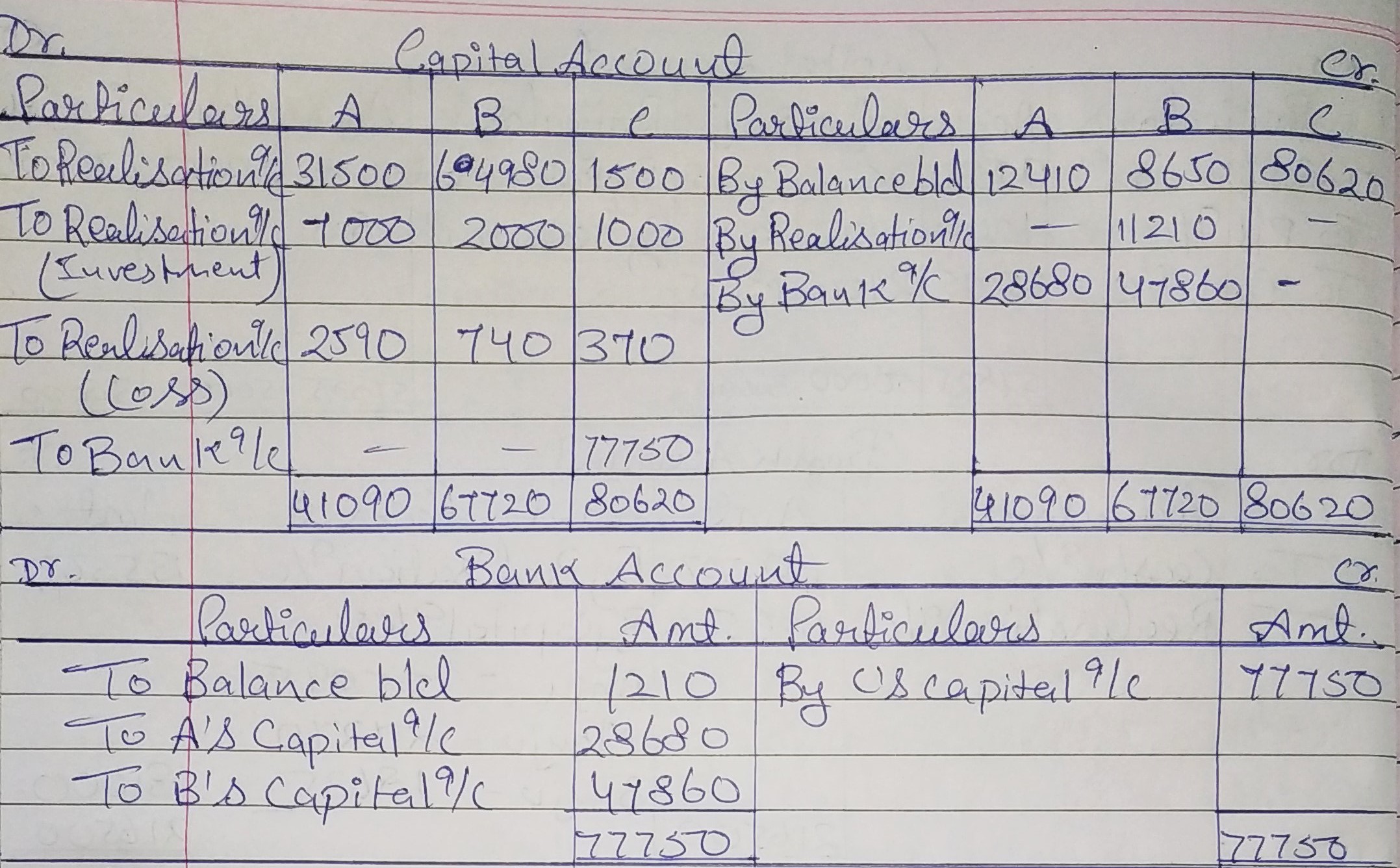

Question 38:

A, B and C were in partnership sharing profits in the ratio of 7 : 2 : 1 and the Balance Sheet of the firm as at 31st March, 2019 was:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |

| Capital A/cs: | Building | 20,000 | ||

| A | 12,410 | Plant | 31,220 | |

| B | 8,650 | Goodwill | 10,000 | |

| C | 80,620 | 1,01,680 | 100 Shares in X Ltd. (At cost) | 2,400 |

| Creditors | 11,210 | 1,000 Shares in Y Ltd. (At cost) | 10,000 | |

| Reserve for Depreciation on Plant | 20,000 | Stock | 11,240 | |

| Debtors | 8,740 | |||

| Bank | 1,210 | |||

| Patents | 38,080 | |||

| 1,32,890 | 1,32,890 | |||

It was agreed to dissolve the partnership as on 31st March, 2019 and the terms of dissolution were−

(a) A to take over the Building at an agreed amount of ₹ 31,500.

(b) B, who was to carry on the business, to take over the Goodwill, Stock and Debtors at book value, the Patents at ₹ 30,000 and Plant at ₹ 5,000. He was also to pay the Creditors.

(c) C to take over shares in X Ltd. at ₹ 15 each.

(d) The shares in Y Ltd. to be divided in the profit-sharing ratio.

Show Ledger Accounts recording the dissolution in the books of the firm.

ANSWER:

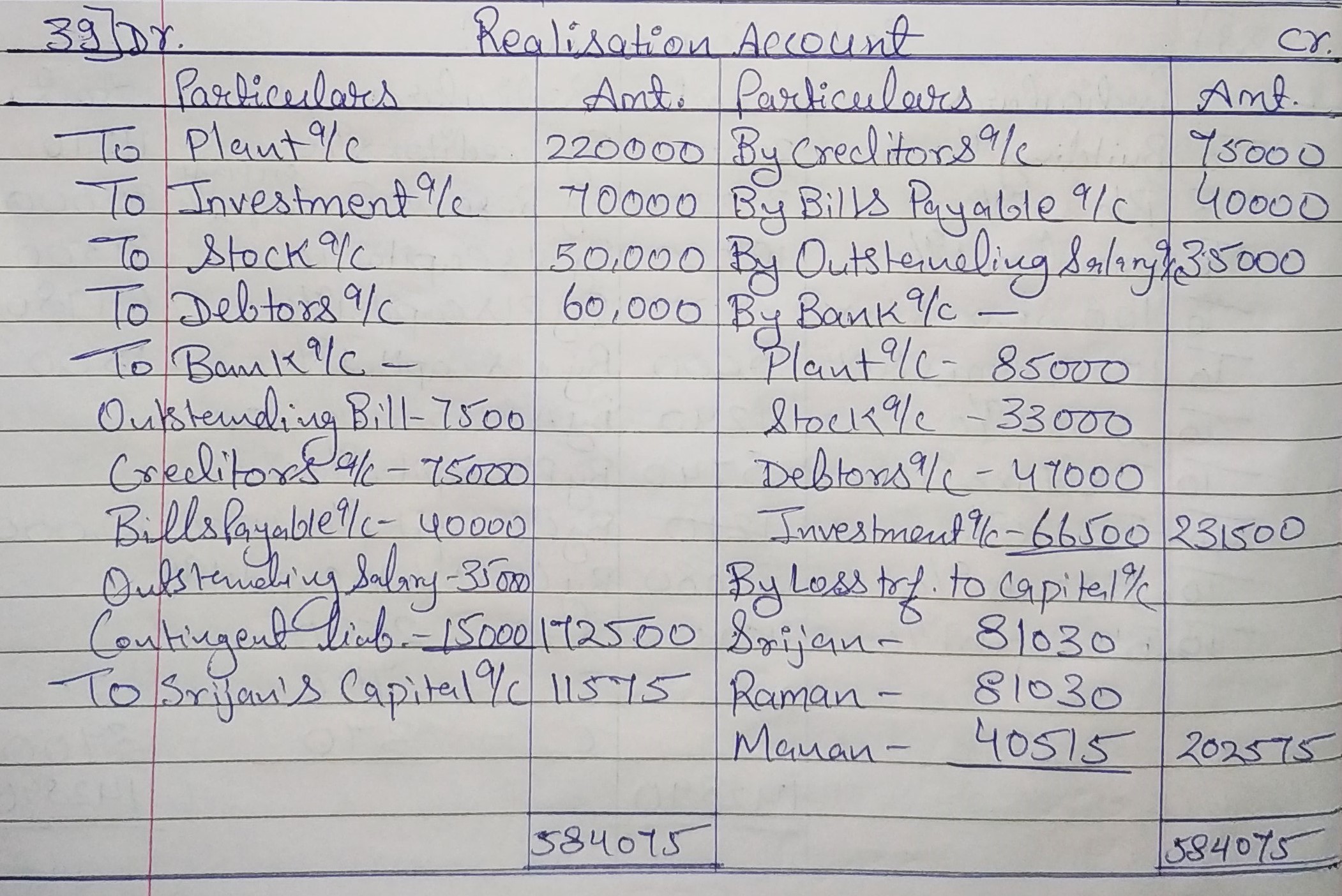

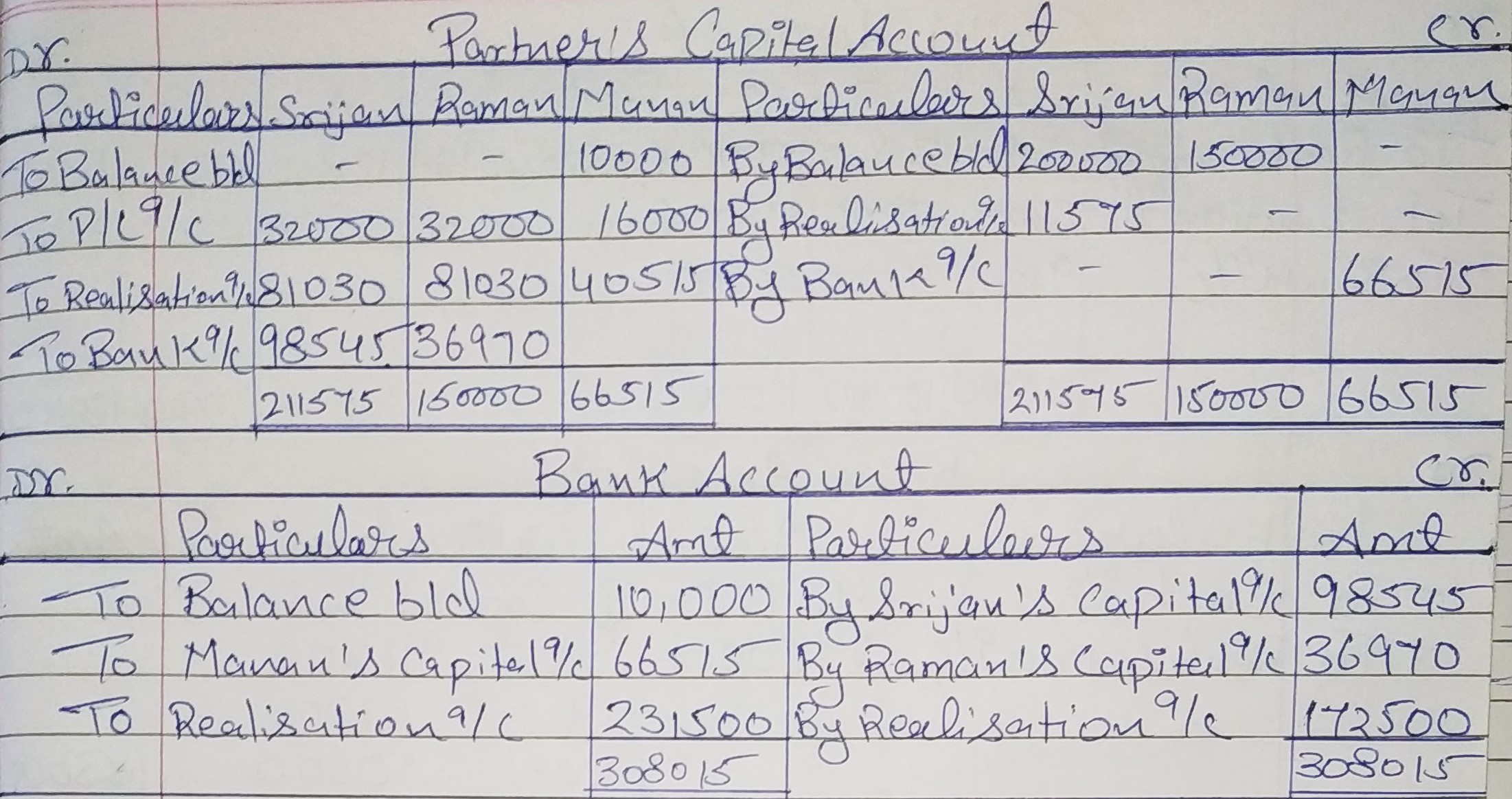

Question 39:

Srijan, Raman and Manan were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. On 31st, March, 2017 their Balance Sheet was as follows:

| Liabilities | Amount (₹) | Assets | Amount (₹) | |

| Capitals: | Capital: Manan | 10,000 | ||

| Srijan | 2,00,000 | Plant | 2,20,000 | |

| Raman | 1,50,000 | 3,50,000 | Investments | 70,000 |

| Creditors | 75,000 | Stock | 50,000 | |

| Bills Payable | 40,000 | Debtors | 60,000 | |

| Outstanding Salary | 35,000 | Bank | 10,000 | |

| Profit and Loss Account | 80,000 | |||

| 5,00,000 | 5,00,000 | |||

On the above date they decided to dissolve the firm.

(a) Srijan was appointed to realise the assets and discharge the liabilities. Srijan was to receive 5% commission on sale of assets (except cash) and was to bear all expenses of realisation.

(b)

| Assets were realised as follows: | ₹ |

| Plant | 85,000 |

| Stock | 33,000 |

| Debtors | 47,000 |

(c) Investments were realised at 95% of the book value.

(d) The firm had to pay ₹ 7,500 for an outstanding repair bill not provided for earlier.

(e) A contingent liabillity in respect of bills receivable, discounted with the bank had also materialised and had to be discharged for ₹ 15,000.

(f) Expenses of realisation amounting to ₹ 3,000 were paid by Srijan.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

Question 40:

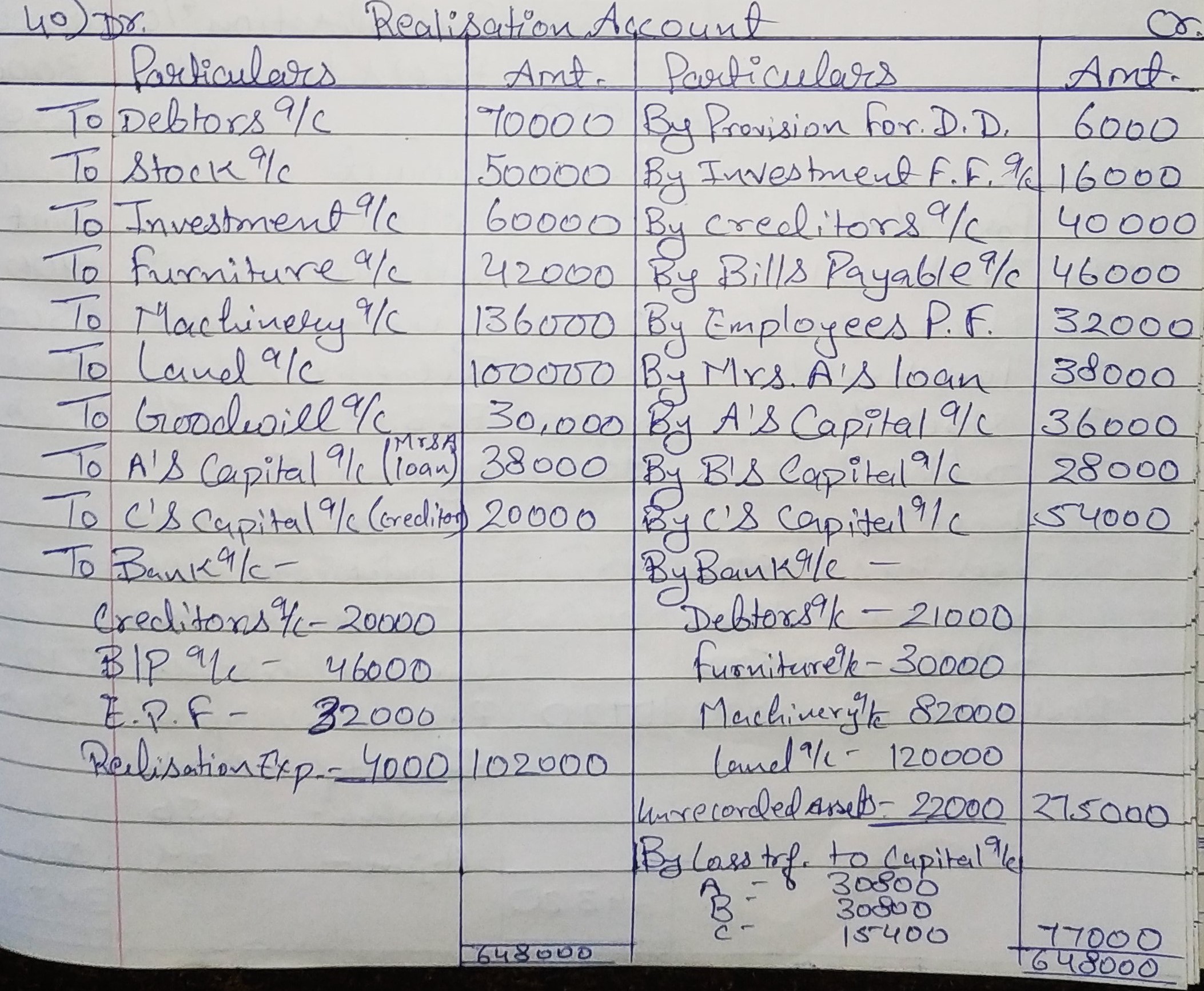

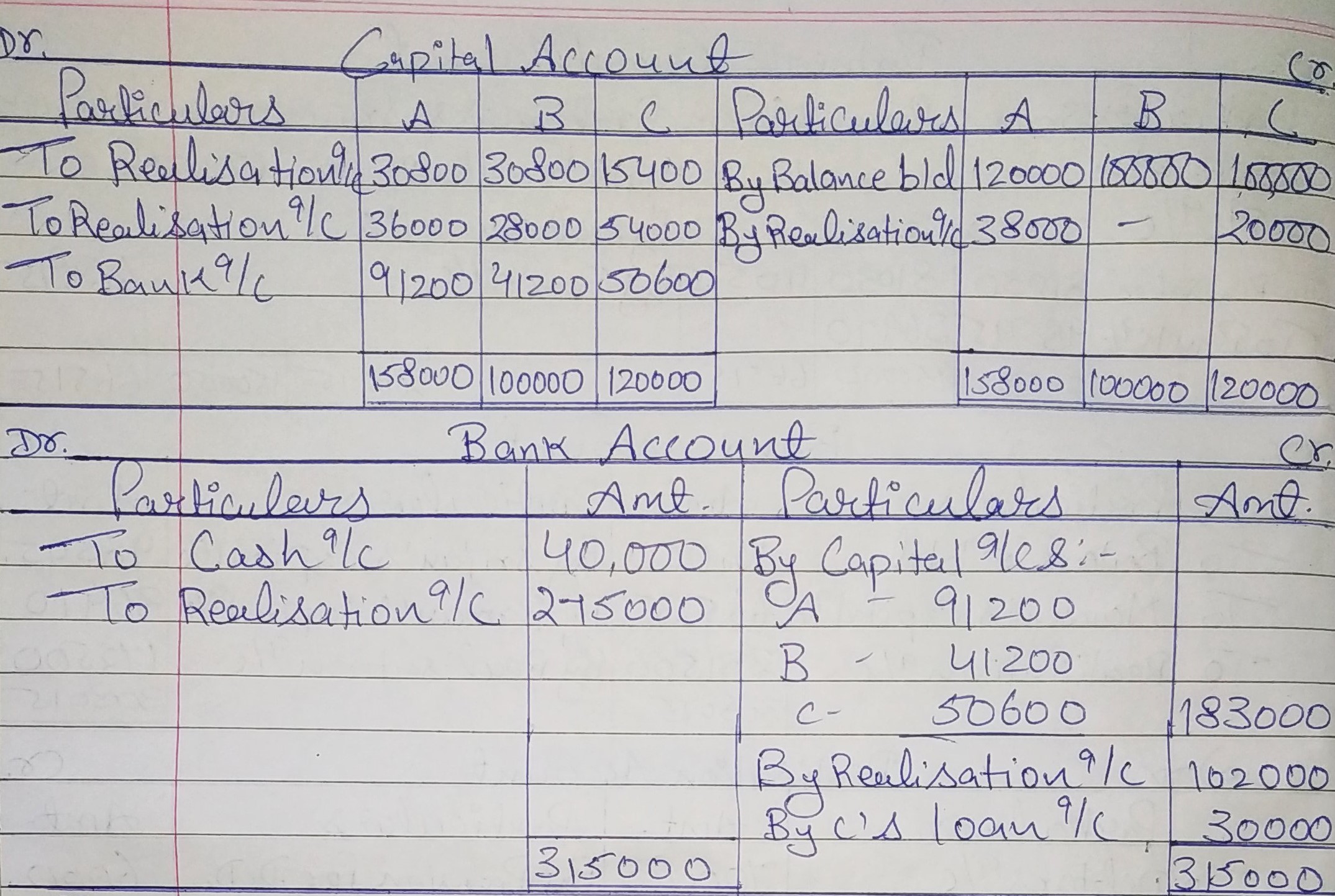

A, B and C were partners sharing profits in the ratio of 2 : 2 : 1. They decided to dissolve their firm on 31st March, 2019 when the Balance Sheet was:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

| Creditors | 40,000 | Cash | 40,000 | ||

| Bills Payable | 46,000 | Debtors | 70,000 | ||

| Employees’ Provident Fund | 32,000 | Less: Provision for Doubtful Debts | 6,000 | 64,000 | |

| Mrs. A’s Loan | 38,000 | Stock | 50,000 | ||

| C’s Loan | 30,000 | Investments | 60,000 | ||

| Investments Fluctuation Reserve | 16,000 | Furniture | 42,000 | ||

| Capitals A/cs: | Machinery | 1,36,000 | |||

| A | 1,20,000 | Land | 1,00,000 | ||

| B | 1,00,000 | Goodwill | 30,000 | ||

| C | 1,00,000 | 3,20,000 | |||

5,22,000 | 5,22,000 | ||||

Following transactions took place:

(a) A took over Stock at ₹ 36,000. He also took over his wife’s loan.

(b) B took over half of Debtors at ₹ 28,000.

(c) C took over Investments at ₹ 54,000 and half of Creditors at their book value.

(d) Remaining Debtors realised 60% of their book value. Furniture sold for ₹ 30,000; Machinery ₹ 82,000 and Land ₹ 1,20,000.

(e) An unrecorded asset was sold for ₹ 22,000.

(f) Realisation expenses amounted to ₹ 4,000.

Prepare necessary Ledger Accounts to close the books of the firm.

ANSWER:

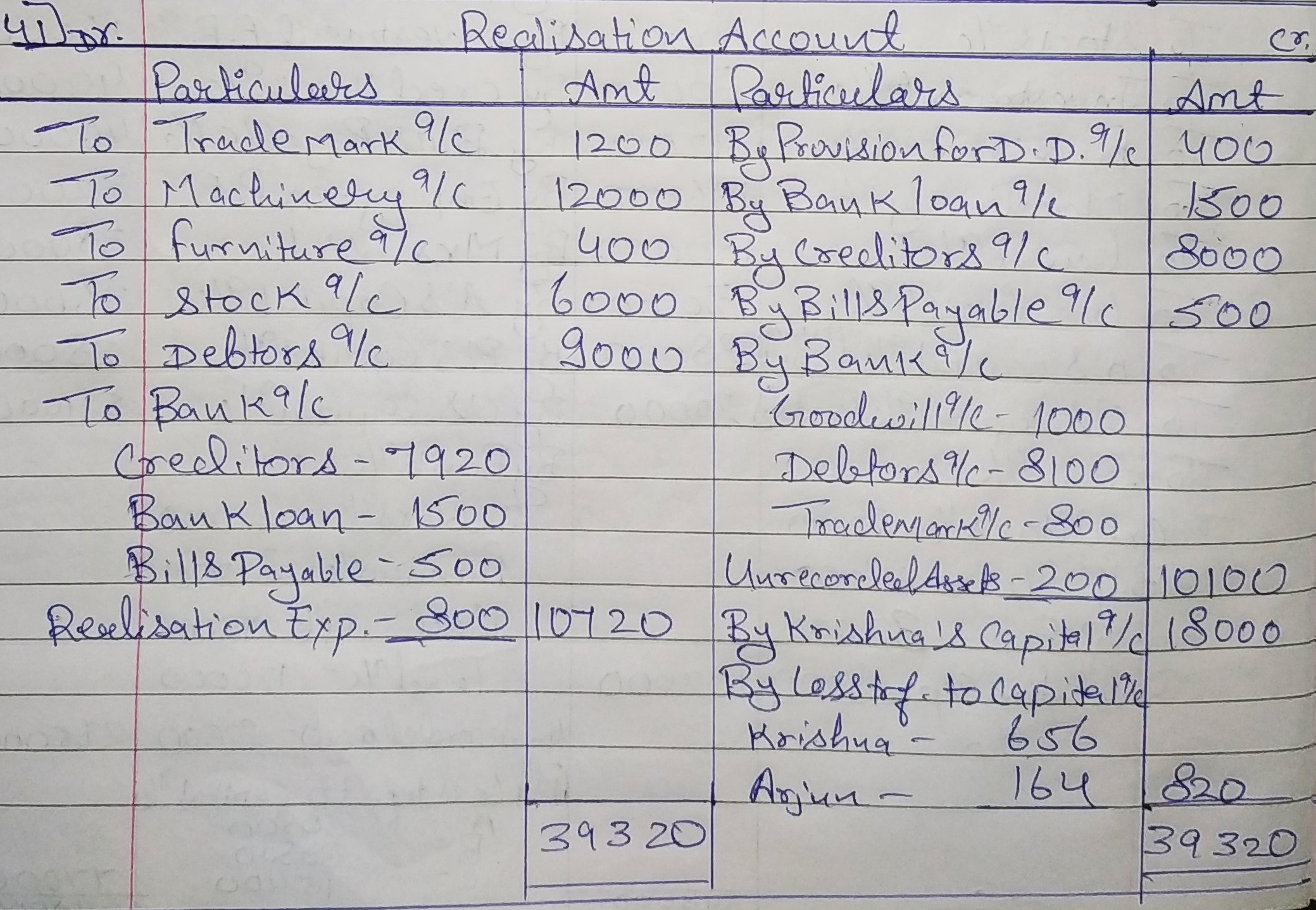

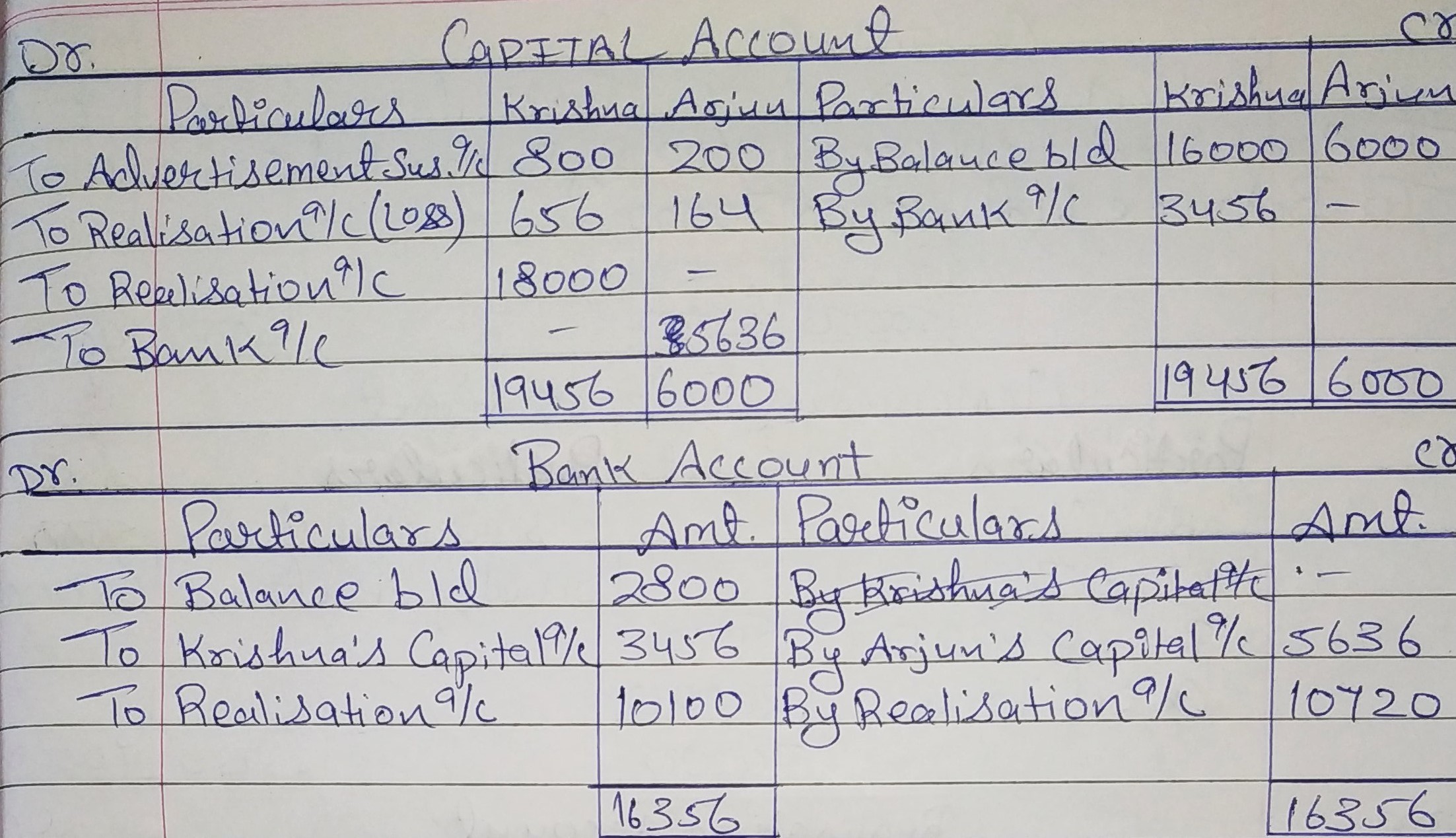

Question 41:

Krishna and Arjun are partners in a firm. They share profits in the ratio of 4 : 1. They decide to dissolve the firm on 31st March, 2019 at which date their Balance Sheet stood as:

Liabilities | Amount (₹) | Assets | Amount (₹) | ||

Bank Loan | 1,500 | Trademarks | 1,200 | ||

Creditors for Goods | 8,000 | Machinery | 12,000 | ||

Bills Payable | 500 | Furniture | 400 | ||

Capital A/cs: | Stock | 6,000 | |||

Krishna | 16,000 | Debtors | 9,000 | ||

Arjun | 6,000 | 22,000 | Less: Provision for Bad Debts | 400 | 8,600 |

Cash at Bank | 2,800 | ||||

Advertisement Suspense | 1,000 | ||||

32,000 | 32,000 | ||||

The realisation shows the following results:

(a) Goodwill was sold for ₹ 1,000.

(b) Debtors were realised at book value less 10%.

(c) Trademarks realised ₹ 800.

(d) Machinery and Stock-in-Trade were taken by Krishna for ₹ 14,400 and ₹ 3,600 respectively.

(e) An unrecorded asset estimated at ₹ 500 was sold for ₹ 200.

(f) Creditors for goods were settled at a discount of ₹ 80. The expenses on realisation were ₹ 800.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

ANSWER:

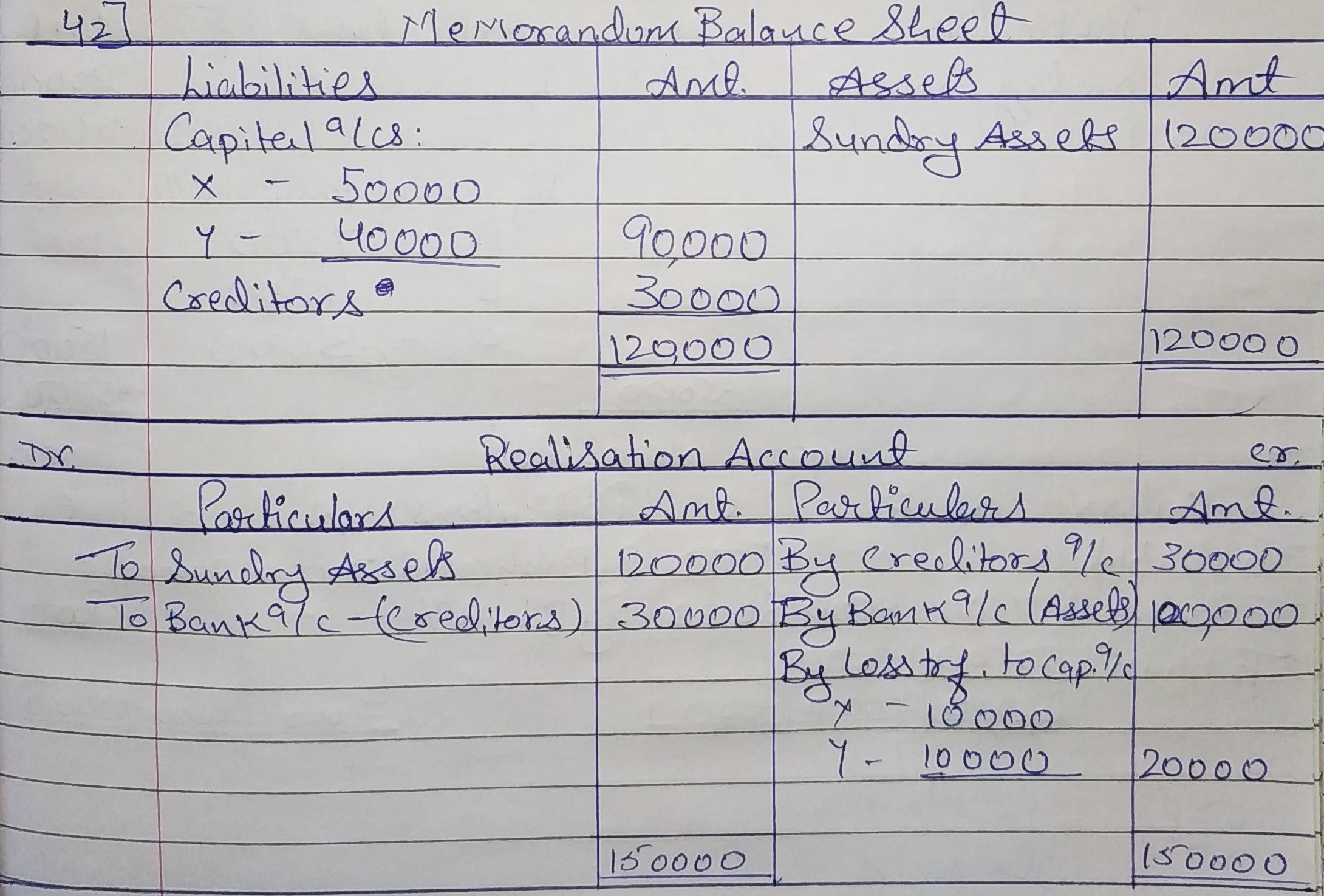

Preparation of Memorandum Balance Sheet

Question 42:

There are two partners X and Y in a firm and their capitals are ₹ 50,000 and ₹ 40,000. The creditors are ₹ 30,000. The assets of the firm realise ₹ 1,00,000. How much will X and Y receive?

ANSWER:

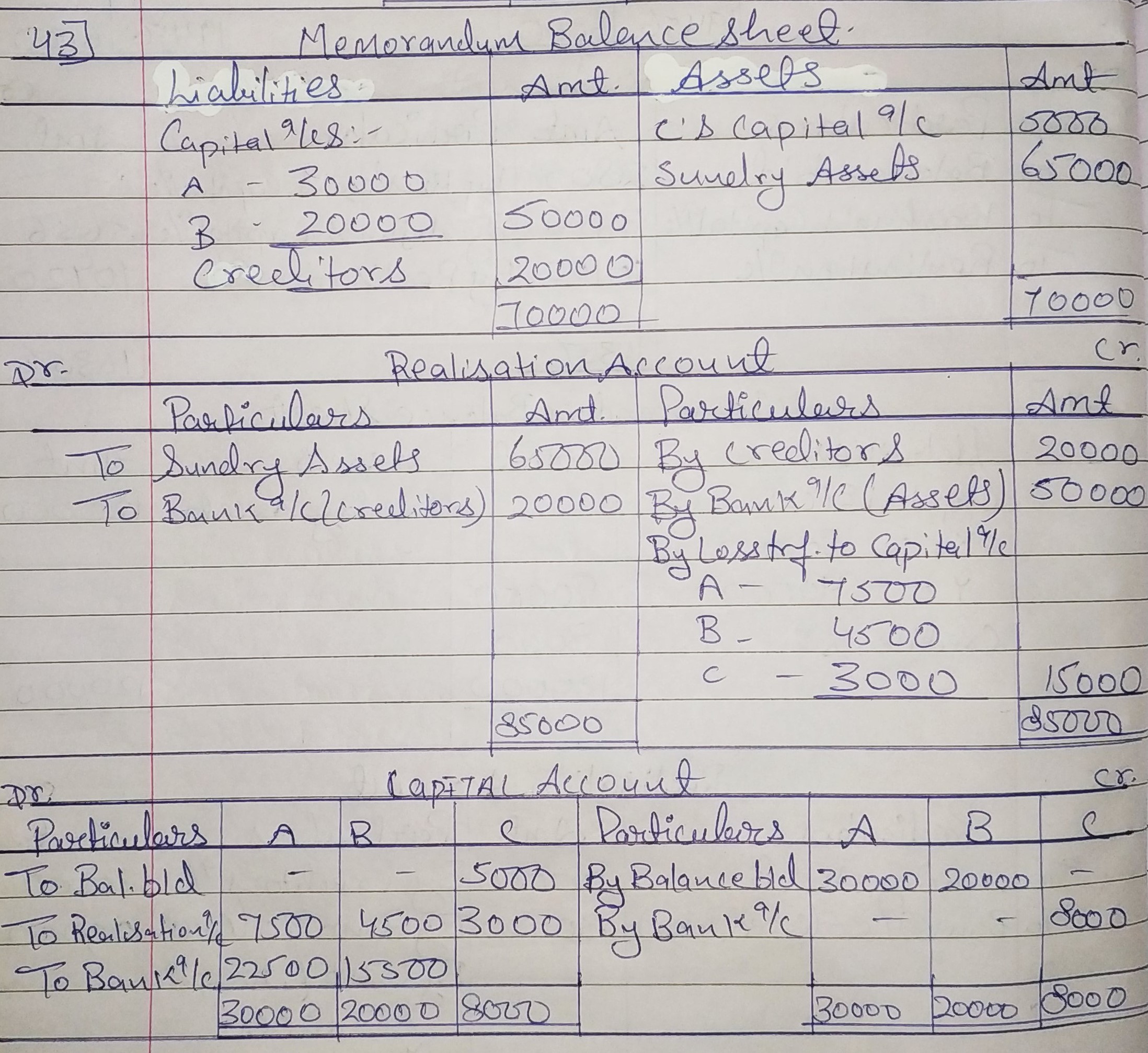

Question 43:

A, B and C were partners sharing profits in the ratio of 5 : 3 : 2. On 31st March, 2019, A‘s Capital and B‘s Capital were ₹ 30,000 and ₹ 20,000 respectively but C owed ₹ 5,000 to the firm. The liabilities were ₹ 20,000. The assets of the firm realised ₹ 50,000.

Prepare Realisation Account, Partner’s Capital Accounts and Bank Account.

ANSWER:

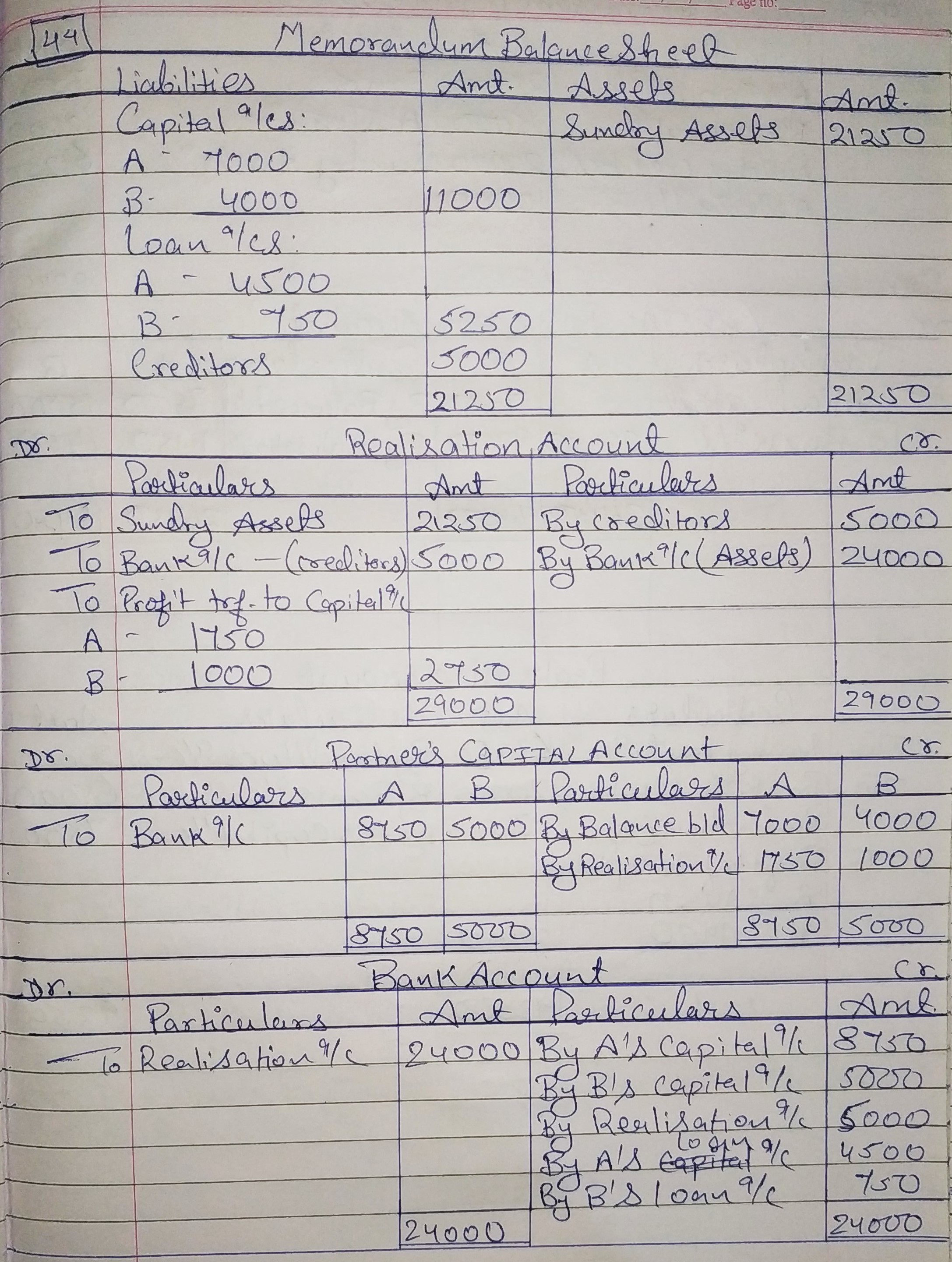

Question 44:

A and B were partners sharing profits and losses as to 7/11th to A and 4/11th to B. They dissolved the partnership on 30th May, 2018. As on that date their capitals were: A ₹ 7,000 and B ₹ 4,000. There were also due on Loan A/c to A ₹ 4,500 and to B ₹ 750. The other liabilities amounted to ₹ 5,000. The assets proved to have been undervalued in the last Balance Sheet and actually realised ₹ 24,000.

Prepare necessary accounts showing the final settlement between partners.

ANSWER:

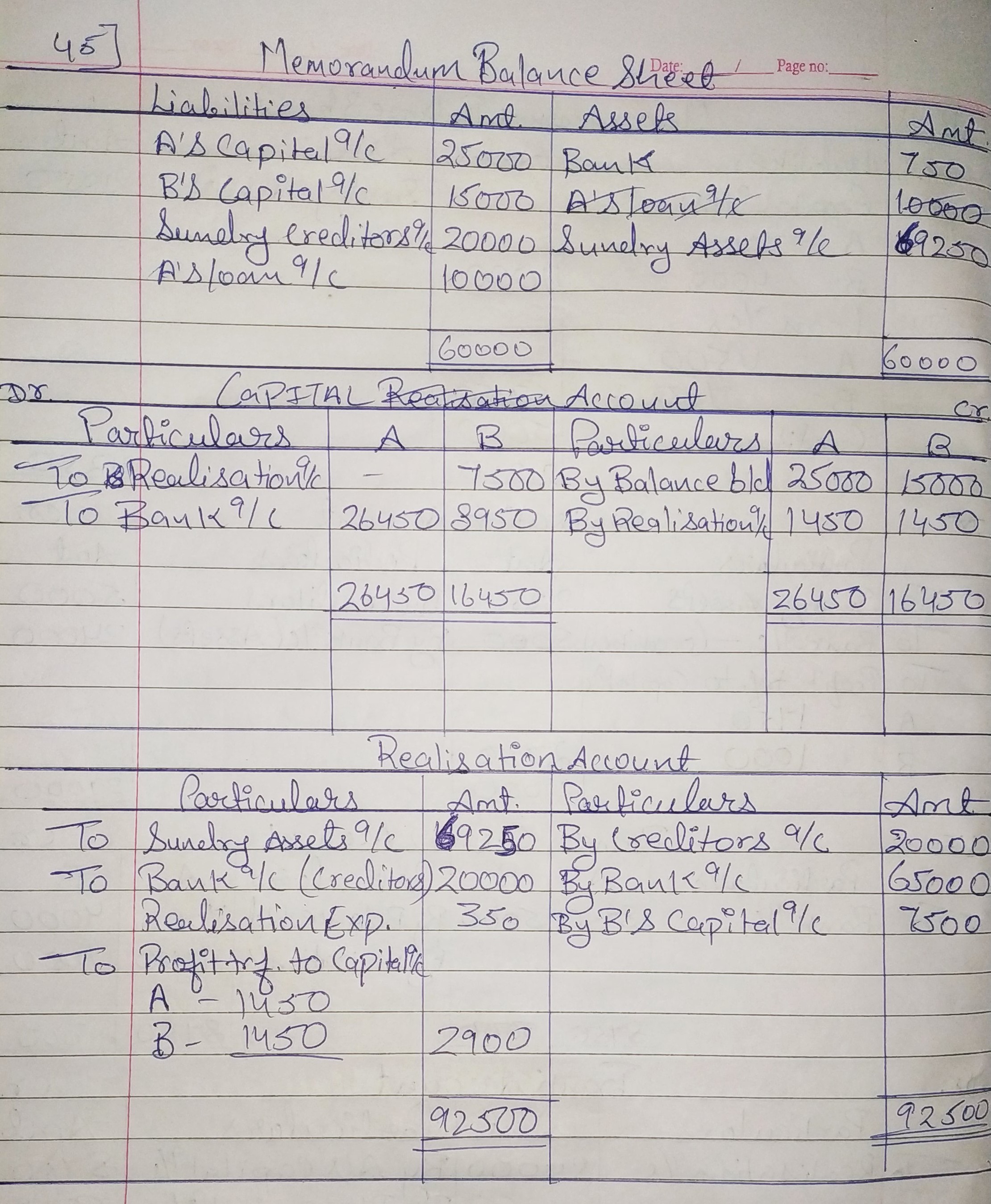

Question 45:

A and B dissolve their partnership. Their position as at 31st March, 2019 was:

| Particulars | ₹ |

| A‘s Capital | 25,000 |

| B‘s Capital | 15,000 |

| Sundry Creditors | 20,000 |

| Cash in Hand and at Bank | 750 |

The balance of A’s Loan Account to the firm stood at ₹ 10,000. The realisation expenses amounted to ₹ 350. Stock realised ₹ 20,000 and Debtors ₹ 25,000. B took a machine at the agreed valuation of ₹ 7,500. Other fixed assets realised ₹ 20,000.

You are required to close the books of the firm.

ANSWER

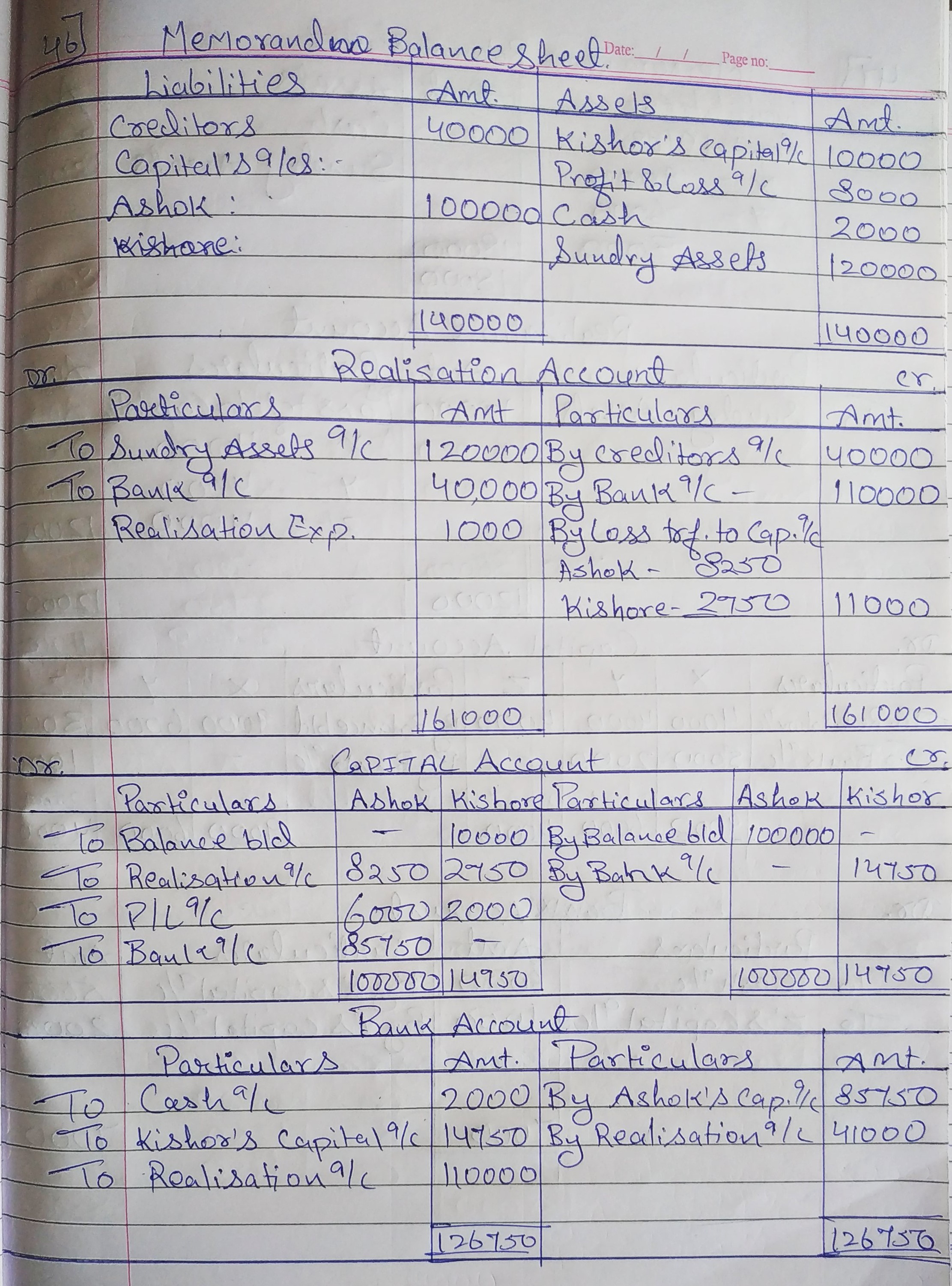

Question 46:

Ashok and Kishore were in partnership sharing profits in the ratio of 3 : 1. They agreed to dissolve the firm. The assets (other than cash of ₹ 2,000) of the firm realised ₹ 1,10,000. The liabilities and other particulars on that date were:

| Creditors | ₹ 40,000 | |

| Ashok’s Capital | ₹ 1,00,000 | |

| Kishore’s Capital | ₹ 10,000 | (Dr. Balance) |

| Profit and Loss A/c | ₹ 8,000 | (Dr. Balance) |

| Realisation Expenses | ₹ 1,000 |

You are required to close the books of the firm.

ANSWER:

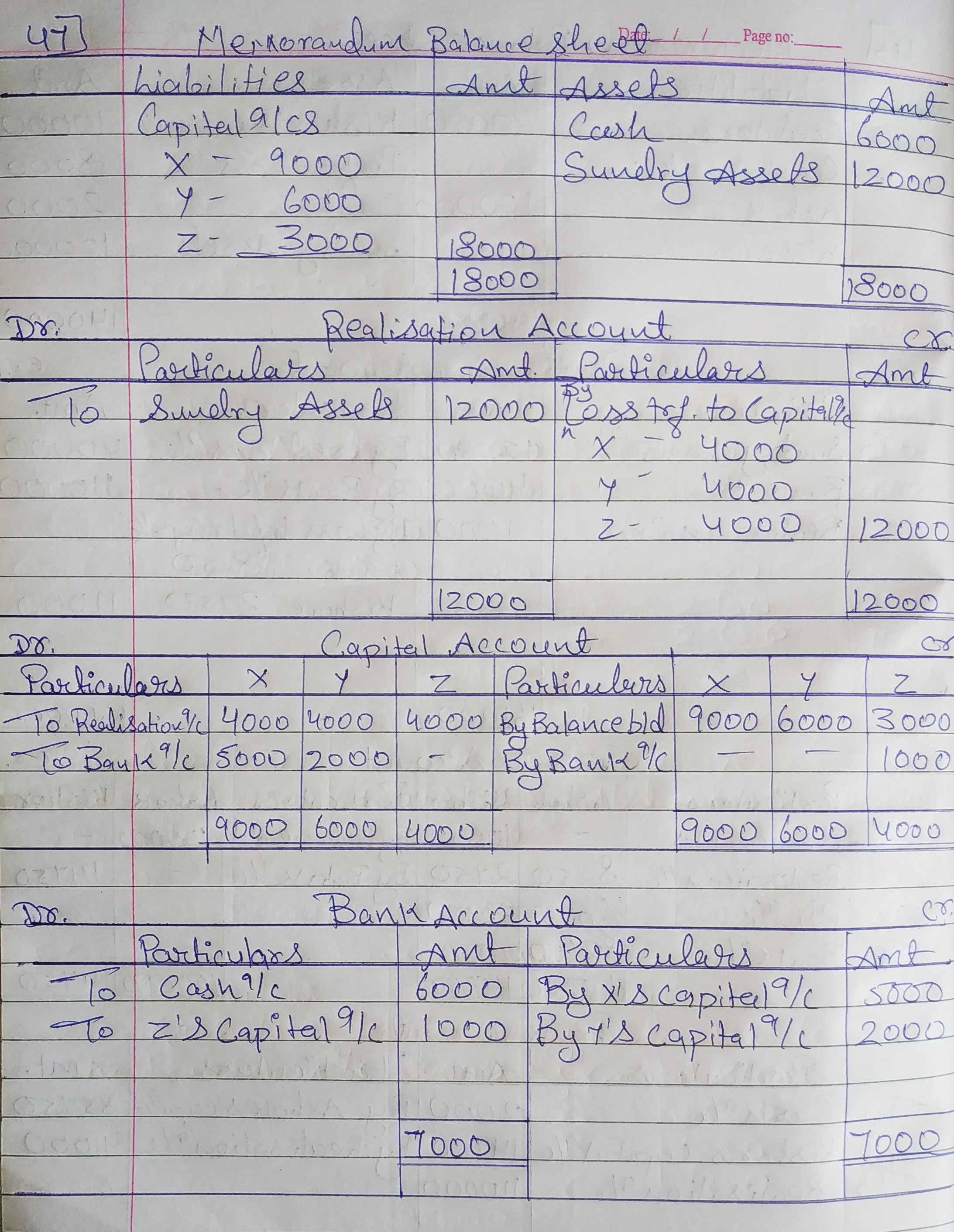

Question 47:

X, Y and Z entered into a partnership and contributed ₹ 9,000; ₹ 6,000 and ₹ 3,000 respectively. They agreed to share profits and losses equally. The business lost heavily during the very first year and they decided to dissolve the firm. After realising all assets and paying off liabilities, there remained a cash balance of ₹ 6,000.

Prepare Realisation Account and Partner’s Capital Accounts.

ANSWER:

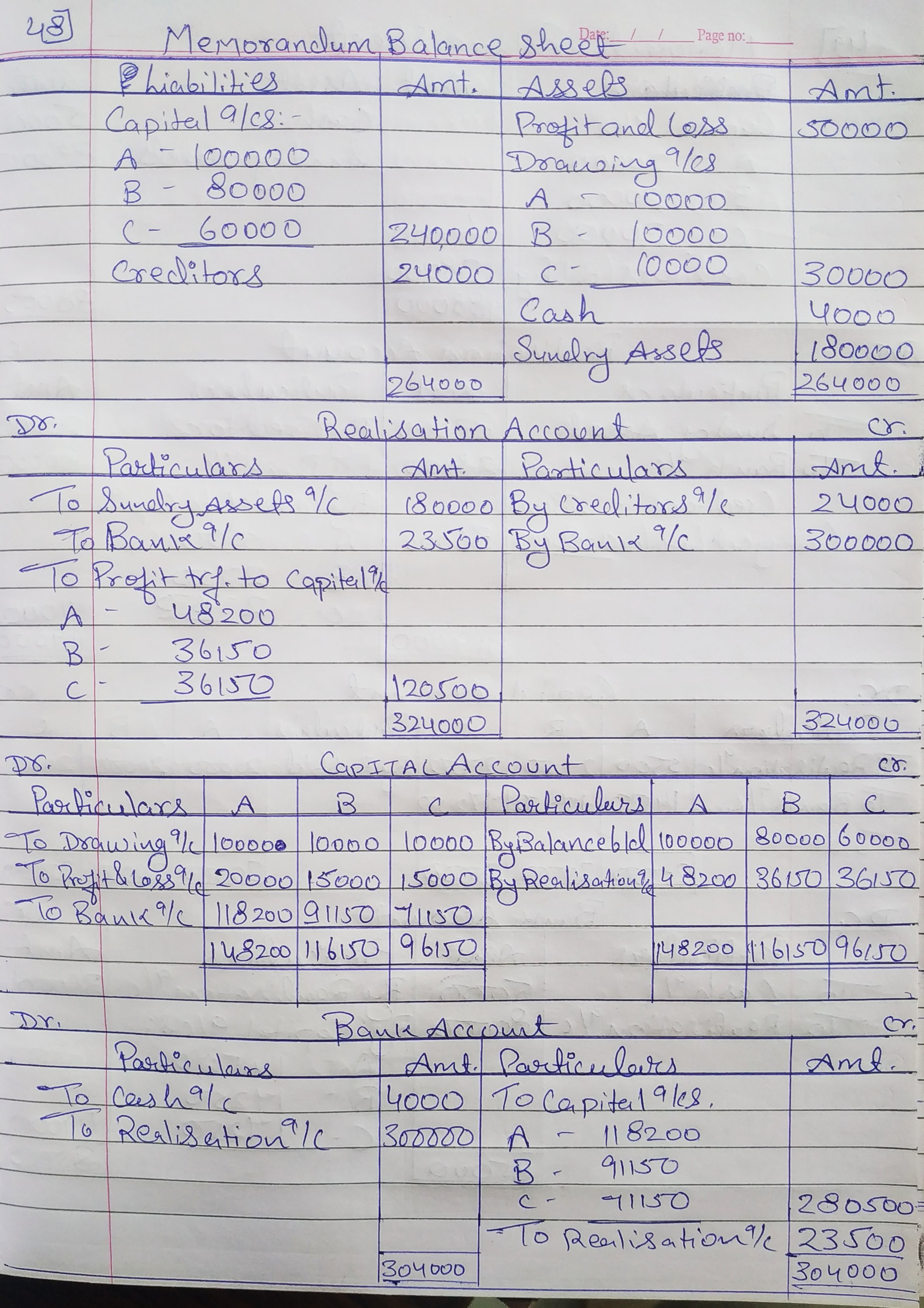

Question 48:

A, B and C started business on 1st April, 2018 with capitals of ₹ 1,00,000; ₹ 80,000 and ₹ 60,000 respectively sharing profits (losses) in the ratio of 4 : 3 : 3. For the year ended 31st March, 2019, the firm suffered a loss of ₹ 50,000. Each of the partners withdrew ₹ 10,000 during the year.

On 31st March, 2019, the firm was dissolved, the creditors of the firm stood at ₹ 24,000 on that date and Cash in Hand was ₹ 4,000. The assets realised ₹ 3,00,000 and Creditors were paid ₹ 23,500 in full settlement of their claims.

Prepare Realisation Account and show your workings clearly.

ANSWER:

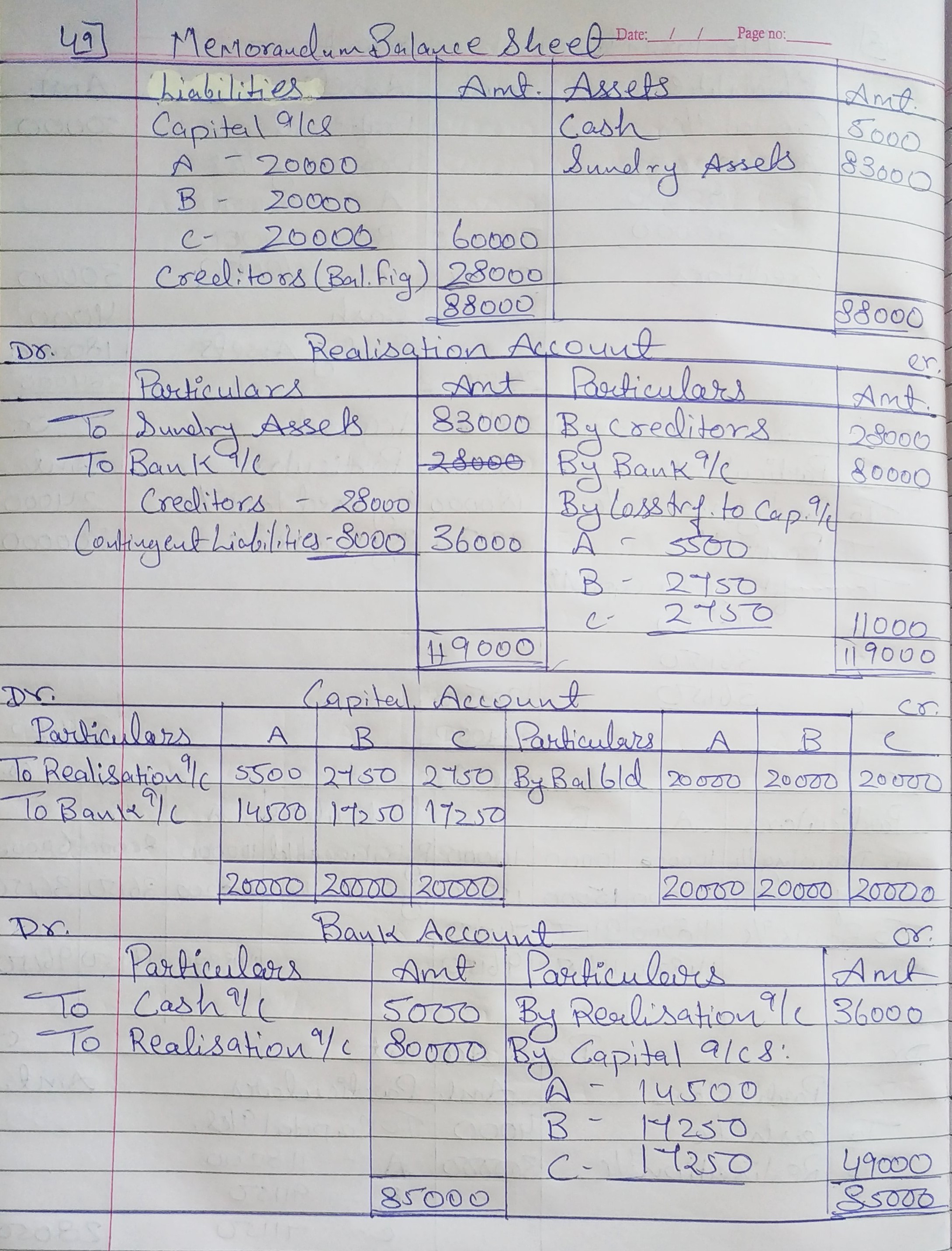

Question 49:

A, B and C were in partnership sharing profits and losses in the ratio of 2 : 1 : 1. They decided to dissolve the partnership. On that date of dissolution, Sundry Assets (including cash ₹ 5,000) amounted to ₹ 88,000, assets realised ₹ 80,000 (including an unrecorded asset which realised ₹ 4,000). A contingent liability on account of bills discounted ₹ 8,000 was paid by the firm. The Capital Accounts of A, B and C showed a balance of ₹ 20,000 each.

Prepare Realisation Account, Partners’ Capital Accounts and Cash Account.

ANSWER:

Question 50:

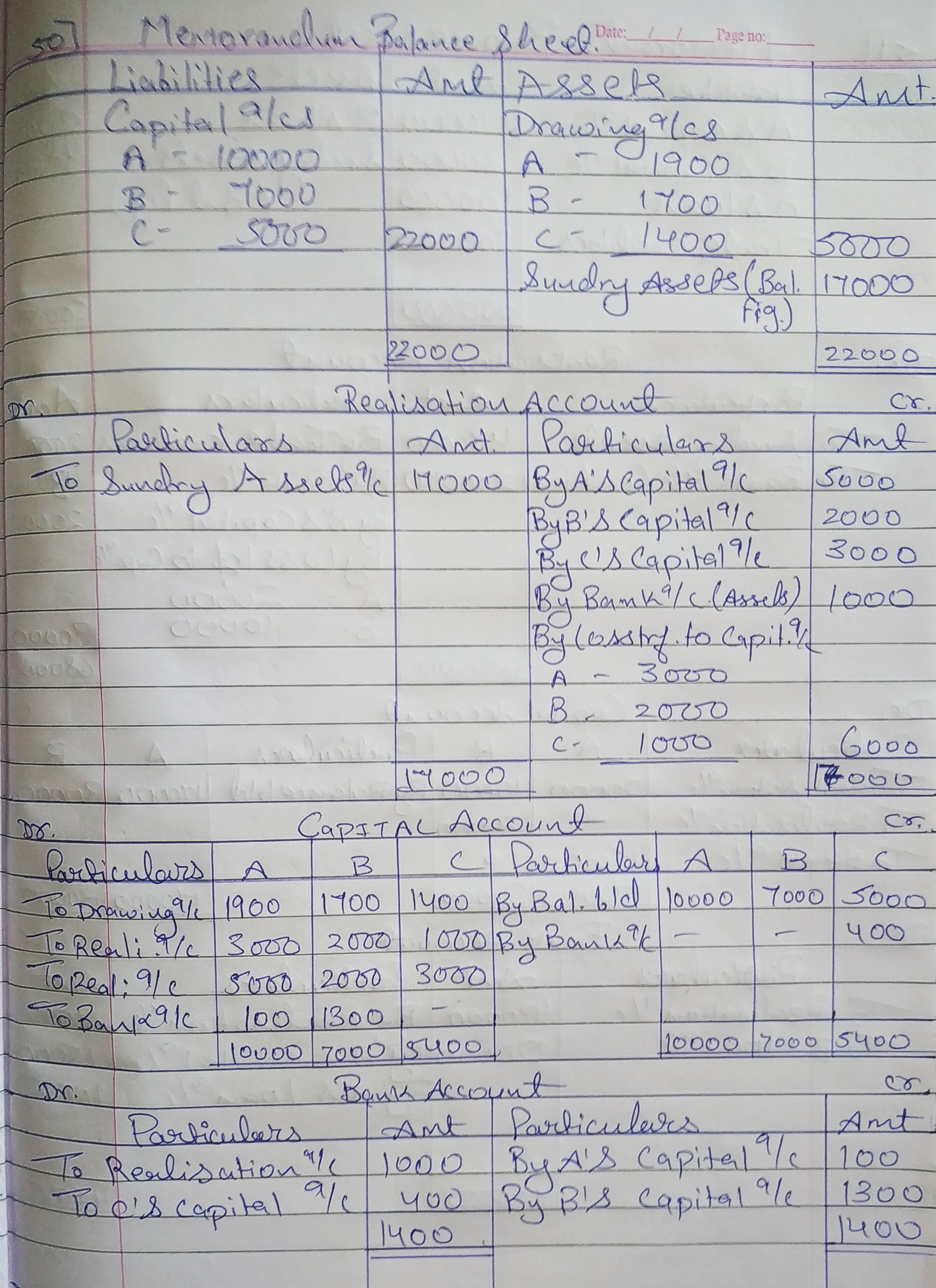

On 1st April, 2018, A, B and C commenced business in partnership sharing profits and losses in proportion of 1/2, 1/3 and 1/6 respectively. They paid into their Bank A/c as their capitals ₹ 22,000; ₹ 10,000 by A, ₹ 7,000 by B and ₹ 5,000 by C. During the year, they drew ₹ 5,000; being ₹ 1,900 by A, ₹ 1,700 by B and ₹ 1,400 by C.

On 31st March, 2019, they dissolved their partnership, A taking up Stock at an agreed valuation of ₹ 5,000, B taking up Furniture at ₹ 2,000 and C taking up Debtors at ₹ 3,000. After paying up their Creditors, there remained a balance of ₹ 1,000 at Bank. Prepare necessary accounts showing the distribution of the cash at the Bank and of the further cash brought in by any partner or partners as the case required.

ANSWER:

Question 51:

The partnership between A and B was dissolved on 31st March, 2019. On that date the respective credits to the capitals were A − ₹ 1,70,000 and B − ₹ 30,000. ₹ 20,000 were owed by B to the firm; ₹ 1,00,000 were owed by the firm to A and ₹ 2,00,000 were due to the Trade Creditors. Profits and losses were shared in the proportions of 2/3 to A, 1/3 to B.

The assets represented by the above stated net liabilities realise ₹ 4,50,000 exclusive of ₹ 20,000 owed by B. The liabilities were settled at book figures. Prepare Realisation Account, Partners’ Capital Accounts and Cash Account showing the distribution to the partners.

ANSWER:

Question 52:

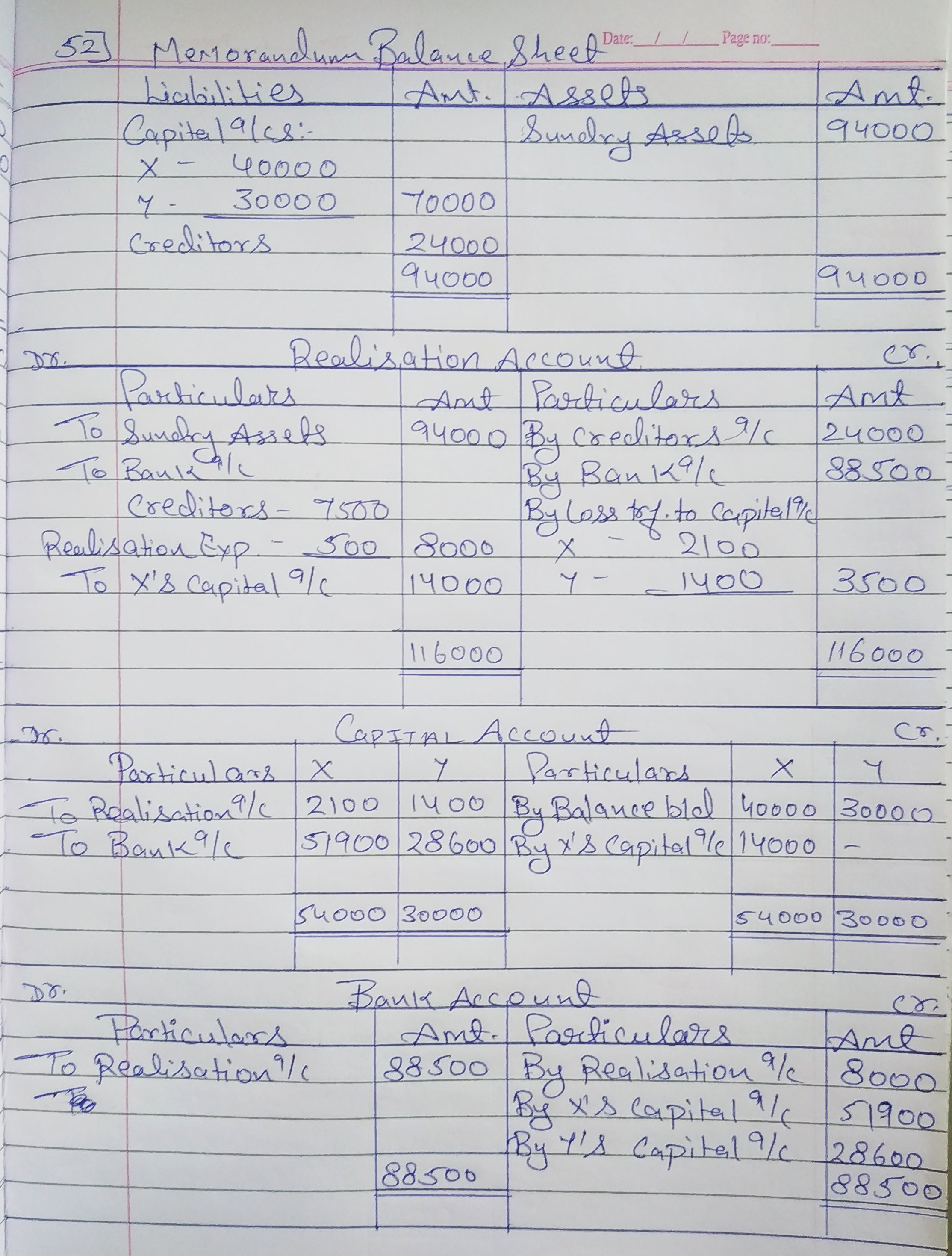

X and Y were partners sharing profits and losses in the ratio of 3 : 2. They decided to dissolve the firm on 31st March, 2019. On that date, their Capitals were X − ₹ 40,000 and Y − ₹ 30,000. Creditors amounted to ₹ 24,000.

Assets were realised for ₹ 88,500. Creditors of ₹ 16,000 were taken over by X at ₹ 14,000. Remaining Creditors were paid at ₹ 7,500. The cost of realisation came to ₹ 500.

Prepare necessary accounts.

ANSWER:

Question 53:

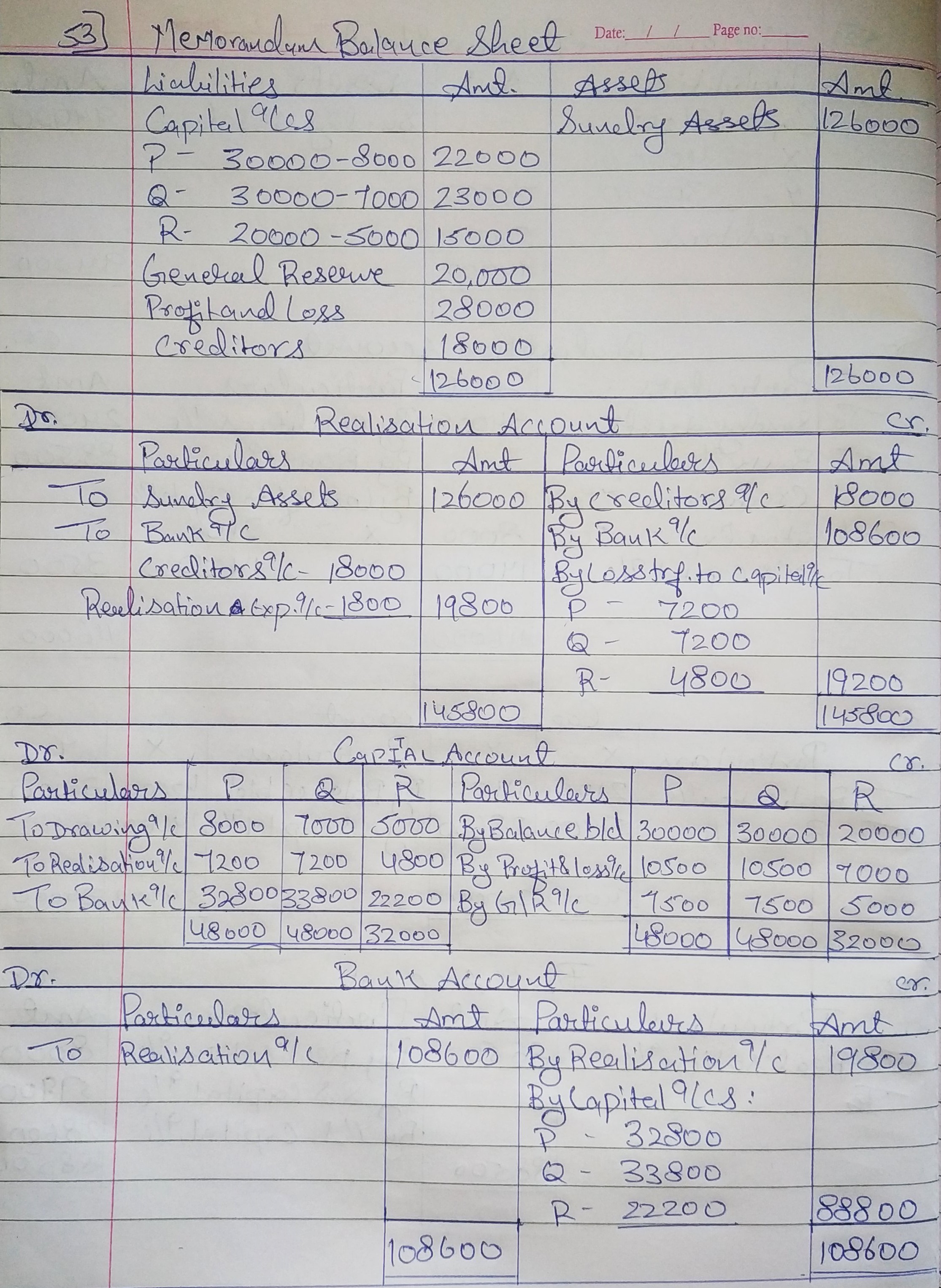

P, Q and R are partners sharing profits and losses in the ratio of 3 : 3 : 2 respectively. Their respective capitals are in their profit-sharing proportions. On 1st April, 2018, the total capital of the firm and the balance of General Reserve are ₹ 80,000 and ₹ 20,000 respectively. During the year 2018-19, the firm made a profit of ₹ 28,000 before charging interest on capital @ 5%. The drawings of the partners are P——₹ 8,000; Q——₹ 7,000; and R——₹ 5,000. On 31st March, 2019, their liabilities were ₹ 18,000.

On this date, they decided to dissolve the firm. The assets realised ₹ 1,08,600 and realisation expenses amounted to ₹ 1,800.

Prepare necessary Ledger Accounts to close the books of the firm.

ANSWER:

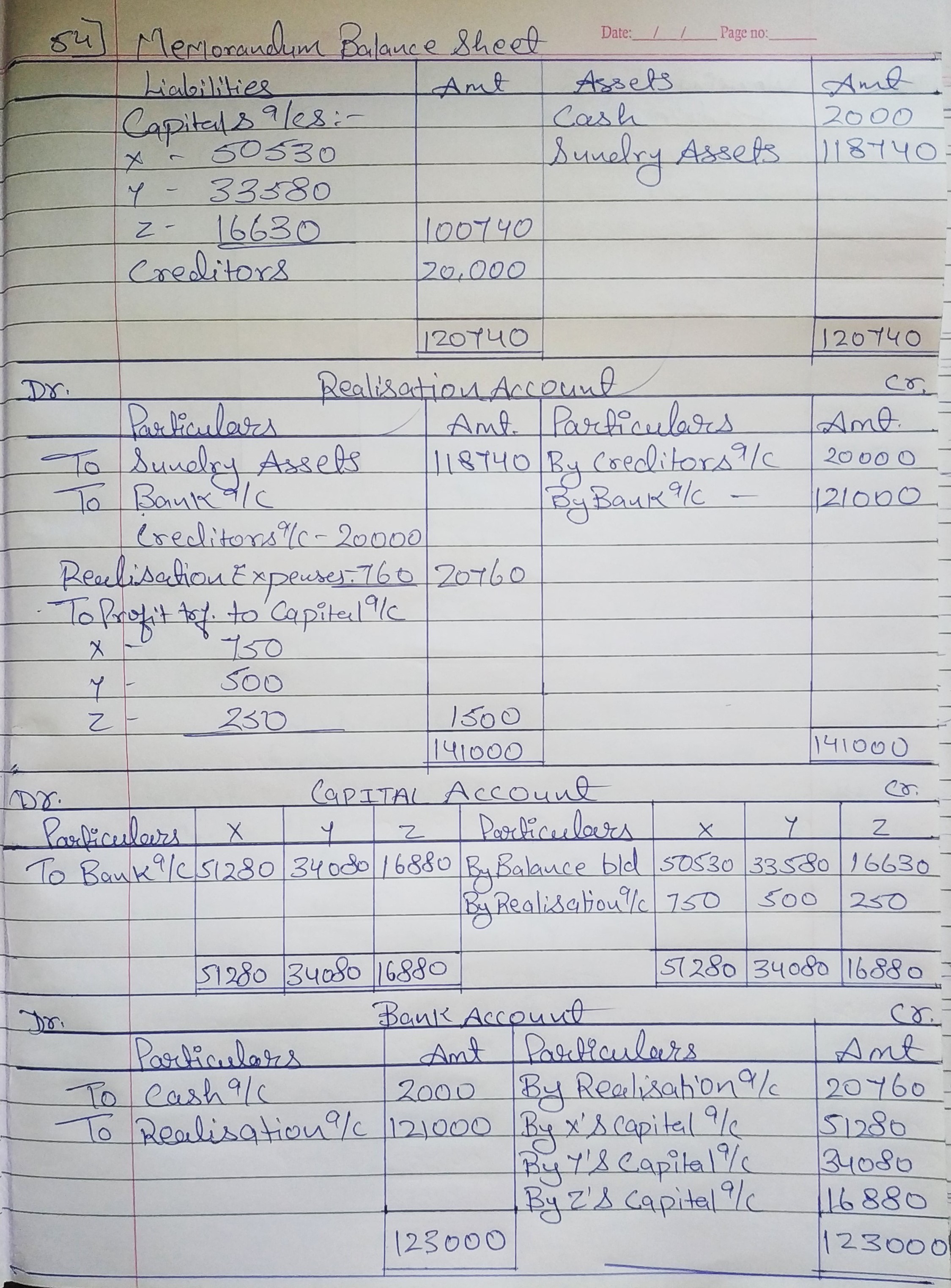

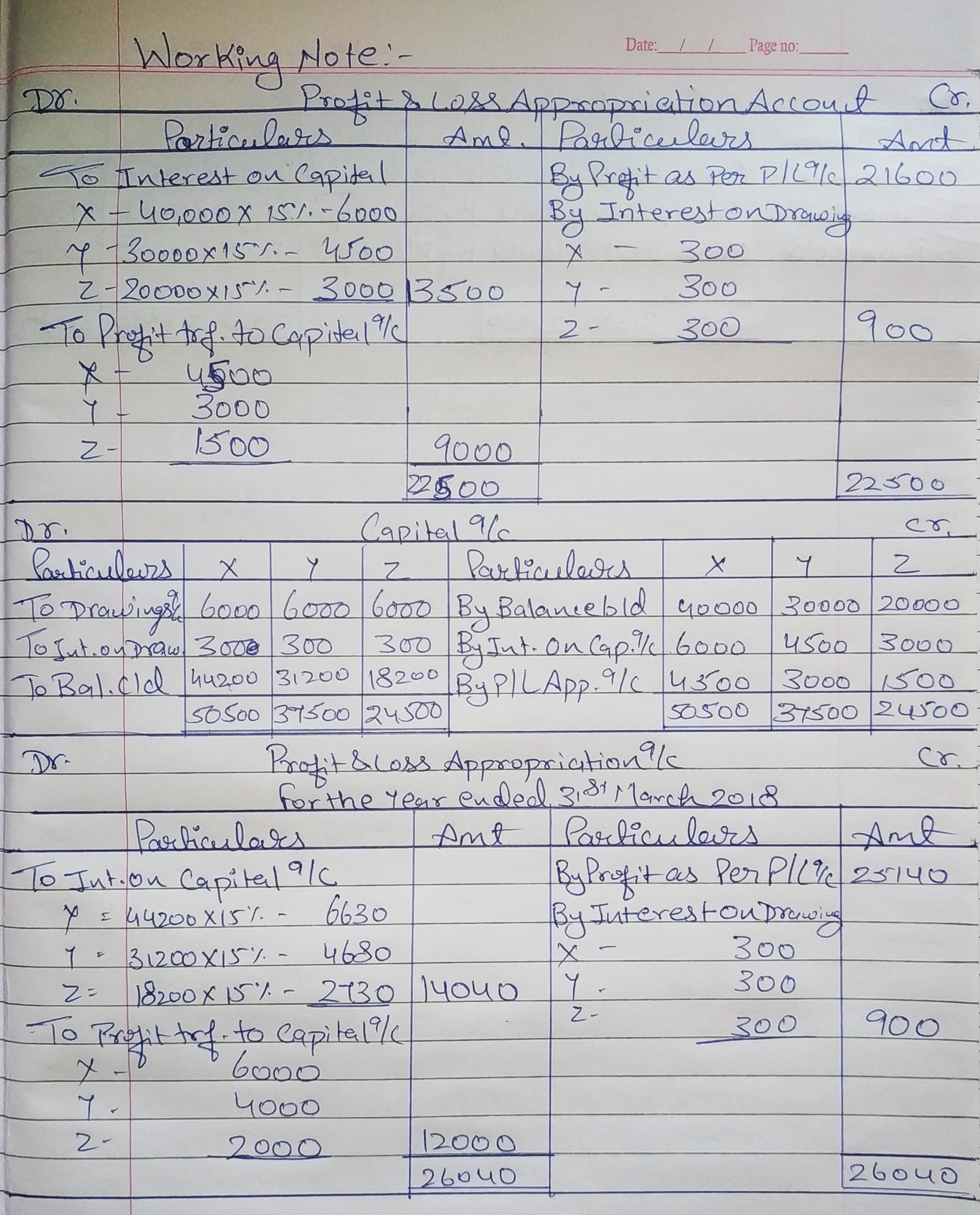

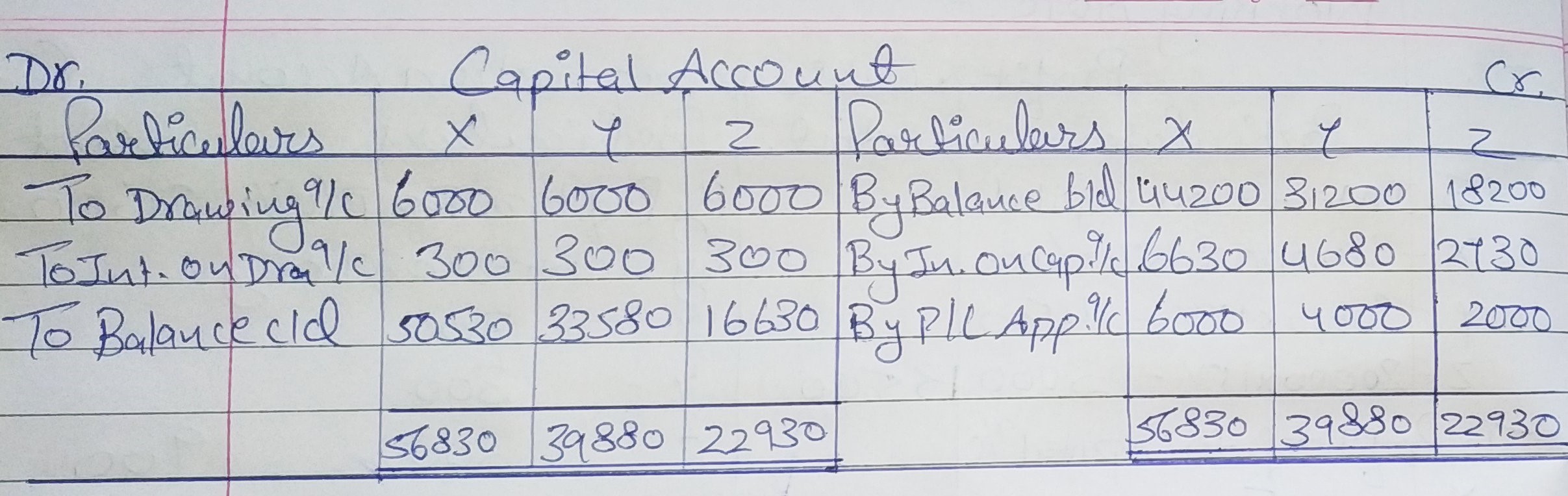

Question 54:

X, Y and Z entered into partnership on 1st April, 2016. They contributed capital ₹ 40,000, ₹ 30,000 and ₹ 20,000 respectively and agreed to share profits in the ratio of 3 : 2 : 1. Interest on capital was to be allowed @ 15% p.a. and interest on drawings was to be charged at an average rate of 5%. During the two years ended 31st March, 2018, the firm made profit of ₹ 21,600 and ₹ 25,140 respectively before allowing or charging interest on capital and drawings. The drawings of each partner were ₹ 6,000 per year.

On 31st March, 2018, the partners decided to dissolve the partnership due to difference of opinion. On that date, the creditors amounted to ₹ 20,000. The assets, other than cash ₹ 2,000, realised ₹ 1,21,000. Expenses of dissolution amounted to ₹ 760.

Draw up necessary Ledger Accounts to close the books of the firm.

ANSWER: